Government has misled South Africans for a decade

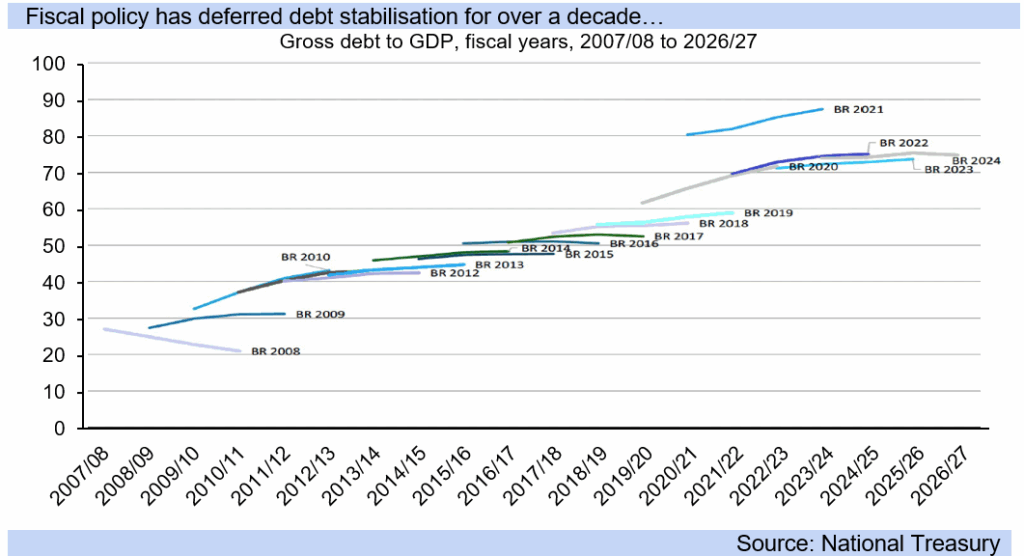

South Africa’s government has projected a stabilisation in the country’s debt pile for over a decade, with the burden more than tripling since 2010 as a share of GDP.

While the government’s debt burden has been projected in almost every Budget Speech since 2009, in practice, the target has been repeatedly postponed.

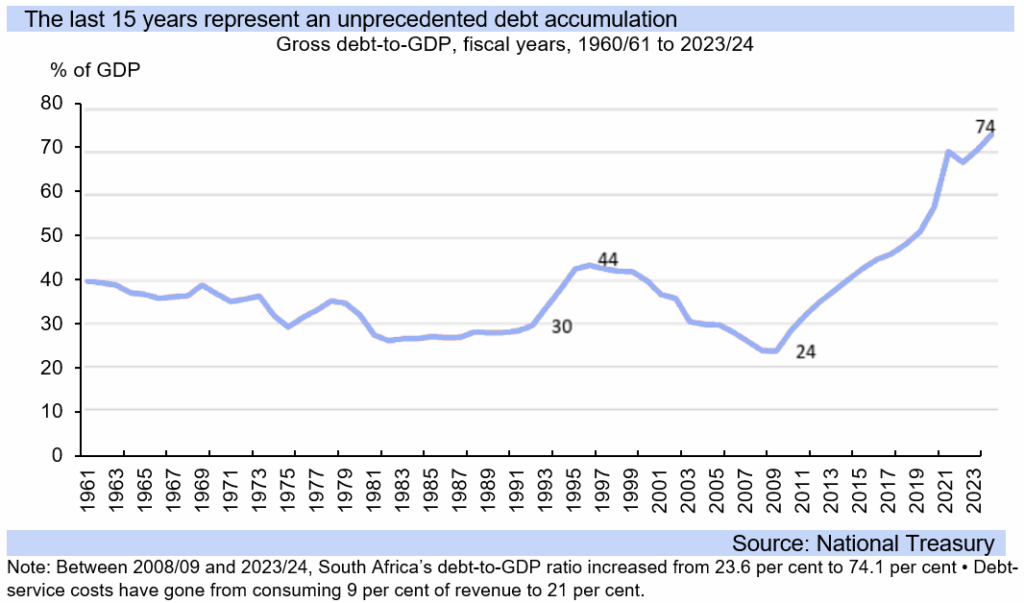

This has resulted in South Africa’s debt burden growing significantly over the past 15 years, from 24% of GDP in 2010 to over 75% in 2025.

