R1,600 relief on the cards for South African homeowners

Another 25 basis point interest rate cut at the Monetary Policy Committee’s (MPC) November meeting could see South African homeowners pay up to R1,674 less on home loans.

This would mark the sixth cut in the current cycle, with the Reserve Bank’s MPC already having delivered 125 basis points worth of cuts since September 2024.

However, some experts have their doubts regarding whether another interest rate cut is on the horizon or if the MPC will maintain its hawkish tone and keep rates unchanged.

South Africa’s current cutting cycle came after a brutal hiking cycle that saw the MPC deliver 475 basis points of cuts, followed by a four-month standstill.

Therefore, the first interest rate cut of the current cycle, delivered in September 2024, came as welcome relief for many South Africans and the economy.

To ease pressure on households even further, the cuts have come alongside some of the lowest inflation rates South Africa has seen in years, with CPI inflation hitting a low of 2.7% in March 2025.

While inflation has trended upwards since, it has remained well within and closer to the bottom end of the Reserve Bank’s target range of 3% to 6%.

South Africa’s latest inflation print for September 2025 saw CPI inflation at 3.4%. While higher than the 3.3% recorded in August, this remains close to the MPC’s new preferred target of 3%.

Therefore, with this low inflation environment and the economy in desperate need of a boost, many experts expect the Reserve Bank’s MPC to announce another interest rate cut at its 19 November meeting.

Another 25 basis point cut would bring South Africa’s repo rate down to 6.75% and the prime lending rate to 10.25%.

Daily Investor calculated how much South African homeowners can expect to save on a standard 20-year home loan if this cut is announced on 19 November.

The table below shows these findings. The average savings among these house prices is R921.

| Home loan value | Current payment with prime rate at 10.50% | New payment with a 25 bps cut, prime rate at 10.25% | Savings |

| 1,000,000 | R9,984 | R9,816 | R167 |

| 2,000,000 | R19,968 | R19,633 | R335 |

| 3,000,000 | R29,951 | R29,449 | R502 |

| 4,000,000 | R39,935 | R39,266 | R669 |

| 5,000,000 | R49,919 | R49,082 | R837 |

| 6,000,000 | R59,903 | R58,899 | R1,004 |

| 7,000,000 | R69,887 | R68,715 | R1,172 |

| 8,000,000 | R79,870 | R78,531 | R1,339 |

| 9,000,000 | R89,854 | R88,348 | R1,506 |

| 10,000,000 | R99,838 | R98,164 | R1,674 |

Reserve Bank’s balancing act

While an interest rate cut may make sense given South Africa’s low inflation, the potential lowering of the Reserve Bank’s inflation target may complicate matters.

At its last meeting in September, the MPC was also faced with a low inflation environment – with August’s CPI print at 3.3% – but chose to keep rates unchanged.

This decision received severe backlash from several stakeholders and prominent South African business voices, including Purple Group CEO Charles Savage.

“Sorry, SARB, but that has to be the most out-of-touch decision I’ve ever seen. Everything was in your favour to reduce rates. Everything.”

NWU Business School Professor Raymond Parsons said that, given the overall balance of risks facing South Africa’s economy, it would have made sense to implement another 25 basis points cut.

He listed several factors that support this view, including average inflation in 2025 now being close to 3%, lower inflationary expectations, an easier US monetary policy, a stronger rand, and no evidence of demand inflation.

The MPC’s hawkishness was attributed to South Africa’s looming inflation target change, with the National Treasury and Reserve Bank having been in talks regarding this topic for months.

While the Reserve Bank has been a staunch supporter of lowering and narrowing the country’s inflation target, ideally to 3%, the Treasury has been more hesitant, which has seen discussion drag on for months.

In the meantime, the MPC announced at its July 2025 meeting that it will now aim for inflation expectations to settle at the bottom of its target range, 3%.

It is important to note that this is not an official change of the inflation target, but merely the MPC’s preference, similar to how it previously aimed for inflation to be anchored around the midpoint of its target range, 4.5%.

However, experts still believe this stated preference and the looming target change are what influenced the MPC’s decision to keep rates unchanged in September.

It makes sense for the MPC to aim to keep inflation at or near the 3% target in case an official change is announced, as this would mean it would not need to keep interest rates higher for longer to bring inflation back down.

“The cautious stance by the majority of the MPC would thus seem to be rather linked to wanting to keep rates higher for longer to entrench its preferred lower 3% inflation target,” Parsons said.

Therefore, until an official change to the inflation target is announced, the MPC’s decision-making will remain highly uncertain, with November likely to bring either relief in the form of a cut or more of the same.

“The future level of borrowing costs is a crucial area of decision-making for the economy, for which a settled official inflation targeting framework is highly desirable for policy certainty. The sooner this is decided, the better,” Parsons said.

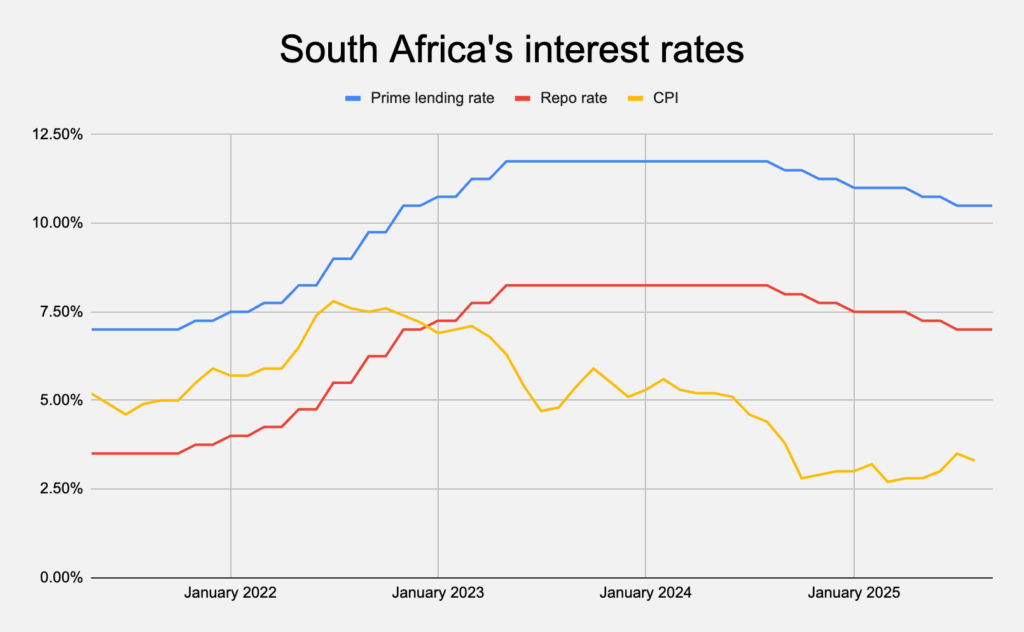

The graph below shows the trends in South Africa’s inflation and interest rates between May 2021 and September 2025.

Comments