South African state bank is technically insolvent

The South African Postbank, a deposit-taking state-owned banking institution that aims to expand access to banking services nationwide, is technically insolvent.

The South African Postbank, closely tied to the Post Office, was founded in 1875 as a standalone entity known as the Savings Bank.

It opened its first branch in Cape Town in 1884, and it rapidly expanded to 125 Post Office branches across South Africa.

Despite using the Post Office’s footprint, the bank remained a standalone entity, and its name was changed to the Post Office Savings Bank.

It was only in 1974 that the Post Office took full responsibility for the Post Office Savings Bank and the National Savings Certificates when the bank was computerised.

The idea of it becoming a fully-fledged commercial bank, operated and owned by the state, emerged in the early 2000s, coinciding with the expansion of South Africa’s social grant system.

In 2003, the Post Office launched its Paymaster to the Nation project, which enabled recipients of social grants to open a Postbank account and receive their grants.

The bank offered its products and services through the Post Office, which has over 2,000 branches nationwide.

The government has long aspired to create a state-owned bank in South Africa to drive transformation in the financial sector.

While the Postbank has always offered minor banking services, it was strictly a savings subsidiary, unable to provide transactional accounts, credit, and other banking services.

With the Postbank Amendment Act in effect since March 2024, it can apply for a new banking licence from the Reserve Bank’s Prudential Authority.

This licence will allow the South African Postbank to become a fully-fledged commercial bank and compete against the likes of Capitec, FNB, Absa, and Standard Bank.

The bank said it would apply for the new licence in the past financial year, but no date has been set for its launch.

“The mission of Postbank is to be the trusted partner of the government in financial inclusion, and it aims to offer inclusive, accessible, simple and secure channels,” it said.

Its mission is to become the bank of choice for the government, business, and individual customers in the underserved communities.

The South African Postbank is technically insolvent

The state-owned bank has had numerous challenges and has failed to achieve clean audits over the last five years.

In the 2020 financial year, it had a qualified audit and, since then, has had disclaimers, meaning it provided insufficient evidence on which to base an audit opinion. In 2024, it received a qualified audit.

This is not where the problems end. It could not offer new products or grow its customer base, hampering transactional revenue growth.

It also suffered from a lack of requisite systems, IT instability, high vacancies, and a lack of banking skills and experience within the business.

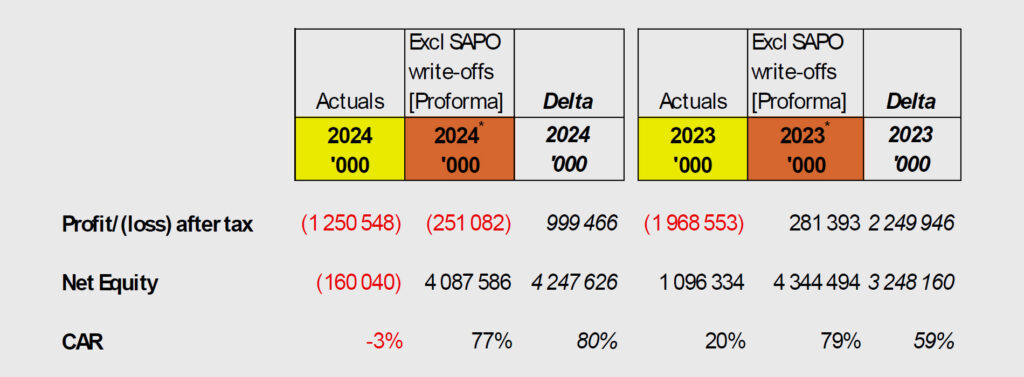

The South African Postbank’s financial report for the 2024 financial year further revealed that it has become technically insolvent.

The bank recorded a net loss of R1.25 billion for the year ended 31 March 2024, a decrease from the prior year’s net loss of R1.97 billion.

The South African Postbank’s revenue decreased by 3% from R2.17 billion in the prior year to R2.1 billion for the year ended 31 March 2024.

The bank has a significant problem in containing costs, as its cost-to-income (CTI) ratio stands at 166%, significantly higher than the targeted 92%.

It stated that the high CTI was primarily driven by an increase in costs related to the SASSA MSA, which included costly channels such as Cash Pay Points (CPP) and Over-the-Counter (OTC).

The after-tax loss of R1.25 billion, primarily due to additional credit losses, pushed the bank’s net equity into negative territory at year-end.

A technically insolvent company cannot settle all its liabilities if all its assets are liquidated. If left unchecked, it can lead to bankruptcy.

The negative equity means the bank is significantly undercapitalised, with a capital adequacy ratio (CAR) of -3.01% as of March 2024, well below the minimum required of 29.5%.

The South African Postbank’s declining capital adequacy ratio and failure to meet minimum requirements are putting its banking license at risk.

Correction: The article previously stated that Innocent Hlungwani was the Postbank CFO. However, he resigned from the position at the end of June 2024. Martin Dowie is the current CFO.

Postbank performance

Comments