OUTsurance went from challenger to champion

OUTsurance has emerged as the dominant player in South Africa’s short-term insurance market, with it now setting its sights on global expansion in Australia and Ireland.

As part of this journey, the company has overtaken historic rivals that have operated in South Africa’s insurance space for over a century.

Senior equity analyst at Melville Douglas, Khumbelo Nevhorwa, recently outlined how OUTsurance has come to dominate short-term insurance in South Africa and whether it could replicate this success elsewhere.

Founded in 1998, OUTsurance has experienced rapid growth from being an annoying disruptor to a behemoth valued at over R110 billion on the JSE.

Nevhorwa explained that the key to this success was the company’s successful disruption of the short-term insurance market, which was historically dominated by insurers with large broker distribution networks for underwriting.

OUTsurance adopted a direct-to-market approach early on in its history, reducing its distribution costs and enabling rapid growth without substantial capital expenditure to build out a broker network.

Coupled with this was the insurer’s careful claims management and refined pricing accuracy through its proprietary price rating model.

This model and OUTsurance’s lower distribution costs remain central to the insurer, enabling it to consistently offer better value to consumers and, in turn, enhanced returns to investors.

Another key factor in OUTsurance’s growth is the company’s focus on short-term insurance, which has the potential to be immensely cash-generative – if management is sound.

Short-term insurance typically includes car, home, and third-party insurance for individuals and businesses. Funeral and pet insurance are becoming increasingly lucrative areas of short-term insurance.

Why short-term insurance

Nevhorwa explained that short-term insurance is inherently cash-generating, with profits earned through the difference between premiums collected and claims paid.

Short-term insurance stands out for its frequent cash flow, as premiums are paid monthly or annually, and claims for most lines of business are settled within 12 months.

Premiums are invested to generate returns during the waiting period for claims, producing additional ‘float returns’. Companies can also earn returns on equity capital buffers, which are typically invested in interest-bearing assets.

This makes them highly lucrative businesses, as earnings can be produced through premium sales and investment returns.

However, Nevhorwa explained that this requires good management and immense discipline to ensure the virtuous cycle can play out.

Insurers that excel in underwriting, investment management and fund returns can generate profits far exceeding their internal rate of return, producing substantial profits and cash for shareholders.

Nevhorwa said OUTsurance has embodied these characteristics over the past 27 years and has garnered a reputation as a steady compounder of earnings.

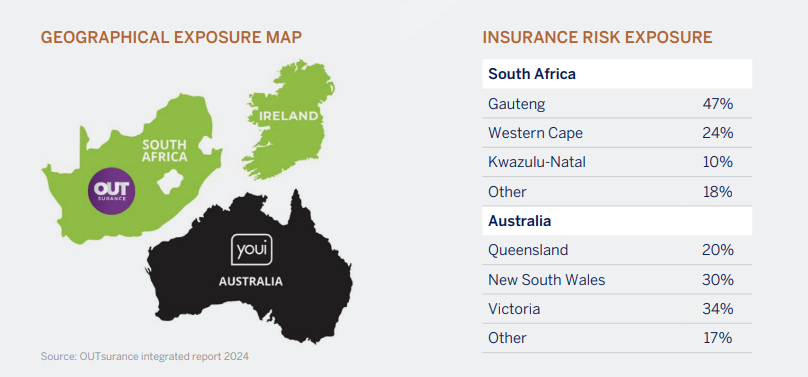

Over two decades later, the insurer is now expanding this model under its own brand in South Africa, Youi in Australia, and OUTsurance Ireland.

In South Africa, premium growth has averaged an annualised rate of 6.3% over the past 10 years, primarily fueled by inflation-driven price adjustments in their mature personal line business.

In Australia, premium growth has been exceptional, reaching an annualised rate of 12.93% over the past 10 years. This growth is attributed to market penetration and favourable exchange rates from a weaker rand.

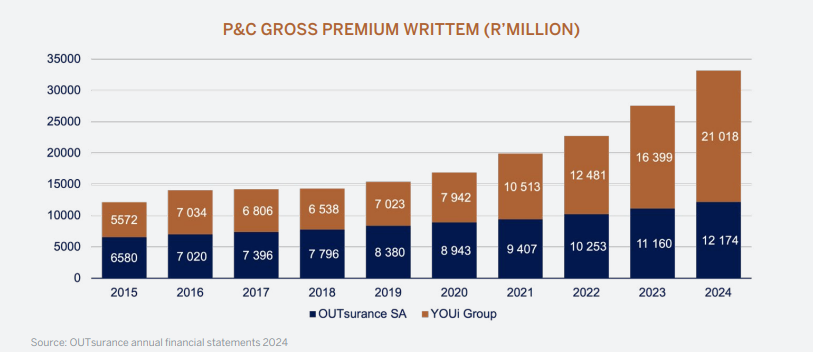

The company’s gross premium written growth can be seen in the group below, which also shows how significant its Australian operations have become.

Continued growth at risk

Management is actively expanding into the business insurance market, supported by the OUTsurance Business Brokers initiative.

