Good news about interest rates in South Africa

South Africa’s real interest rates are relatively high, yet they are not so high as to be crushing domestic demand for credit.

The country’s slow economic growth is predominantly due to supply-side issues relating to deteriorating infrastructure, which is limiting the production and sale of goods and services.

Despite this, interest rates are likely to come down further over the next year as they remain elevated on a real basis.

As inflation continues to surprise on the downside, there is a risk that interest rates become too high and constrain economic growth.

Symmetry chief investment strategist Izak Odendaal recently explained how one can assess whether interest rates are too high in South Africa.

Odendaal said there are two main approaches to assessing what the ‘right’ interest rate is for a country based on its inflation and economic growth.

Most typically, economists would model a ‘real neutral rate’, which is a theoretical interest rate where supply and demand are nicely balanced.

At this rate, the economy is neither running too hot nor too cold, with inflation under control and interest rates not overly restrictive on economic growth.

Odendaal said this rate is also known as the ‘goldilocks rate’, given the assumption that it is “just right” for an economy.

Once this rate has been modelled, one can compare it to the current real repo rate of just less than 4% to see whether the Reserve Bank’s current stance is restrictive or accommodative.

The real repo rate is calculated by removing inflation from the Reserve Bank’s repo rate, which currently stands at 7%.

The Reserve Bank estimates South Africa’s goldilocks rate to be just below 3%, which indicates that its current policy stance is restrictive.

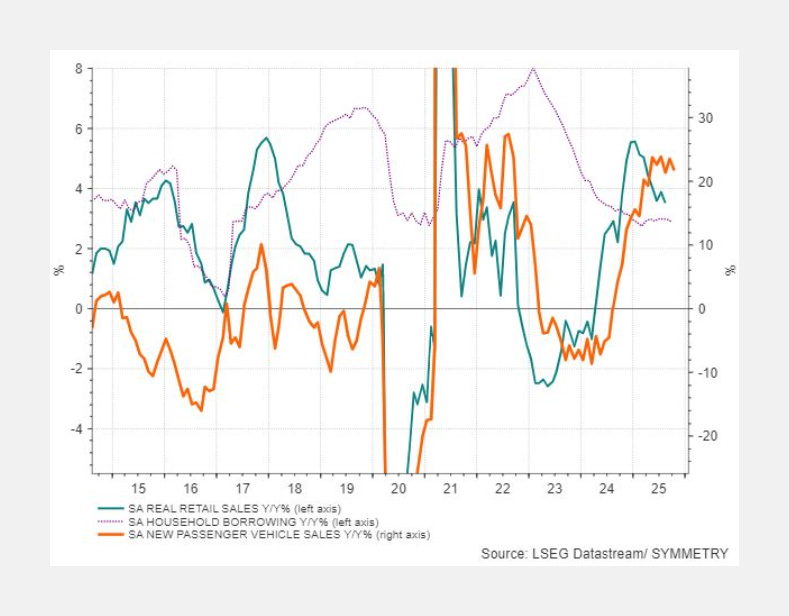

However, Odendaal said this method does not provide a complete picture, with an analysis of interest-rate sensitive sectors of the economy also proving informative.

If interest rates are too high, consumer spending and borrowing will plunge. Spending and lending will boom if rates are too low.

Odendaal said he prefers the latter as it is practical in measuring the impact of interest rates on the economy and consumer behaviour.

Looking at interest-rate sensitive sectors of the economy, it seems as though interest rates are high, but not high enough to constrain economic activity.

This approach shows that rates were too high in 2022/23, but following the Reserve Bank’s cutting cycle in 2024 and 2025, there has been a significant uptick in retail and new car sales.

However, household borrowing, which is mainly home loans, is only growing at 3% and is proving extremely slow in its recovery.

As a result, Odendaal said it is a mixed picture, with rates being higher and likely to decline further next year, but not so high as to be crushing domestic demand.

Interest rate cuts coming

With the Reserve Bank’s current policy stance being restrictive, it is likely to cut interest rates by 50 basis points over the next year.

As inflation continues to surprise to the downside, the Reserve Bank may cut interest rates significantly despite its implicit lower inflation target of 3%.

The likelihood of interest rate cuts is increased by the fact that the US Federal Reserve is set to cut interest rates further to boost the world’s largest economy.

This gives the Reserve Bank more room to cut interest rates in South Africa, as it will limit the potential impact on the rand.

Coronation’s head of fixed income, Nishan Maharaj, explained that while the expected 50 basis points in cuts is lower than some market expectations, it will still provide a substantial tailwind for local bonds and growth.

Maharaj explained that inflation has repeatedly surprised to the downside due to weak demand-side pressure and softer food prices and rental inflation.

He said this has resulted in the market pricing in expectations of 100 basis points of further cuts before settling in at 50 basis points over the next year.

“We expect the peak in inflation to be at 4% (previously at 4.5%) in the first quarter of 2026, which we believe will give the Reserve Bank room to ease interest rates a further 50 basis points over the next year,” Maharaj said.

He explained that Coronation still expects inflation to average 4% over the next two years. Despite this, the real interest rate in South Africa remains restrictive at over 2.5%.

Any further downward surprise in inflation will make this rate increasingly restrictive and potentially unnecessarily so.

Stanlib chief economist Kevin Lings explained that it is possible for interest rates to be cut in November, but that the meeting may come too soon.

“The latest inflation data should further encourage the Reserve Bank to consider cutting rates by a further 25 basis points before the end of the year – despite its 3% inflation goal,” Lings said.

“A cut of 25 basis points would not be in complete conflict with the recent downward revision to the Reserve Bank’s inflation objective of a sustained 3%.”

Inflation expectations in South Africa have declined over the past few months, with any downward surprise in inflation likely to bring them lower.

However, Lings said the Reserve Bank may be concerned about letting inflation drift further away from its preferred 3% target.

As inflation rises, albeit slowly, away from that target, it will make it more difficult to bring it back down in future. This will likely result in interest rates remaining higher for longer.

Comments