Nedbank’s forgotten powerhouse going from strength to strength

Nedbank MFC continues to grow its market share in vehicle financing, despite the rise of used cars being sold through WeBuyCars and the rapid growth of Chinese brands in South Africa.

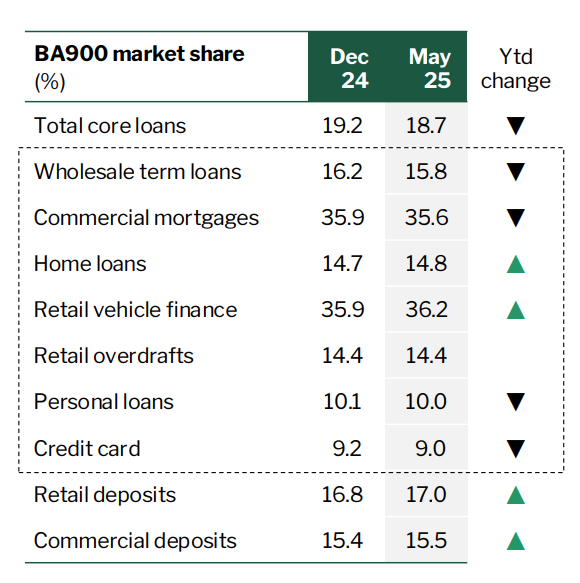

The division grew its market share to 36.2% of the market over the last six months, the bank revealed in its interim results.

This makes it the largest player in this segment, which is highly lucrative given the strong growth in new car sales so far in 2025 and the relatively high barrier to entry.

Vehicle financing is different from other forms of retail lending in that it is conducted through a dealer and not directly extended to an individual.

This makes it difficult for new entrants to break into the market, as existing players have relationships with dealers.

For example, South Africa’s premier digital bank, Discovery Bank, has repeatedly said it has no plans to move into vehicle financing as its behavioural model is centred around individual behaviour, limiting its ability to offer a unique service.

Capitec has moved into vehicle financing but has made a point of lending to individuals directly when they buy used cars rather than trying to break into the new car market.

One of the more major threats to Nedbank MFC has been the rise of used car sales in South Africa, with the strong growth of WeBuyCars due to the affordability of used cars in comparison to new models.

This has also been coupled with a rise in Chinese vehicles, which do not have a pre-existing dealership network or relationship with banks, posing a threat to existing financiers.

However, Nedbank CFO Michael Davis told Daily Investor that the MFC division continues to show strong growth despite these challenges and macroeconomic headwinds.

“We currently hold a 36% market share in the vehicle financing segment, and we have continued to take market share in the past year,” Davis said.

“We have gotten a lot of questions around new versus used and around Chinese new vehicles coming into the market and the impact those trends would have on our financing.”

“To answer those questions, we have grown market share effectively, where we have been comfortable to grow share in vehicle finance.”

This indicates that Nedbank MFC is going from strength to strength, with it being one of the few areas in which the bank managed to grow its lending market share. This can be seen in the graph below.

Impact of lower interest rates

Davis expects demand for new cars to begin to grow as the effect of lower interest rates play out in the coming months.

However, he warned that the business is currently experiencing higher impairments than expected in the MFC’s back book.

“In terms of the performance of the business, we have seen higher levels of impairments, not in the front book, but those that relate to the back book,” Davis said.

“We expect these to ease into the second half of the year as consumers experience the benefit of higher real income from lower inflation and interest rates.”

Davis explained that it takes around 18 months for the effect of lower interest rates to play out through the economy, with lending gradually picking up.

Much of the benefit from consumer spending has come from lower inflation, which translates into faster-growing real incomes.

He said faster-growing real incomes and lower interest rates will improve the economies of the motor vehicle finance business in the second half of the year.

“We are coming off the tail end of an interest rate hiking cycle from 2021, with prime rates peaking at 11.7%%,” he said.

“We have seen rates be cut by 50 basis points in 2024, followed by 75 basis points in 2025. Typically, it would take 18 months before this translates into a positive impact on impairments.”

“So, we should see the economics of that business improve into the second half of the year through a lower bad debt impairment number.”

While Nedbank MFC’s financial performance is set to improve, it is not clear whether Chinese brands will play a part in this.

Chinese brands may become victims of their own success. GWM and Haval compete in the same market segments, and as they grow, they risk eating into each other’s market share.

Another challenge has emerged in recent weeks, with the revelation that Chinese brands may not hold their value well in the second-hand market.

This is chiefly because their attractive engine warranties only apply to the vehicle’s original owner and are not transferable upon sale.

Comments