The rise in South Africa’s debt burden has translated into the country’s deteriorating credit ratings, with it being three notches below investment grade. This is also known as junks status.

A BB- credit rating from Fitch for South Africa’s government bonds results in South Africa being grouped with countries such as Turkey, the Ivory Coast, Namibia, Jordan, Jamaica, Armenia, Nepal, and Turkmenistan.

Credit ratings represent the perceived creditworthiness of countries’ debt, that is, their ability to repay, and South Africa’s is seen to have deteriorated substantially, Investec chief economist Annabel Bishop said.

This is because the country’s gross debt escalated from 23.6% as a share of GDP in 2008/2009 to 76.9% at the end of the 2024 financial year.

The escalation in borrowing has resulted in debt service costs jumping from 9% to 21% of government revenue, as the benchmark bond yield escalated from near 6% to above 12% at times.

South Africa’s benchmark ten-year government bond yield has dropped to 9.11% this year from 12.23% in April, due to a number of factors, Bishop said.

The deterioration of South Africa’s financial health only accelerated in recent years, with the 2020 lockdowns resulting in government borrowing jumping substantially as economic activity fell.

However, the current financial situation the state finds itself in is not a result of borrowing during the pandemic, but is the result of 15 years of economic mismanagement and excessive government spending.

The National Treasury noted that since 2009, nearly every budget has projected debt would stabilise in the near future.

However, the stabilisation target has been repeatedly postponed and revised upwards as we failed to achieve the necessary fiscal adjustments.

Each postponement, while often seeming legitimate at the time, has had a cumulative effect and now puts the country on the edge of a financial crisis.

The growth in South Africa’s debt burden and the repeated projections of stabilisation can be seen in the graphs below, courtesy of Bishop.

Closer than ever

The National Treasury’s policy of fiscal consolidation has ensured the government is closer than ever to achieving the goal of debt stabilisation.

In a research note after the last iteration of the Budget Speech this year, chief investment strategist at Old Mutual’s Symmetry Izak Odendaal said this policy is crucial to the country’s financial sustainability.

South Africa has been trying to rein in borrowing and stimulate economic growth for the past decade, without much success.

While the country’s economic growth has yet to pick up meaningfully, Odendaal said the National Treasury has done a good job of reining in government spending and limiting growth in the country’s debt.

He explained that the severe financial situation the state finds itself in has created a sense of urgency in the National Treasury.

It usually takes a sense of crisis for politicians to make difficult decisions, usually because they can see trouble in the markets, the streets or at the voting booth, Odendaal said.

In South Africa’s case, that sense of crisis occurred in recent years. The poor state of the economy has forced a profound shift in thinking, and the private sector is being allowed – and encouraged – to invest in infrastructure.

The ballooning interest burden makes the cost of fiscal laxity very real. Every rand spent on interest could have been spent on health, education, or policing.

This crisis has forced the government to take action. It is undergoing fiscal consolidation to limit spending growth and thus, over time, stabilise and reduce the country’s debt burden.

Importantly, Treasury will maintain a primary surplus in the coming financial year, meaning that tax revenue is projected to exceed non-interest spending.

It will rise over the medium term from 0.7% of GDP to 2.1% in 2027/28. The main budget deficit, which includes interest payments, is expected to continue narrowing over the medium term, reaching 3.2% of GDP by 2027/28.

As a result of running a primary surplus, the debt-to-GDP ratio is projected to peak in the current fiscal year at 77.4% and drift lower over time.

Odendaal said a peak in the debt ratio has been promised for a decade and never happened, but we are closer than ever.

These projections can be seen in the graph below, courtesy of Odendaal.

Comments