Bad news for South Africans who want to buy a home

Lending to South African households and companies grew strongly in October, but credit extension to households remains subdued.

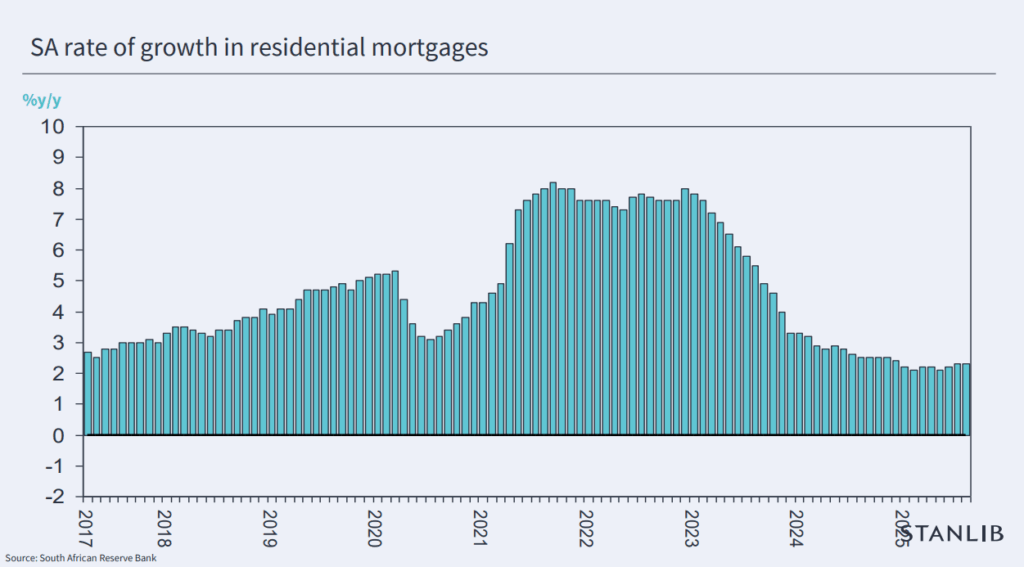

In particular, residential mortgage advances increased by just over 2% year-on-year in recent months, indicating that banks are pulling back on home loans in South Africa.

On the other hand, banks remain willing to extend credit to businesses, particularly in respect of financing alternative energy projects and other infrastructure investments.

Stanlib chief economist Kevin Lings outlined the strong growth in private sector credit extension and the unwillingness of banks to extend credit to households.

In October, private sector credit extension grew by 7.3% year-on-year, which is a substantial acceleration from 6.1% in September and is above market expectations.

This indicates that banks are increasingly willing to extend credit amid improving confidence in the local economy and faster growth.

Banks will also be more willing to extend credit due to the steady reduction in interest rates in South Africa, with inflation coming down to hover between 3% and 4%.

The Reserve Bank has cut interest rates by 150 basis points over the past 12 months, which has made credit significantly more affordable for many South Africans.

“If we break down this reading further, it becomes clear that this growth in credit is not being driven by households and individuals,” Lings said.

Household sector credit is only growing at 3.1% year-on-year, substantially slower than corporate credit extension.

“There are many components within that segment that are actually quite lacklustre, in particular residential mortgages. That growth rate is just above 2%,” Lings said.

“That has been there for quite some time. In other words, we just do not have a vibrant housing market in South Africa. We are not seeing a significant expansion or the building of residential properties.”

Lings noted that this is also partly driven by the flat growth in housing prices in many parts of the country, excluding the Western Cape, which makes housing developments unattractive for companies.

“It is evident from the data that the housing market is not driving any of the credit growth in South Africa,” Lings said.

Slow recovery

There are signs of a slow recovery in South Africa’s housing market, with prices rising and buyer confidence returning amid strong first-time buyer demand.

Pam Golding Property Group CEO Dr Andrew Golding said South Africa’s housing market recovery remains firmly on track, despite slowing mortgage lending growth.

The market is continuing to build momentum amid sustained positive sentiment. “National house price inflation is also gaining ground, rising to 4.2% in August 2025, according to the revised Pam Golding Residential Property Index,” Golding said.

“Encouragingly for investors and existing homeowners, subdued consumer price pressures supported real (inflation-adjusted) house price growth of 0.9% in August, marking six consecutive months of positive gains.”

By price segment, the upper band above R3 million posted the strongest growth at 5.5% in August. This was followed closely by the R2 million to R3 million band at 5.4%, while homes priced below R1 million rose by 3.3% over the same period.

“A broad-based recovery is also evident across South Africa’s major metro markets, with Cape Town leading the pace and Tshwane spearheading the rebound in Gauteng,” Golding said.

“The coastal price premium continues to widen, while freehold properties are registering a slightly stronger recovery in prices than sectional title units.”

Golding added that market activity remains sustained across regions and price bands, including the luxury segment, highlighting renewed buyer confidence.

Even during the typically quieter winter months, the property market in areas like Cape Town’s Atlantic Seaboard remained hot.

In June 2025, Pam Golding reported a record sales turnover of R240 million in the Atlantic Seaboard for that month alone.

“In-demand locations, particularly those offering strong lifestyle appeal, continue to attract buoyant activity, underpinned by semigration trends and access to competitively priced finance,” he said.

Golding explained that the property market’s resilience is all the more notable against the backdrop of a subdued economy.

Comments