South African homeowners are in serious trouble

Residential mortgage defaults continue to rise strongly in South Africa despite significant reductions in interest rates and inflation over the past two years.

This indicates that South African households are still under immense financial strain amid a stagnant economy and elevated unemployment.

The pressure South Africans are under is also reflected by the unwillingness of banks to lend to homebuyers, with mortgage growth being among the slowest of all credit extension in the country.

Banks are also significantly more willing to extend credit to companies rather than individuals, with credit card growth slowing in recent months.

The Reserve Bank’s latest Financial Stability Review outlines the financial pressure South Africans are experiencing.

It identified the increased financial distress seen in households and small businesses as one of the major threats to the stability of South Africa’s financial system.

“The combination of persistently low economic growth, high levels of unemployment and elevated debt-service costs continues to weigh on household finances,” the bank said.

“Real incomes have remained broadly stagnant in 2025, though lower inflation and interest rates have offered some relief, as evidenced by the decline in debt-service costs as a share of household income.”

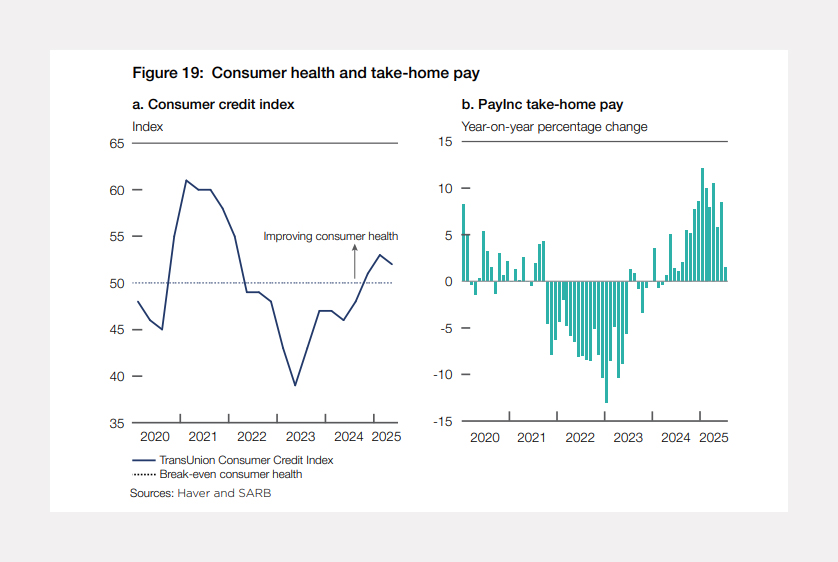

Despite a moderate decline in the first half of 2025, the TransUnion Consumer Credit Index confirmed an improvement in household credit profiles.

The index remained above the neutral 50-point threshold, suggesting that the moderation in credit activity is more reflective of tighter lending standards than a decline in consumer demand.

Although living costs are rising – particularly due to the sharp increases in electricity prices and municipal rates – higher real take-home pay since the fourth quarter of 2024 has mitigated some of the impact.

This points to some positivity for households in South Africa, with financial conditions easing. This can be seen in the graphs below.

Trouble remains

Despite the signs of improvement, the risk of financial distress among households remains elevated in South Africa, with data surrounding lending to households painting a dire picture.

The Reserve Bank highlighted lending data to show that households are still under immense financial pressure in South Africa.

Data regarding private sector credit extension has also indicated that banks are less willing to lend to households, as affordability remains a major issue.

This is despite a reduction in interest rates in South Africa since September 2024, which has provided significant relief to individuals with debt.

However, even with this easing, the number of consumers with impaired credit records remains stubbornly high.

While the ratio of impaired records to total credit-active consumers declined over the past quarters, this improvement is mainly due to a decrease in the number of credit-active consumers rather than a decline in impaired credit records.

This downward trend suggests that broader financial distress may be mitigated by more conservative lending practices by lenders, the Reserve Bank said.

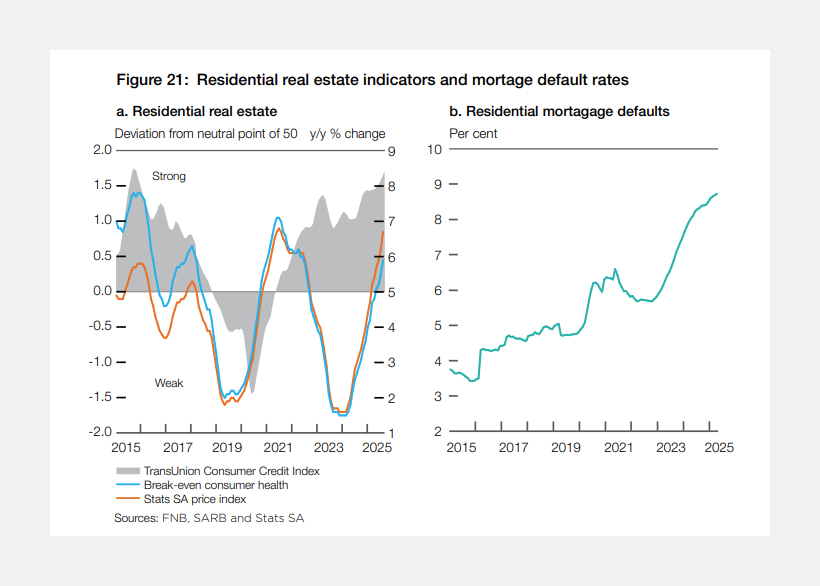

Where concern is most evident is in South Africa’s housing market, with both homeowners and those looking to buy property being in significant financial distress.

The residential property market continues to demonstrate resilience, as reflected by selected price and market strength indicators.

However, residential mortgage defaults have continued to trend upwards since the start of 2023 despite an easing in interest rates, which indicates ongoing financial strain among households.

Banks are also unwilling to extend credit to homebuyers, with household sector credit only growing by 3.1% year-on-year. This is substantially slower than corporate credit extent, which is in the double-digits.

“There are many components within that segment that are actually quite lacklustre, in particular residential mortgages. That growth rate is just above 2%,” Stanlib chief economist Kevin Lings said.

“That has been there for quite some time. In other words, we just do not have a vibrant housing market in South Africa. We are not seeing a significant expansion or the building of residential properties.”

Lings noted that this is also partly driven by the flat growth in housing prices in many parts of the country, excluding the Western Cape, which makes housing developments unattractive for companies.

“It is evident from the data that the housing market is not driving any of the credit growth in South Africa,” Lings said.

Comments