South African banks set to open the taps

Credit extended to South African households and businesses are set to grow significantly in the coming months as the effect of interest rate cuts begins to filter through the economy.

This is feedback from Standard Bank chief economist Goolam Ballim, who outlined his macroeconomic projections for South Africa at the bank’s annual Economy event in February.

One of the clear trends Ballim flagged was improving perceptions of the South African economy and, crucially, personal finances.

At the beginning of 2025, more South Africans expect the local economy to perform better in the short term and anticipate better personal financial conditions.

The effects of this can already be seen in improving retail sales data and increased new car sales towards the end of 2024 and in January 2025.

Ballim said this trend is expected to continue, with declining interest rates expected to increase disposable income and consumer spending.

This marks a significant shift from the previous two years, where household spending came under pressure from elevated interest rates.

From November 2021 to the middle of 2023, the Reserve Bank raised rates by a cumulative 475 basis points, significantly increasing the cost of debt and taking money out of consumer pockets.

The bank kept rates at a 15-year high for a full year before beginning its cutting cycle with a 25 basis point cut in September 2024.

As a result of these elevated interest rates, some banks tightened their lending criteria, while others saw a decline in affordability for new loans as consumers failed to meet their lending standards.

This resulted in credit extension to the private sector, particularly households and small businesses, slowing down significantly.

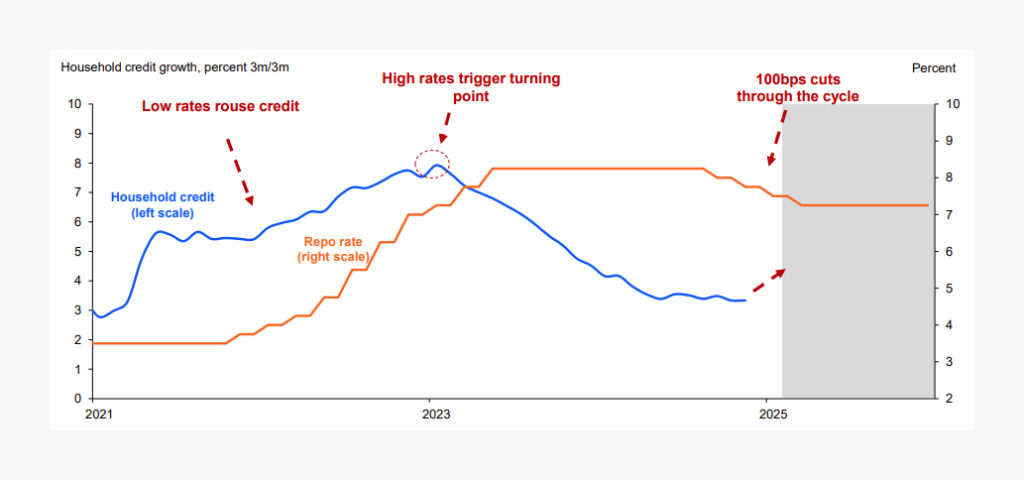

Data from the Reserve Bank showed just how steep the drop in credit extension was, with growth slowing from 9.9% year-on-year in February 2023 to a mere 3.2% in April 2024.

This was the lowest growth rate since October 2021, when South Africa was still coming out of pandemic-era lockdowns.

The sharp decline in household credit growth can be seen in the graph below, courtesy of Ballim.

As the graph also shows, Ballim expects household credit growth to pick up throughout 2025.

Interest rates have been reduced by a cumulative 75 basis points since September 2024, which should translate into banks extending more credit and more individuals meeting affordability criteria.

The reason why household credit growth has not increased as yet is the effect of interest rate changes lags behind the announcement of hikes or cuts by around six months.

As the effects filter through the economy, Ballim expects household credit growth to pick up.

Another driver of the increase in household credit growth is that government borrowing is expected to remain elevated.

As South African banks are already heavily exposed to government debt, they are likely to begin to push domestic savings to the private sector rather than increase exposure to the state.

Should the recent improvement in foreign investor sentiment towards South Africa persist, the reliance on the domestic financial system to fund the fiscal deficit could decrease.

The improved economic growth outlook could also create more investment opportunities for non-banking institutions within the private sector.

However, Ballim warned that credit extension growth is unlikely to reach pre-pandemic levels as interest rates are likely to settle above the rate seen in 2019.

He expects only one more interest rate cut before the bank holds the repo rate steady for some time as financial markets digest the beginning of Trump’s second term and the domestic growth picture becomes clearer.

Old Mutual chief economist Johann Els is more upbeat and believes that the Reserve Bank will have room to cut rates two more times in 2025 by 25 basis points each.

Els explained that South Africa is experiencing such low inflation that it can absorb this shock without having to put interest rate cuts on hold.

This does not mean inflation will not rise. It will not breach the midpoint of the Reserve Bank’s 3% to 6% target range and push it to put rate cuts on hold.

Comments