South Africa heading for a miracle

South Africa is on track to achieve a fiscal miracle in coming back from the brink of a debt trap in a stagnant economy, with the National Treasury’s policy of fiscal consolidation bearing fruit.

Coupled with the official announcement of a lower inflation target, South Africa could be entering a virtuous cycle it has not experienced since the mid-2000s.

The past 15 years have been characterised by excessive government spending, a slowing economy, and money flowing out of South African assets.

This picture seems to have been reversed, with the National Treasury reining in state expenditure, economic growth expected to pick up in the coming years, and foreign investors returning to the country’s bond market.

All of this can be accelerated by continued reforms and the achievement of structurally lower inflation in South Africa, which will boost economic growth, reduce the state’s debt-servicing costs, and ultimately ease financial pressure on households.

This is feedback from Symmetry’s chief investment strategist, Izak Odendaal, who explained that this is the culmination of years of effort to restore South Africa’s fiscal and economic credibility.

It has not been easy, with the progress coming at some cost to the country through slower economic growth and potential strain on service delivery.

Odendaal said fiscal consolidation is a painful process of constraining government spending and raising tax revenues, with taxpayers essentially paying more and getting less in return.

However, it has been necessary since South Africa followed the alternative approach of funding spending with debt for too long. The government now spends a fifth of tax revenues on interest payments, diverting funds away from other important social objectives.

The 2025 Medium-Term Budget Policy Statement is not a turning point in fiscal policy, as it is the culmination of years of effort. But it represents a turning point of sorts in investor perception of South Africa.

However, the country does still need faster economic growth as continued fiscal consolidation is not sustainable over the long run.

A bigger economy organically generates more tax revenues and increases the government’s capacity to service existing debt.

In terms of revenue and spending trends, it is notable that the current fiscal year will see SARS collecting R19 billion more than budgeted, despite softer-than-expected economic growth.

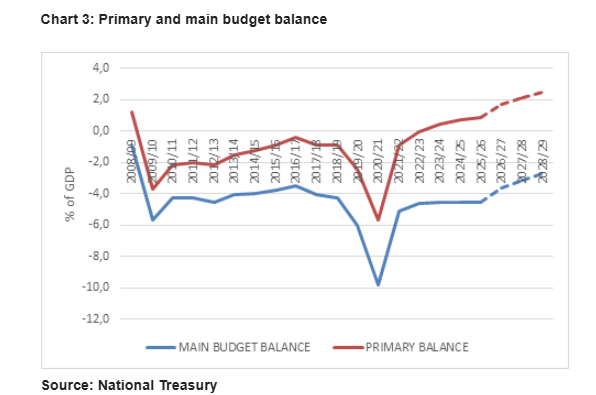

Putting spending and revenue side by side, the difference is the budget balance, which has been in deficit since 2008, meaning that spending consistently exceeded tax income.

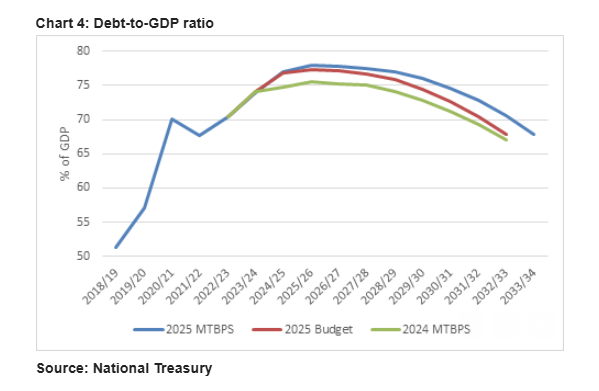

The gap was filled by borrowing, with the government’s outstanding debt rising to R5.5 trillion or 77% of GDP. This, in turn, drove the surge in annual interest payments, which doubled from 2.5% of GDP a decade ago.

If interest payments are excluded, a much better picture emerges. This is the so-called primary balance, which has been in surplus for the past three fiscal years and is projected to increase further over the medium term.

This essentially means that revenues now cover non-interest spending, with a bit left over to start paying down debt.

Lower inflation miracle

The other part of the puzzle is about enhancing South Africa’s credibility with investors further by lowering the inflation target to be in line with the country’s peers and more developed economies.

This promises immense benefits for South Africa, including a stronger and more stable rand, lower interest rates in the long run, and faster economic growth.

Odendaal said the benefits of achieving sustained inflation at or around 3% will be substantial for South Africa.

Households will experience a slower rise in the cost of living, while businesses will similarly not lose competitiveness against other countries as quickly.

After just 10 years, a country with 4.5% annual inflation will have a price level 20% higher than one with 3% inflation. After 20 years, the gap is 60%.

The theory of purchasing power parity suggests that the exchange rate between these two countries will adjust to restore competitiveness to parity.

This largely explains why the rand weakens so much over time against the currencies of relatively low-inflation economies such as the US dollar or euro.

Wrestling inflation down to 3% on a sustained basis – something that won’t happen overnight – therefore points to a more stable rand over time.

It also implies lower interest rates. If we assume that the repo rate should be 2.5% above inflation through the cycle, we are talking about it declining from 7% currently to around 5.5% eventually.

This will be a multi-year process, but the Reserve Bank is now likely to bring the next cut forward, perhaps even this week.

Since the government now officially supports a 3% inflation target, the Reserve Bank will have greater confidence that the target can be achieved over the medium term.

A large part of how inflation targeting works is that people must believe that inflation will be 3%, or whatever the number is.

With Treasury throwing its weight behind this target, it becomes easier to communicate to the population that they should anchor on 3%, as opposed to the slightly confusing message that the Reserve Bank aims for the lower end of the 3% to 6% range.

The message can also reverberate more quickly through the broader public service, which, as we know, has been the biggest culprit in giving above-inflation salary increases and implementing above-inflation increases in administered prices.

Research from the Reserve Bank shows that a lower inflation target of 3% can result in additional GDP growth of over 0.25% per year within five years and 0.4% within a decade due to improved economic competitiveness.

These estimates are conservative, with the benefit set to be greater as lower interest rates ease the government’s debt-servicing costs and increase productive investment.

In the researchers’ baseline scenario, debt-servicing costs as a percentage of GDP are projected to decline from 5.4% in 2025 to 5.3% in 2030 and 4.8% in 2035.

This compares to debt-service costs that fall to 5.1% of GDP in 2029/30 and 4.2% of GDP in 2034/35. The researchers estimate that R130 billion of nominal fiscal savings would be realised in the first five years, rising to R600 billion by the end of the decade.

Comments