South Africa’s electricity sector among the worst in the world

South Africa’s electricity sector is the second-most heavily regulated in the world, significantly limiting the entry of new generation capacity, which would bring load-shedding to an end and reduce costs.

The country has begun reforming the sector to make it easier for new players to participate, but this is taking too long, and more wide-ranging reforms are needed.

The Organisation for Economic Co-operation and Development (OECD) recently explained why South Africa needs to fundamentally restructure its electricity supply chain.

In its latest economic survey of South Africa, the organisation outlined some of the main reasons why the country’s economy has stagnated and how it can be revived.

It dedicated a chapter to the country’s electricity crisis, saying it is far from solved and a major barrier to faster economic growth.

One of the key ways in which South Africa’s economic growth can be revived is by having a more competitive electricity sector.

This will reduce the country’s reliance on a single company, Eskom, and enable the addition of new generation capacity to the grid.

Eskom’s current financial health limits its investment in new capacity and has contributed to its soaring cost of producing electricity, which is passed on to consumers.

This, in turn, ensures the country is still vulnerable to power outages and limits economic growth, as any pickup in activity will push demand significantly above supply.

The government is aware of this challenge and has begun reforming South Africa’s electricity sector to encourage new investment and competition.

However, the OECD said a fundamental restructuring of the entire electricity supply chain is needed to ensure long-term electricity security.

This includes establishing a competitive market, opening the distribution segment to include private operators and strengthening municipal financial and managerial capacity.

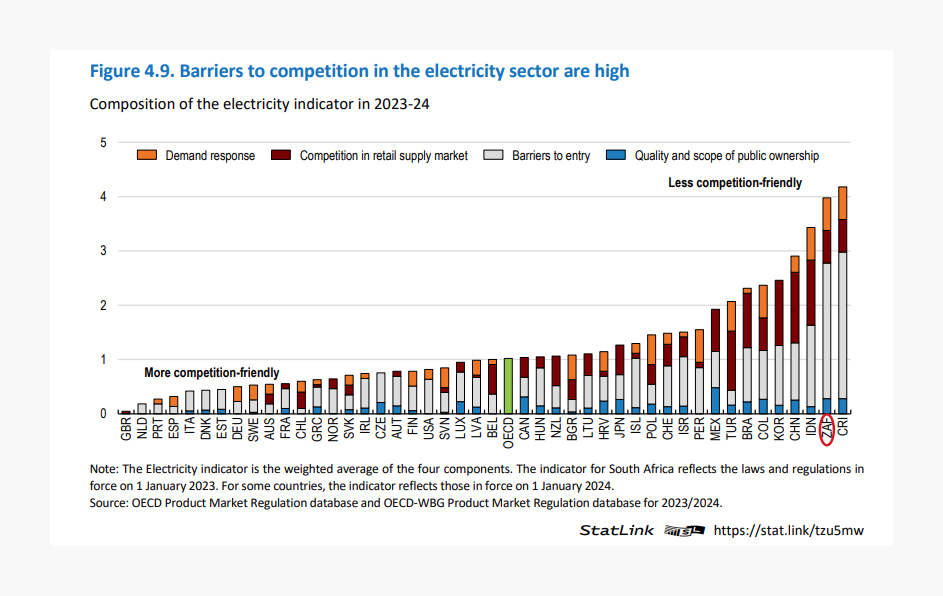

The electricity regulation component of the OECD’s Product Market Reform (PMR) indicator shows that South Africa’s electricity sector is more heavily regulated than nearly all OECD and emerging economies.

Eskom owns or operates most of the sector’s transmission and distribution segments and generates around 91% of the country’s electricity.

This current structure limits the entry of new players in all segments, providing preferential access for Eskom’s ageing fleet to the grid and limiting competition and energy security.

Third-party access is not yet fully established in both the transmission and distribution segments.

Access to the transmission grid is mainly limited to specific contracts procured by Eskom and the Electricity Ministry, with access granted based on availability and priority to Eskom generators.

In effect, Eskom has the power to set barriers for renewable energy investments and prioritise its own energy generation facilities, creating a major conflict of interest.

Integrating electricity generated privately into the distribution network is also conditional on municipal approval, with only a few municipalities having approved installations of embedded generation in their network facilities.

The graph below shows that South Africa’s electricity sector is the second-most uncompetitive among the countries studied by the OECD.

Slow progress being made

Significant progress was made in 2024 in laying the foundations for a more modern governance and market structure for the electricity industry.

Most notably, Eskom is being unbundled into three separate entities, each with independent management and financial autonomy.

The National Transmission Company of South Africa (NTCSA), operational since July 2024, was established as a wholly owned subsidiary of Eskom with an independent board, which is an important step towards full unbundling.

This separate entity is expected to ensure better and fairer access to the grid for all electricity generators.

A new fully independent transmission system operator (TSO), expected to replace the NTCSA, will manage the competitive market.

The Electricity Regulation Amendment Act, passed in August 2024, established the framework for a competitive regulatory environment.

This framework lays the foundation for creating a wholesale electricity market where energy can be bought and sold.

This will, in turn, facilitate a more flexible and efficient expansion of generation capacity, resulting in enhanced energy security.

However, the OECD warned that the implementation of these reforms needs to be quick and effective, to allow new capacity to be added to the grid in time for Eskom’s coal plants to be decommissioned.

A five-year transitional period is planned to make the NTCSA fully independent from Eskom and to establish the TSO.

The market is projected to start in 2026 with a limited number of participants. This phased approach will allow adequate time to develop and implement the essential institutional framework.

It also said the legal separation of the distribution and generation segments into subsidiaries of Eskom should be accelerated.

Separating the distribution grid operator functions from the electricity trading activities, which could be open to competition, has the potential to significantly enhance service delivery to end users.

One important implication is that the municipal trading function would eventually be open to competition; households and businesses would then be able to choose their electricity provider.

Comments