South Africa is headed for trouble

The continued mismatch between the Reserve Bank and the National Treasury could spell trouble for South Africa’s fiscal future.

While the Reserve Bank is pushing for a lower inflation target, the Treasury has been hesitant to make this policy official and has been planning fiscal spending and revenue around higher inflation.

The Bureau for Economic Research’s (BER) Claire Bisseker recently explained that the Reserve Bank’s new preference for a 3% inflation target presents significant problems for the National Treasury and its upcoming ‘mini-budget’.

The discussion surrounding a lower inflation target has been ongoing for most of 2025, with the Reserve Bank and Treasury having been in discussion for months.

However, no official change has been announced yet, as this task falls to the National Treasury, which has been dragging its feet on the issue.

In the meantime, the Reserve Bank has unofficially changed its target from 4.5% to 3%, having stated its preference for this lower target back in September.

This came amidst low inflation in South Africa, which has averaged just over 3% in the year to date.

Bisseker explained that the Reserve Bank’s preference for a 3% inflation target has significant implications for the expected growth in nominal GDP and, therefore, anticipated revenue growth.

This creates a problem for the Treasury, which has budgeted for nominal GDP growth to average 6.3% over the medium term.

In reality, this figure will likely be closer to 4% given much lower inflation than anticipated and slower real GDP growth than initially expected.

“Since all fiscal ratios are measured relative to nominal GDP, this means that the Treasury’s fiscal targets will be harder to achieve over the medium term,” Bisseker explained.

Luckily, she said the Treasury’s recent revenue windfall will help to offset this.

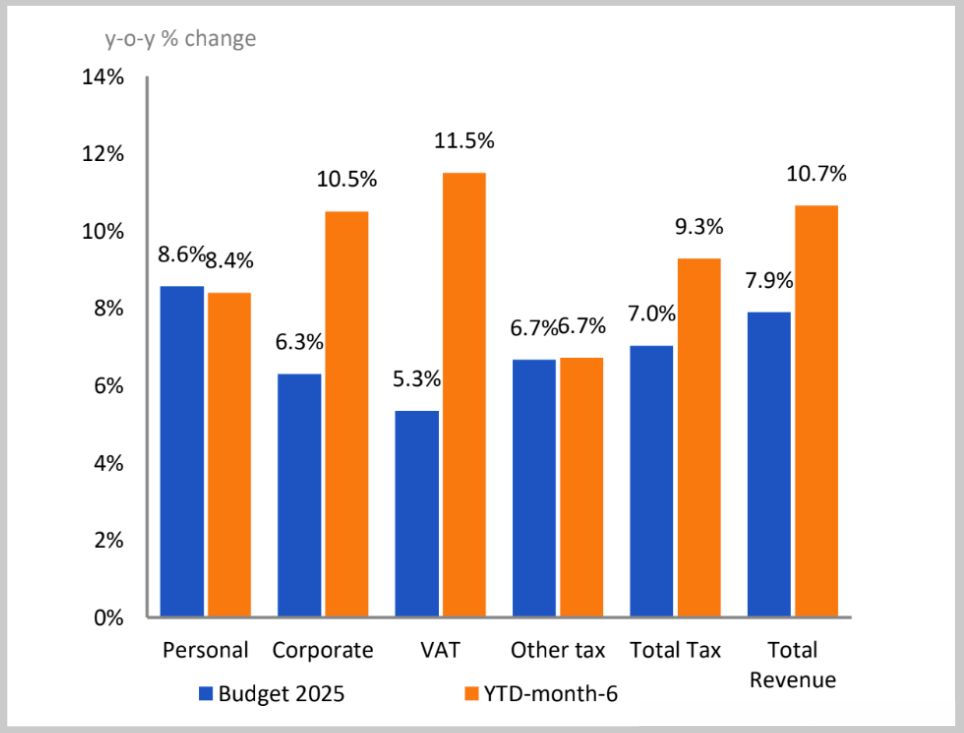

Data from April to September 2025 shows that total revenue was 10.7% higher than the same period last year, running well ahead of the 2025 budget whole-year target of 7.9%.

However, Bisseker pointed out that this is mostly due to temporary base effects and cyclical factors, with 2025’s strong commodity price growth boosting the profits of miners and, therefore, corporate income tax revenue.

The graph below, courtesy of the BER, compares the government’s budgeted revenue versus year-to-date revenue.

Policy mismatch

Bisseker explained that the Reserve Bank’s preference for inflation of 3% also implies that, as it acts to reduce inflation, nominal tax revenues could fall in tandem.

“If the Treasury doesn’t anticipate this by marking down spending growth in the medium-term budget, South Africa could be in even bigger trouble fiscally,” she warned.

This is particularly concerning ahead of the Treasury’s upcoming Medium-Term Budget Policy Statement on 12 November, which will provide an update of the government’s macroeconomic and fiscal projections.

Bisseker said it will be difficult for Finance Minister Enoch Godongwana to present a wholly credible three-year budget without a credible inflation forecast, which in turn needs clarity on the target.

“If he fails to clarify this issue on 12 November, and instead delays it to the February 2026 national budget, it will detract from the good fiscal news that the day is expected to bring,” she said.

This is not the only problem that delaying the announcement of a lower target could present.

Several economists have warned that the government has a very narrow window to adjust the inflation target while minimising the impact of short-term risks that could result from the change.

Lowering South Africa’s inflation target could hold immense benefits for the country, including lower inflation and interest rates over the long term.

A lower target will also bring South Africa more in line with its global peers, improving the country’s export competitiveness, and could alleviate the government’s heavy debt servicing burden.

However, these benefits will come with some short-term pain, including a negative impact on the country’s already weak growth and increased pressure on households with debt.

This is because, in order for inflation to settle around the new, lower target, interest rates may need to be higher for longer.

Therefore, economists have urged the government not to delay changing the target for too long, as inflation could accelerate, requiring higher interest rates for longer to bring inflation down to the lower target.

Comments