South African banks opening the taps

Credit extension to households and companies in South Africa is gradually picking up as improved sentiment and lower interest rates spur growth in loans and advances.

South African banks have kept a tight lid on loans growth in recent years as rising interest rates resulted in a significant jump in bad debt.

Commercial banks typically benefit from higher interest rates as their margins improve on existing loans, increasing revenue and profit.

However, as rates stay higher for longer, this positive tailwind can quickly turn as consumers come under increasing pressure and cannot pay back their debt.

This translates into higher credit losses for banks and a rise in bad debt that they have to cover by raising provisions, impacting profitability.

To mitigate against this, some banks tightened their lending criteria, while others saw a decline in affordability for new loans as consumers failed to meet their lending standards.

This resulted in credit extension to the private sector, particularly households and small businesses, slowing down significantly.

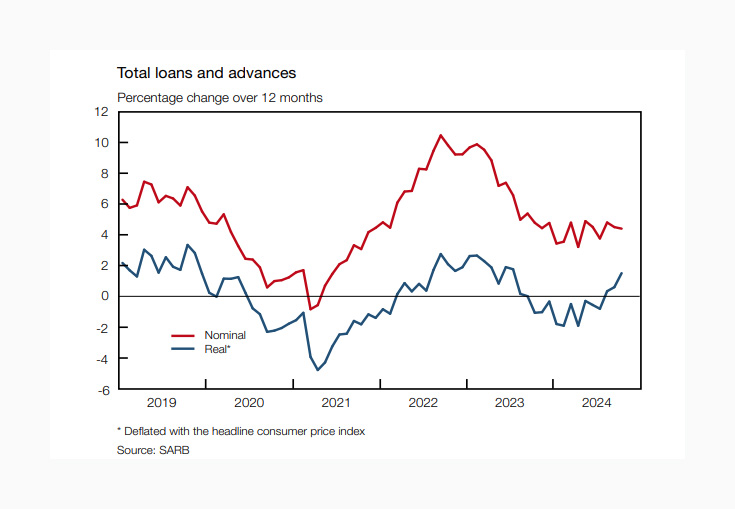

Data from the Reserve Bank showed just how steep the drop was in credit extension, with growth slowing from 9.9% year-on-year in February 2023 to a mere 3.2% in April 2024.

This was the lowest growth rate since October 2021, when South Africa was still coming out of pandemic-era lockdowns.

Growth in credit extension averaged 4.2% in the first ten months of 2024, well below the averages of 7.5% and 7.4% recorded over the same period in 2022 and 2023, respectively, the Reserve Bank said in its latest Quarterly Bulletin.

However, this rate has begun to tick up, with the growth rate in September and October reading 4.4% and 4.5%, respectively.

The bank said that credit extension is growing particularly strongly in the corporate sector as banks remain weary of extending further credit to South African consumers under immense financial pressure.

Crucially, after ten successive months of contraction, growth in real loans and advances expanded by 0.6% and 1.5% in September and October 2024, respectively.

This was due to growth in nominal loans and advances marginally outpacing growth in consumer price inflation.

The shift from negative territory to positive growth can be seen in the graph below.

The Reserve Bank said there are a few reasons why the uptick in credit extension to the private sector is expected to be sustained.

It explained that as government borrowing is projected to remain elevated, the risk of further increases in the financial sector’s exposure to the sovereign is high.

This is likely to begin to push some banks to shift domestic savings to the private sector rather than increase exposure to government debt.

Should the recent improvement in foreign investor sentiment towards South Africa persist, the reliance on the domestic financial system to fund the fiscal deficit could decrease.

In addition, a reduction in credit risk due to declining interest rates and an improving growth outlook may encourage banks to extend more credit to the private sector rather than purchasing government bonds.

The improved growth outlook could also create more investment opportunities for non-banking institutions within the private sector.

CEOs of two of South Africa’s largest lenders, Standard Bank and Capitec, have expressed that they are beginning to expand their lending portfolios more aggressively.

Speaking to Daily Investor after Standard Bank’s interim results, CEO Sim Tshabalala emphasised that the bank had not restricted its lending activities, noting that it applied consistent criteria to all clients over the past two years.

Tshabalala stated that the peak of bad debt in South Africa has passed, with consumers likely to benefit from declining inflation and interest rates in the coming months.

The combination of lower interest rates and increased confidence in the local economy is expected to drive growth in Standard Bank’s lending activities.

“So, in other words, we’ve seen the worst of it as interest rates decline, inflation declines, and consumer confidence improves. We should see a growth in the loan book.”

“The taps are open, and we are just waiting for more demand from individuals.”

Capitec CEO Gerrie Fourie has similarly indicated that the bank plans to grow its lending book in the coming year, citing opportunities arising from lower inflation and interest rates.

“We are happy with how we have handled the crisis and how agile we have been. We are fairly happy with the result,” Fourie said during the bank’s interim results presentation for the six months ending in August.

“We put tremendous effort into the collection side of things to ensure we could improve the collection with an entirely new system and help our clients during this time.”

Now, as inflation and interest rates ease, Capitec is loosening its lending criteria to meet growing consumer demand for credit.

“What we have done now actually is to open up, with loan disbursements in August being at R4.5 billion – one of our highest figures ever,” Fourie said.

“We believe there are opportunities given what we have seen with inflation and the economy. So, we are opening up in the credit space.”

Comments