The South African company that doubled investors’ money in a year

Weaver Fintech, formerly HomeChoice International, has seen its share price more than double over the past year as its pivot towards financial services reaps handsome rewards for the company.

The company, now worth over R6.5 billion on the JSE, has seen demand for its fintech products surge in the past few years, with it now serving over 3.7 million customers.

Its name change from HomeChoice International to Weaver Fintech is a direct result of this, with the financial services business now contributing 92% of profit before tax.

The change was a long time coming, with the company first launching short-term lending products in 2007 to retail customers.

It gradually expanded its offering to include transactions using mobile technology in 2011. Over the next decade, fintech revenue surged.

As a result, in 2021, HomeChoice established Weaver Fintech to house its financial services offering and present it as a standalone business that offered products outside of HomeChoice’s network.

The business grew to comprise personal lending, payment solutions, value-added services, and insurance products on mobile platforms.

Weaver’s big break would come with its purchase of PayJustNow in 2021, which was then a digital payments start-up operating in the buy-now-pay-later (BNPL) space.

The rise of BNPL in South Africa in the aftermath of the Covid-19 pandemic saw PayJustNow’s customer base and revenue surge.

Over the most recent full financial year, PayJustNow added between 60,000 and 100,000 new customers every month. It is now the largest business of its kind in the country.

Weaver also owns FinChoice, which was created in-house by HomeChoice in 2007 to house its short-term lending business.

As a whole, Weaver adds around 130,000 new customers every month across BNPL, short-term lending, and its insurance business.

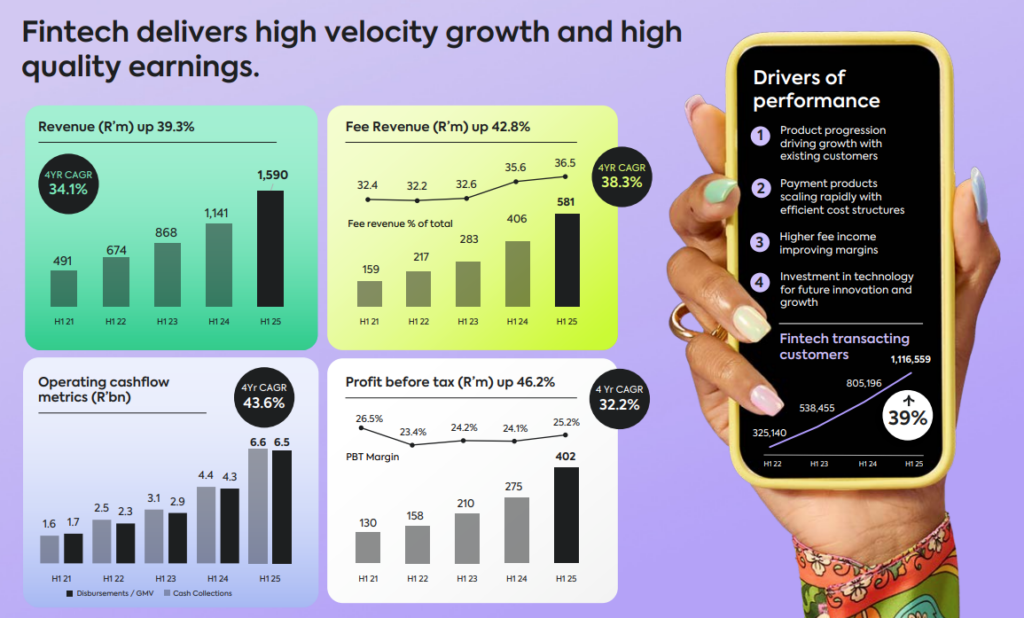

This growth has driven the company’s share price higher, with it crucially translating into a 29.4% surge in revenue to R2.6 billion in Weaver’s latest interim financial results.

Profit before tax skyrocketed by 48% to R370 million on the back of fee income growing by 47.2%. This now accounts for just less than a third of total revenue.

Weaver’s secret sauce

PayJustNow is the cornerstone of Weaver’s business, providing a large chunk of its customer base and driving its growth.

It is also the home of its secret sauce, with PayJustNow able to grow its business rapidly without a corresponding surge in non-paying customers.

In an interview with Daily Investor prior to Weaver’s name change, PayJustNow co-founder Craig Newborn explained how the company was able to do this.

Newborn explained that the company has plenty of runway to continue growing, with its eye on a bigger slice of South Africa’s 25 million credit-active individuals.

While the company’s growth rate is expected to continue for some time, it is not waiting for a slowdown to improve its customer mix.

PayJustNow has been able to keep its share of non-paying customers exceptionally low, hovering around 2% by implementing a behavioural scorecard to process approvals.

In contrast to its direct competitors, the company also gets customers to pay one-third of the price at checkout. Newborn said this provides a good entry barrier to its service, filtering out a large number of potential non-paying customers.

Newborn also explained the company’s interesting business model, which allows it to charge no fees or interest on payments.

The company only charges fees when payments are over 24 hours late, based on the customer’s chosen payment date.

The company makes very little money from these fees, which Newborn said are not even enough to cover the cash lost from its non-paying customers.

Therefore, most of PayJustNow’s income is generated by fees paid by the merchants who use its service to facilitate transactions and monthly payments.

Newborn said the company has ambitious plans to leverage this relationship with merchants to drive higher-quality earnings for the company.

This is referred to as Weaver’s fintech ecosystem, which is effectively a platform where merchants and customers can discover each other and customise financial solutions.

The ecosystem has expanded rapidly. The customer base grew 23.5% to 3.3 million, with the merchant base exceeding 3,100 as of the company’s latest interim results.

Weaver currently offers more than nine fintech products, with five additional launches planned for the second half of its 2025 financial year.

“The strength of our two-sided ecosystem lies in its powerful network effect. As we acquire more customers, merchants gain greater sales opportunities,” the company said.

“In turn, an expanding merchant network increases choice for customers, driving mutual growth. Merchants benefit from personalised solutions and ongoing engagement with a growing pool of active users.”

“We see a significant opportunity to deepen customer relationships through product cross-sell and increased ecosystem participation.”

Currently, 18% of active customers use two or more products, with the company having a long-term goal of reaching 50%.

This impressive growth and improving customer mix have caught the attention of investors, with Weaver’s share price more than doubling over the last year. This can be seen below.

Comments