South African banks opening the taps

South African banks significantly increased their credit extension to households and companies towards the end of 2024 as interest rate cuts helped improve consumer affordability.

The Reserve Bank’s latest Quarterly Bulletin for the fourth quarter of 2024 outlined key trends within South Africa’s financial services sector.

One of the key shifts noted by the bank is the uptick in loans and advances extended to South African households and businesses, marking a big change from the previous year.

Throughout 2023 and the beginning of 2024, loan growth was subdued in South Africa as interest rates were raised to 15-year highs to curb inflation.

These elevated interest rates resulted in a sharp rise in the number of clients who could not afford to take on more debt.

While demand for credit was strong, banks were unable to extend it to clients as financial pressure from inflation and interest rates began to weigh on South Africans.

Elevated interest rates typically benefit commercial banks as the interest margin on their extended loans improves, enhancing profitability.

However, after an extended period of high interest rates, these banks are hit with rising credit impairment charges and bad debt.

This forces them to raise provisions to cover non-performing loans, impacting profitability.

By the end of 2024, the picture had changed significantly, with inflation plunging to around 3% and interest rates being cut by 50 basis points in the second half of the year.

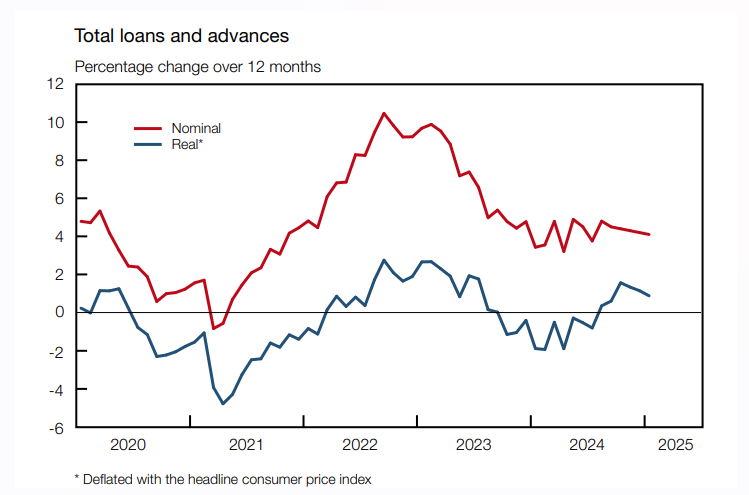

Thus, the Reserve Bank flagged an increase in year-on-year growth in total loans and advances from a low of 3.2% in April 2024 – the lowest rate since 2021 – to 4.1% in January 2024.

Crucially, with inflation substantially lower, this resulted in the growth of credit extension being positive in real terms for the first time in nearly a year.

In real terms, total loans and advances increased year over year from August 2024 after 10 consecutive months of contraction.

This can be seen in the graph below, courtesy of the Reserve Bank.

Big corporates leading the way

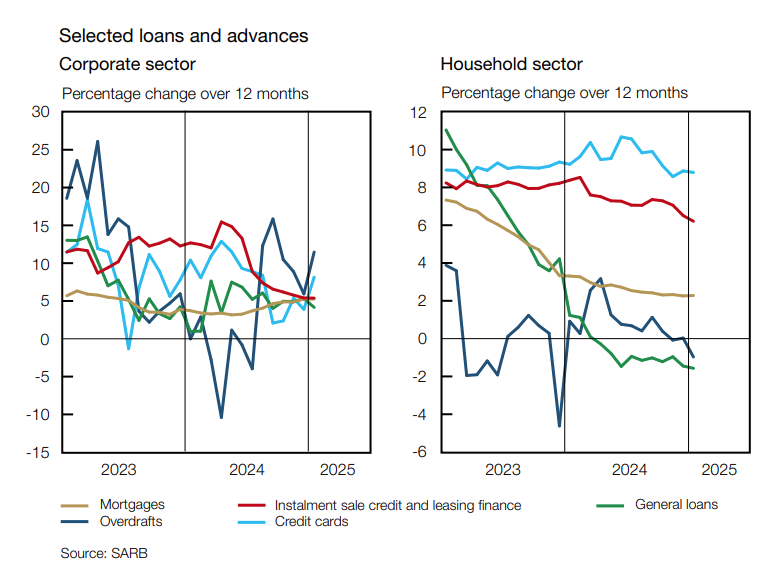

The Reserve Bank’s report also flagged a trend of lending to businesses far outpacing that to households, despite it slowing slightly in recent months.

Total loans extended to companies in 2024 grew by 4.8%, compared to only 3% for credit extended to households, the lowest rate since February 2021.

This is in line with comments from some of South Africa’s largest banks, with these institutions looking to grow lending aggressively to businesses as households remain under affordability pressures.

In its annual results for the past financial year, Standard Bank noted a reduction in non-performing loans and a slowdown in clients entering delinquency.

This has translated into declining credit impairment charges and an improved credit-loss ratio.

“The consumer in our retail business has started to improve, with the number entering early delinquency reducing in the last year. This is a huge, huge positive,” former Standard Bank Deputy CEO Kenny Fihla told Daily Investor after the company’s results.

“We have also seen the distress book coming down marginally, which is also a positive for our clients and for us.”

This means that clients are able to afford more credit and take on additional debt, and, crucially, Standard Bank can meet this demand.

“So, clearly, there are opportunities for us to start being slightly more aggressive from a lending point of view,” Fihla said.

“But, we have to do that in a well-thought-through manager in those sectors that are driven and supported by growth and in areas where we think there will be high quality.”

“We think that our Corporate and Investment Banking (CIB) business will continue to drive the growth of our asset base, with a focus on energy and infrastructure.”

Fihla explained that there is a significant demand for credit in this area. Due to the nature of its CIB unit and its clients, it is very high-quality, with minimal non-performing loans and reduced risk.

“There is also a strong demand for credit growth from our business and commercial banking unit. Here, we need to jack up our own credit management practices,” he said.

“But even then, it is not going to be wholesale lending. It will be targeted and focused on the areas that offer the most growth opportunity.”

“It will be done in a well-thought-through manner in those sectors that are driven and supported by growth and in areas where we think there is going to be large investment either by the government or the private sector.”

“So, it is going to be widespread, but led in the main by our CIB business.”

Comments