South Africa is in serious financial trouble

South Africa’s debt-servicing costs have more than doubled as a share of total government spending in the past 15 years, threatening to push the country into a debt trap.

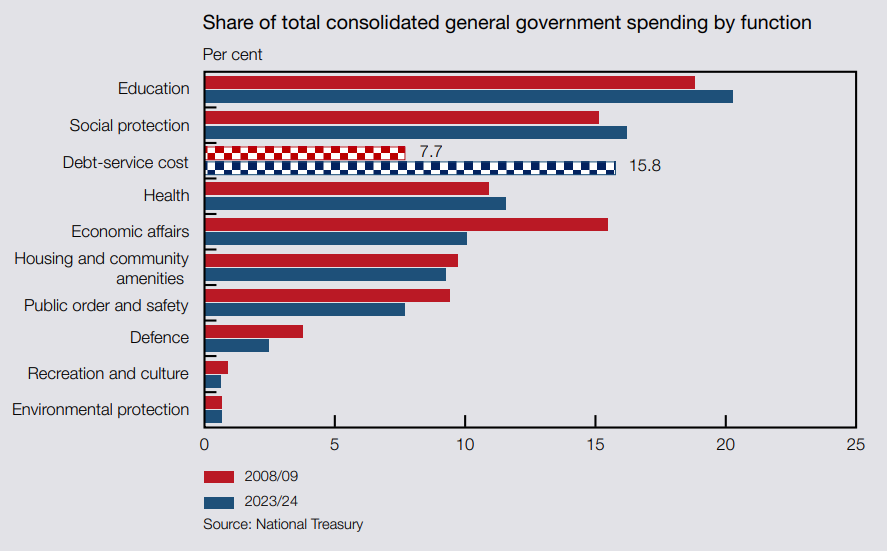

Higher debt-servicing costs have eaten up the government’s spending power, with it set to spend more on interest payments than education in the current financial year.

These costs also translate into large budget deficits, potentially resulting in the country issuing new debt to pay off existing debt, creating a debt trap.

This was outlined in the Reserve Bank’s latest Quarterly Bulletin, which showed the rapid deterioration of South Africa’s financial health since 2008/09, when the government last ran a budget surplus.

The Reserve Bank said since then, the national government’s debt has steadily grown. Along with this growth comes rising debt-servicing costs.

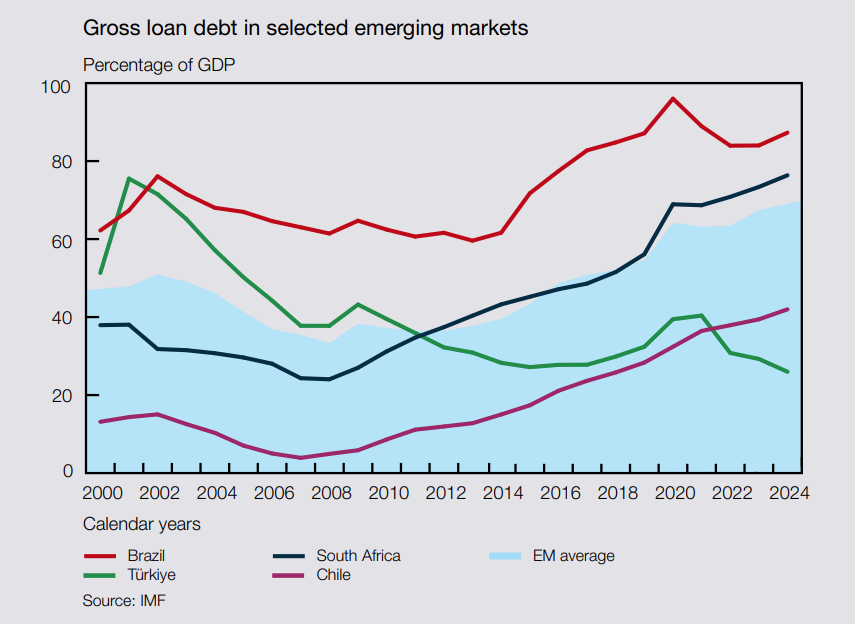

As a share of GDP, South Africa has experienced one of the fastest increases in government debt in history, from 24% in 2008/09 to over 76% at the end of the 2025 financial year.

This growth is much faster than its emerging market peers over the same period, with the country’s debt-to-GDP ratio now exceeding the average for emerging markets since 2020.