This strategy has proven effective, with volumes growing and profits entering a positive trajectory on the J-Curve.

However, as many insurers have warned recently, OUTsurance is threatened by the rise of catastrophic events in both South Africa and Australia.

This puts pressure on short-term insurers to reprice policies relatively quickly and evaluate their coverage to ensure they remain profitable.

Despite more frequent catastrophic events like floods, storms, and wildfires, OUTsurance has shown an ability to reprice policies promptly and mitigate claims impact.

Nevhorwa explained that this is where OUTsurance’s internal pricing and claims systems come into their own, enabling it to reprice policies quickly and profitably.

This is important not only for the company’s financial performance but also for its reputational risk over time, which is a vital part of the insurance business.

Despite this ability, increased catastrophic events in South Africa and Australia still pose a substantial threat to OUTsurance’s business.

Such events, particularly if they are widespread or occur in short order, can lead to insurable losses exceeding normal claims expectations, impacting earnings and capital reserves.

This deals a double blow in terms of impaired financial performance and a reduction in investable returns, which provide an important source of earnings.

One way in which insurers can mitigate against this threat is by increasing their geographic diversification, which is an underappreciated reason for OUTsurance’s expansion into Australia and Ireland.

The Irish expansion, in particular, offers rich rewards, as the catastrophic events that South Africa and Australia experience tend to coincide due to the countries’ similar climates.

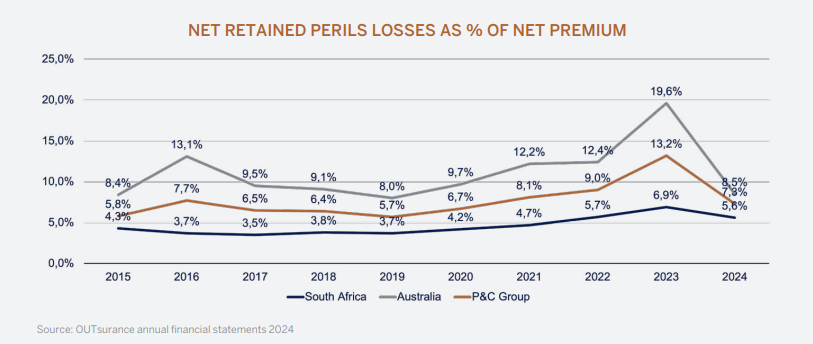

OUTsurance has worked on reducing its overall exposure to particular areas by diversifying its underwriting across product lines and geographies. It also utilises reinsurance to transfer a portion of catastrophic losses.

This results in the insurer maintaining its peril losses at a fairly consistent share of net premiums. This can be seen in the graph below.

Future growth

In recent years, OUTsurance has faced questions regarding where its future growth will come from as it has rapidly reached maturity in the South African insurance market.

Over the past 27 years, the company has grown to become the dominant motor insurer in South Africa and has a significant market share in other personal insurance segments.

This has forced it to look elsewhere for growth, including funeral and pet insurance, which are growing strongly in South Africa, but remain a relatively small share of the company’s earnings.

Nevhorwa said there is particularly strong growth potential in business insurance, where OUTsurance’s direct-to-market model has been less successful.

However, most of its future growth will come from outside South Africa, with continued expansion in Australia reaping rewards and the newly launched Irish business showing good potential.

OUTsurance’s Australian business, YOUi, has plenty of room to grow outside of Queensland state, with it progressively expanding its operations.

The company’s Irish business has yet to prove its ability, with OUTsurance only formally launching operations in May 2024.

Nevhorwa explained that what makes OUTsurance unique is its historic management of expansions into new markets.

While all companies promise strong cost control when expanding, very few have a strong track record of well-managed expansions, particularly outside South Africa.

OUTsurance is an exception in how it has managed to expand very profitably into Australia, which bodes well for its Irish business.

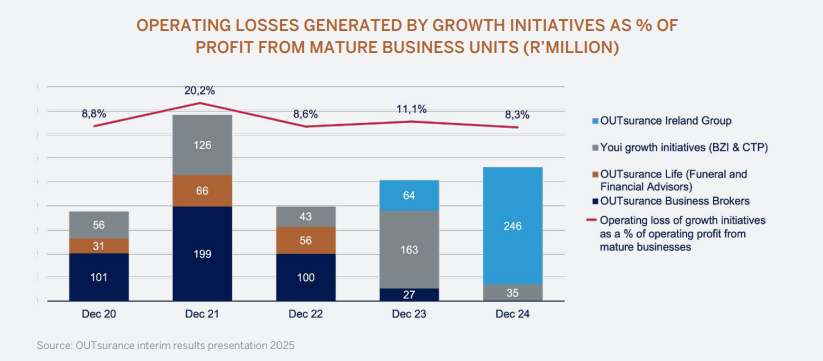

Nevhorwa also explained that the company has a strict policy to limit the losses of new ventures to 10% of operational profits to ensure its capital buffers are protected.

This disciplined approach has proven effective, enabling OUTsurance to prioritise sustainable growth while maximising operational efficiency. The graph below shows this in action.

Comments