South Africa’s newest banks are hiding in plain sight

Retailers are issuing credit at a far faster rate than South Africa’s traditional banks, as consumers are increasingly turning to alternative sources of credit.

While banks still hold by far the biggest share of the local credit market, retailers are rapidly growing their share of the financial services market.

A growing number of retailers are also expanding or launching their own banking offerings, posing a notable threat to traditional lenders’ market share.

FNB’s latest Economics Weekly showed that banks continue to dominate the local credit market, holding 78.6% market share.

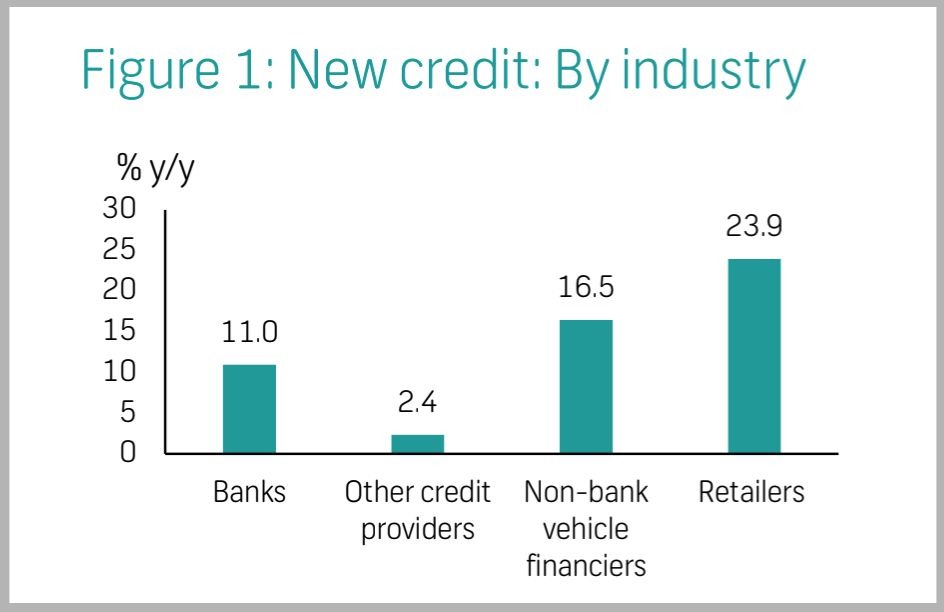

Banks issued R122.7 billion of the total R156.1 billion new credit issued in the third quarter of 2025. This marks an 11% year-on-year increase.

However, retailers recorded by far the fastest growth, with new credit issued up 24% year-on-year, double that of banks, to reach R12.2 billion.

This lifted retailers’ share of the market to 7.8%, which FNB said reflects the rising popularity of in-store credit, driven by discretionary and durable goods purchases.

Aside from retailers, other alternative credit issuers also showed strong growth. For example, non-bank vehicle financiers expanded significantly by 16.5% year-on-year to R11.5 billion.

Other providers grew more modestly by 2.4% to R9.7 billion. This segment includes pension-backed lenders, developmental lenders, micro-loan lenders, agricultural lenders, insurers, non-bank mortgage lenders and securitised debt.

These trends come as non-bank lenders, particularly retailers, are increasingly looking to grow their share of the local credit market and expand into the financial services sector.

Major retailers like Shoprite and Pepkor, for example, have either grown their banking capabilities in recent years or are looking to launch banks.

This presents a notable threat to South Africa’s biggest banks, as these retailers have the ability to tap into their extensive physical store network and millions of existing customers who interact with the company on a regular basis.

The growth in retailers’ new credit issuance compared to banks in the third quarter of 2025 is shown in the graph below, courtesy of FNB.

Shoprite and Pepkor

South Africa’s biggest retailer by market cap, Shoprite, has steadily been growing its banking capabilities over the past few years, evolving from a simple Money Market account in 1998 to a fully-fledged bank in 2020.

Now, the retailer has announced plans to dominate South Africa’s money transfer market before mounting a full challenge to the country’s traditional big banks.

Shoprite is well on its way to achieving this, with its offering already having attracted four million customers since 2020.

The retailer has a significant advantage over other companies, as its services are used almost daily by customers and it boasts an extensive footprint of “branches” through its over 2,800 retail stores across the country.

Shoprite, in particular, also has unparalleled access to underserved segments in the country’s banking market, as its extensive store footprint includes locations in small, remote communities.

This means the retailer’s outlets are often the only safe payout points for people who rely on money sent by family working elsewhere.

These transfers, from account to account or counter to counter, form the foundation of Shoprite’s financial services offering and are the base from which it plans to expand into banking.

Pepkor is another key company for traditional banks to keep an eye on, as the retailer is also looking to launch a banking offering in the coming years.

With a reputation as the largest retailer in southern Africa by store footprint, with nearly 6,000 stores, Pepkor could become a formidable force in South Africa’s banking industry.

The retailer has already seen some success in the financial services market, with its fintech segment having increased its revenue by 31.1% to R16.6 billion in Pepkor’s 2025 financial year.

This strong growth was driven by a 61.4% increase in financial services revenue and a 13.7% rise in its Flash business, which provides payment solutions to small businesses, including informal market traders.

Pepkor’s fintech segment already constitutes 15% of the retailer’s revenue, and its 6,000-store footprint makes the company a potentially strong competitor in the banking space.

Bloomberg reported that the retailer is considering plans to open bank branches in South Africa that offer zero-fee services, using its extensive store network to reach millions of lower-income customers.

The publication explained that by opening this offering, likely to be called Pep Bank, within its existing stores, the retailer can roll branches out quickly and attract customers who already frequent its outlets.

It can also leverage the substantial data it has collected on customers to more effectively tailor its financial product offerings.

Comments