The ‘new’ South African bank taking on the Big Four – and winning

Discovery Bank has managed to successfully crack into South Africa’s highly competitive banking sector, with it taking market share from incumbents to become profitable just seven years after launch.

For the bank to meet its ambitious growth targets for the coming few years, it will have to continue winning over clients from the traditional Big Four of Absa, Nedbank, Standard Bank and FNB.

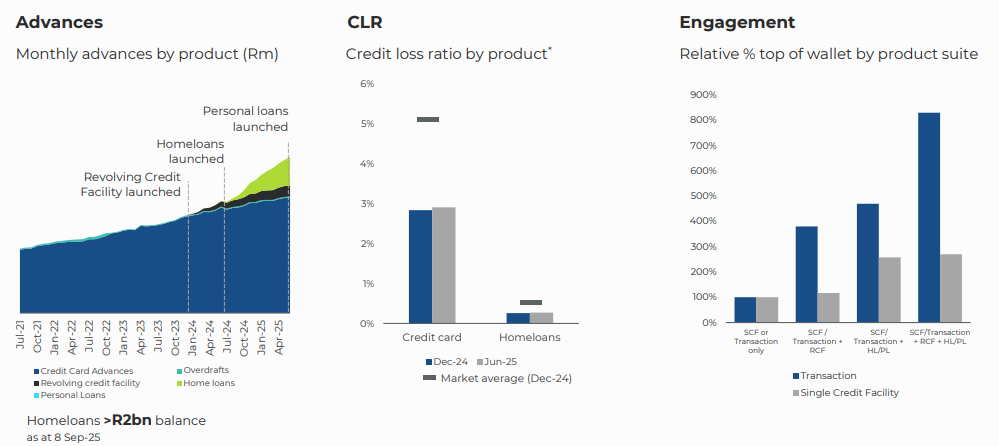

The bank has proven that it can win over clients, with its home loan offering growing rapidly since launch.

CEO Hylton Kallner previously told Daily Investor that 80% of all its home loans are “switches” by clients who had existing bonds with other banks.

Kallner has also explained that Discovery Bank has reached an inflection point whereby the majority of its new customers are completely new to the Discovery ecosystem.

This means the bank is now successfully competing in the market against the Big Four and other players, winning over existing clients and attracting new entrants to its offering.

Discovery CEO Adrian Gore recently explained that this is not something that happened overnight, with the bank’s offering being built over the past decade on four pillars.

Speaking at the bank’s product update earlier this month, Gore outlined these four pillars and how they have resulted in Discovery building a disruptive competitor to the incumbents.

“I remember well when we set out to build Discovery Bank, our ambition was clear – to build a bank that is unique and brilliant, that is built from the ground up,” Gore said.

Building a bank from scratch is no mean feat, with Discovery having spent around R15 billion on its bank. Some of its competitors have opted for the cheaper option of a white-label offering, which may limit service delivery and customisation in future.

“Our conviction was based on the relevance and importance of four fundamental pillars upon which Discovery Bank is based,” Gore said.

The first pillar is the extension of Discovery’s shared-value model into banking, by using Vitality Money to drive behavioural changes that improve financial outcomes.

This model incentivises and guides individuals to manage their money more prudently, improving their financial outcomes and reducing risk for the bank.

The bank is also a completely digital bank that has a limited physical presence, using technology to offer a private banking experience to a wide customer base.

This has proven immensely successful, with high-income clients who would traditionally be serviced by private banking offerings from the incumbents switching to Discovery Bank.

Part of this is Discovery Bank being able to be a full-service bank, offering products ranging from savings accounts to home loans. It is the only digital bank to offer a full suite of personal banking products.

The final pillar of Discovery Bank is to become the composite maker of all of the group’s products, with the banking app becoming the primary gateway for clients to interact with the Discovery ecosystem.

Currently, clients are able to see their products on the banking app, but not engage with them. The launch of car insurance on the app is the first step towards creating this Discovery “super app”.

Winning against the Big Four

Discovery Bank has ambitious growth targets for the next three financial years, with it aiming for R3 billion in operating profit by the end of the 2029 financial year.

Central to this continued growth is its home loans offering, which is set to greatly increase the size of Discovery Bank’s loan book.

Kallner and Gore have said that the bank does plan on growing its loan book aggressively in the coming years, leveraging the launchpad it has from nearly a decade of conservative growth.

Home loans are particularly attractive as individuals tend to have them with their primary bank. As a result, if you can switch a client’s home loan to your bank, you are likely to benefit from increased transactions, savings accounts, and additional loans from that client.

Kallner said Discovery Bank’s home loan book has managed to grow to over R2.2 billion in its first year of operations.

Crucially, the bank has proven its ability to win over clients with existing home loans, with the offering not being available to individuals without a Discovery Bank transaction account.

“The offering is still very much dominated by switches from clients with existing bonds. That is approximately 80% of the business and the loan book,” Kallner said.

This means that only 20% of the home loans offered by Discovery Bank are to individuals who do not have an existing mortgage.

Furthermore, Kallner explained that the switched client is, from Discovery Bank’s perspective, a lower-risk client for the bank.

“From our perspective, the switched client is obviously a much lower-risk client. The pricing that we are able to offer by understanding the client and the risk through our behavioural models has resonated,” he said.

Gore explained to Daily Investor that Discovery Bank has been able to grow rapidly without noticeably impacting South Africa’s incumbent banking giants.

However, this does not mean they are not taking the bank seriously as a competitor, with some incumbents overhauling their private banking business in recent years.

“To be fair to them and us, they have always given us credit for what we offer and for keeping an eye on our growth. So, we have not exactly come from behind unnoticed,” Gore said.

“They have always been unbelievably razor sharp in competing with us, and there is nothing new in that. But do they pose a risk? Of course they do. Our banks are excellent. They are a hell of a competitor.”

However, Gore believes that Discovery Bank has an edge as a new entrant to the market that is uninhibited by legacy issues.

“Other banks do have some technology issues at that scale or with their legacy systems. Some of that stuff is not easy to do. We have to continued to innovate, and there is no hubris at all from our side,” Gore said.

Comments