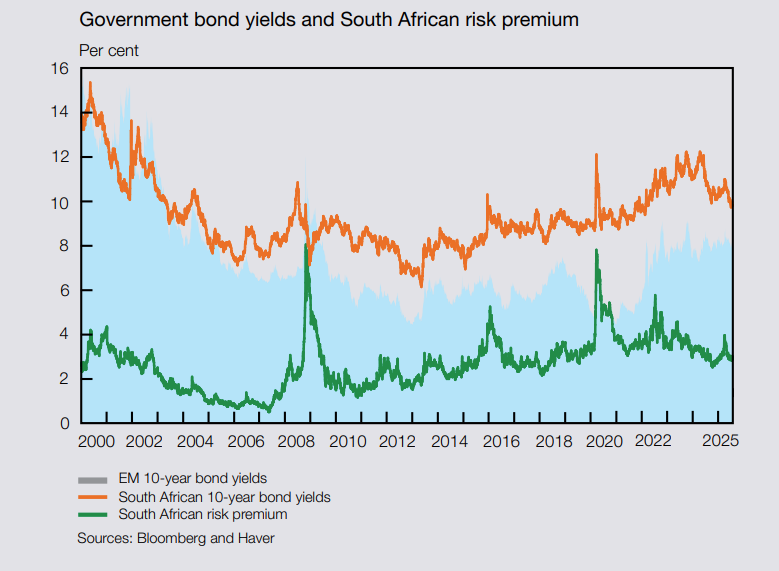

The rising debt burden has been coupled with elevated interest rates as South Africa’s risk premium has ballooned over the same period.

As South Africa’s credit ratings deteriorated, the premium the country has to pay to get investors to hold its debt has increased.

This pushes the interest rates on South Africa’s debt higher, making it more expensive for the country to borrow and service this debt.

The Reserve Bank noted that the government has little control over bond yields, but it can manage perceptions of risk through credible financial management and resilience to external shocks.

These are things the government has failed to do over the past 15 years, with the country’s fiscal risk profile subjected to immense scrutiny and uncertainty.

This has resulted in South Africa’s bond yield rising more than those of other emerging markets amid increasing global uncertainty.

The Reserve Bank said this is primarily due to South Africa’s growing debt levels and elevated debt-servicing costs, alongside slow economic growth.

The graphs below show South Africa’s rising debt burden and the increased risk premium the country has to pay on its debt.

Eating up the budget

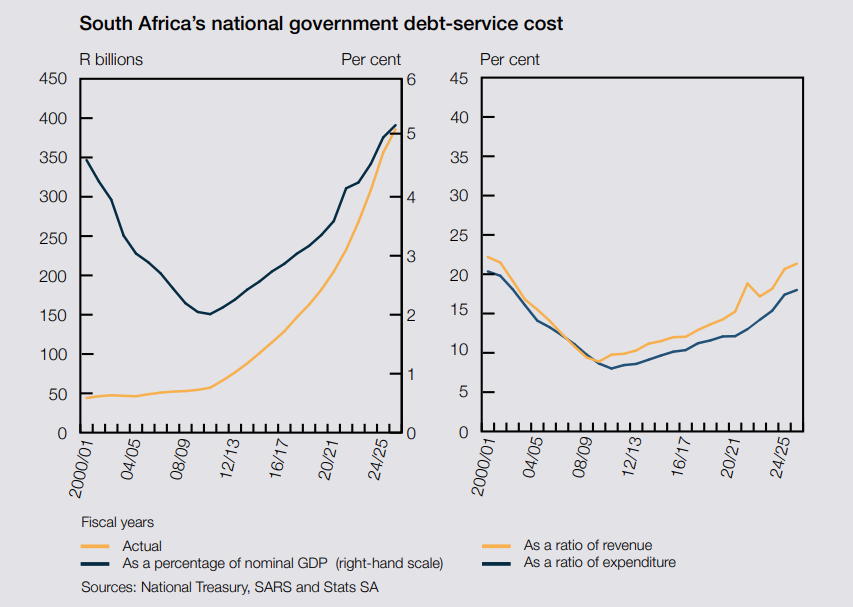

The combination of a rising debt burden and increased interest rates on the debt has resulted in South Africa’s annual debt-servicing costs skyrocketing over the past 15 years.

South Africa’s debt-servicing costs have risen from R54.3 billion in 2008/09 to R385.6 billion in the 2024/25 financial year.

This is a compound annual growth rate of 13.1%, making debt-servicing costs the fastest-growing expenditure item in the national budget.

The increase reflects the combined impact of rising debt and elevated borrowing costs, both of which present significant fiscal constraints, the Reserve Bank said.

It warned that South Africa’s finances risk becoming unsustainable, with higher debt-servicing costs resulting in wider budget deficits, increasing the risk of falling into a debt trap.

After declining to a low of 8.9% as a share of GDP in 2008/09, debt-servicing costs have increased notably and are set to peak at 21.9% in 2025/26.

As a share of government expenditure, debt-servicing costs hit a low of 8.6% in 2008/09 and are set to peak at 18.4% in 2025/26.

The Reserve Bank said this reflects a greater allocation of resources towards servicing debt, crowding out expenditure from other areas such as infrastructure investment, social services, and economic development.

If debt-servicing costs continue to grow at the same rate, the government is set to spend more money on paying interest than social grants in the coming three years.

As more resources are allocated to interest payments, the share of spending on infrastructure, education, health and economic development reforms has declined over time, undermining the government’s goal of building a more resilient and inclusive economy.

In addition, the escalating cost of servicing debt has necessitated running a primary surplus during the past two fiscal years.

Although this is required to curb the growth in government debt, it is also associated with a slowdown in essential public services spending – a practice referred to as ‘austerity’.

The growth of debt-servicing costs as a share of government spending from 2008/09 to 2023/24 can be seen in the graph below.

Comments