One of South Africa’s oldest companies taking the JSE by storm

Premier is well-positioned to deliver strong returns for shareholders, with a new mega bakery and major acquisition set to take the food producer to new heights.

Anchor Capital investment analyst Sean Culverwell recently outlined Premier as one of the asset manager’s top stock picks for 2026.

Founded over two centuries ago in 1824, Premier is not only one of South Africa’s oldest food producers, but also one of the country’s oldest companies.

Premier began as Attwell’s Bakery, a small Western Cape bakery that would later expand into a chain and merge with the Port Elizabeth Steam Mill Company to form the South African Milling Company.

The South African Milling Company oversaw major milestones, including the first advertisement for Snowflake Flour, the construction of new mills, and the company’s expansion into maize meal, samp and shipping.

The company continued to expand into the 1910s, at the same time that businessman Joffe Marks established Premier Milling Company.

Marks had previously founded Marks & Co in 1890, starting with a single mill at Fordsburg, and later expanding the business to include flour and maize mills.

Marks & Co expanded rapidly through acquisitions, including Union Flour Mills and the Vereeniging Milling Company, which would later become Epic Oil Mills and EPOL Animal Feeds.

Premier was established as the successor business to Marks & Co., and soon became the largest industrial food producer in the Southern Hemisphere.

In 1964, Premier merged with the South African Milling Company and continued to expand the company’s offerings, constructing new mills across the country.

Another big change came in 1998, when General Foods Industries purchased Premier, which was called Premier Foods Industries at the time, and merged into Premier Foods Limited.

Less than a decade later, in 2004, the Foundation for African Business and Consumer Services (FABCOS) acquired a 74% stake in Premier Foods.

With this acquisition, FABCOS became the controlling shareholder with 55%, while Genhold, Genfood’s holding company, held a 26% stake.

In 2011, another major company, billionaire Christo Wiese’s Brait, showed interest in Premier, becoming the food producer’s strategic long-term shareholder.

Premier continued its acquisition spree in the years to follow, adding well-known brands like Mister Bread, Manhattan, and Lil-Lets to its stable.

Today, the company is still one of South Africa’s largest food producers, known for brands like Snowflake Flour, Blue Ribbon, Iwisa, Mister Sweet, and Super C.

Premier listed on the JSE in 2023 and has since seen its share price skyrocket by over 175%, creating tremendous value for shareholders. Culverwell expects this strong run to continue into 2026.

The ‘Shoprite’ of milling and baking

Culverwell said that, under Brait’s stewardship, Premier has invested around R3.5 billion in acquisitions since 2012 and over R7.5 billion in capital expenditure to upgrade its manufacturing facilities and distribution network.

“Headlined by its flagship Blue Ribbon brand, Premier has effectively become the ‘Shoprite’ of milling and baking,” he said.

“The company’s growth strategy hinges on three core drivers: single-digit revenue growth, operating margin expansion, and declining finance costs. “

He explained that Premier’s consistent execution against these three levers has delivered industry-leading growth since its listing, a trend he expects to continue in 2026.

The first major factor working in Premier’s favour is the opening of its long-delayed Aeroton mega-bakery in November.

The group announced in its latest interim results that the commissioning of Phase 1 of the Aeroton mega-bakery project is on track for mid-November 2025, with Phase 2 set for February 2026.

“This significant undertaking is expected to meaningfully enhance efficiencies and economies of scale and to fundamentally improve the quality of the bread Premier offers to its consumers in the inland region,” the company said.

Culverwell agreed with this, saying the construction of the bakery marks a major milestone and should be a significant margin driver for Premier.

He said that, with the Aeroton facility open, the company can consolidate its regional manufacturing footprint by mothballing its three older bakeries in Vereeniging, Old Pretoria and Potchefstroom.

This will lower the requirement to transport bread from other facilities to service the area, resulting in cost savings.

In addition, Culverwell said the new site is expected to drive improvements in bread quality and service levels, particularly in the informal channels, “which is a hotly contested area of the market”.

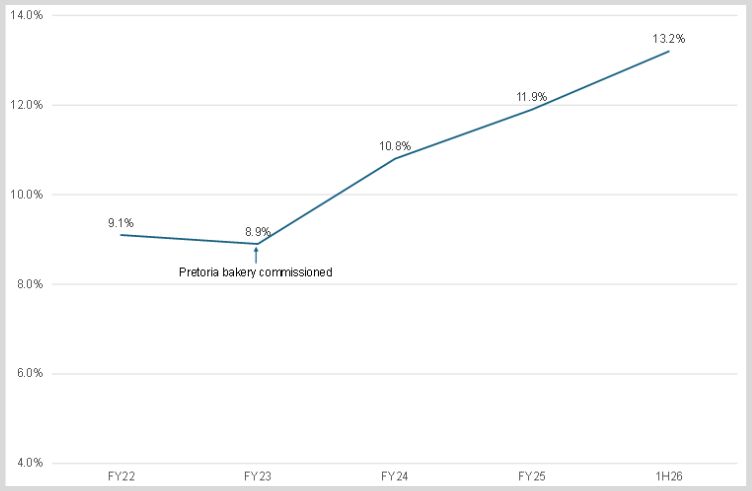

“Importantly, this is not Premier’s first mega-bakery. The group commissioned its Pretoria mega-bakery in 2023, and the benefits have been evident since,” he said.

The graph below, courtesy of Culverwell, shows the growth in the Premier’s EBIT margin following the construction of its first Pretoria mega-bakery.

The cherry on top

Another factor that makes Culverwell believe that Premier is set to shine is the company’s proposed acquisition of fellow food producer RFG.

RFG Holdings, previously known as Rhodes Food Group, specialises in convenience meal solutions and started as a canned fruit and jams producer in 1896.

Since then, the group has grown into a multinational food producer that packages premium private label product ranges for key retailers and houses well-known brands like Rhodes and Bisto.

In mid-October 2025, Premier announced that it had entered into a deal to buy all of RFG’s issued ordinary shares, excluding those held by RFG or its subsidiaries.

This deal, if approved, will result in the merger of two of South Africa’s oldest companies.

Culverwell explained that, while the acquisition of RFG is still subject to approval, management is confident the deal will be closed by the end of March 2026.

“We believe the deal makes both strategic and financial sense,” he said, explaining that the acquisition could address two of Premier’s major weaknesses.

He explained that two longstanding concerns in the Premier investment case have been limited liquidity in its shares and concentration risk to Millbake.

“Consolidating RFG addresses both, while also providing immediate earnings accretion,” he said.

“The industrial and route-to-market synergies between the two companies are obvious on paper, but such benefits are often difficult to deliver in practice.”

However, he noted that CEO Kobus Gertenbach and his team have given shareholders little reason to question their execution.

“With the commissioning of Aeroton in November, Premier effectively concludes its Millbake capex cycle,” Culverwell said.

“The RFG deal is a share swap, so rising cash on the balance sheet presents an opportunity for management to raise the dividend payout ratio or execute on the authorised share buyback programme.”

“Both of which would be the cherry on top of what is an already enticing investment case.”

Comments