Government’s big VAT win

South Africa’s government has collected significantly more revenue from value-added tax (VAT) in the current financial year than expected in the Finance Minister’s May Budget Speech.

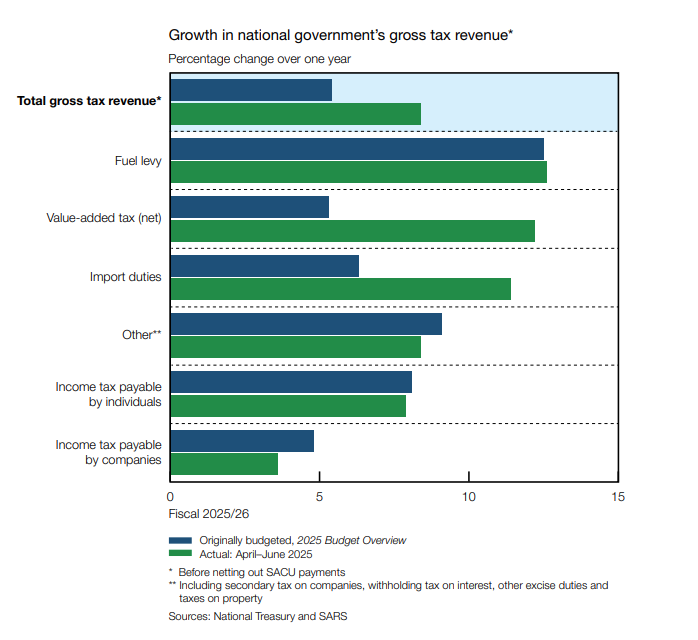

Data in the Reserve Bank’s latest Quarterly Bulletin shows that VAT receipts are up 12.2% year-on-year, compared to an expected increase of 5.3%.

This means the government has collected R106.2 billion from VAT in the first quarter of the financial year. The National Treasury expects full-year receipts to be R482.2 billion.

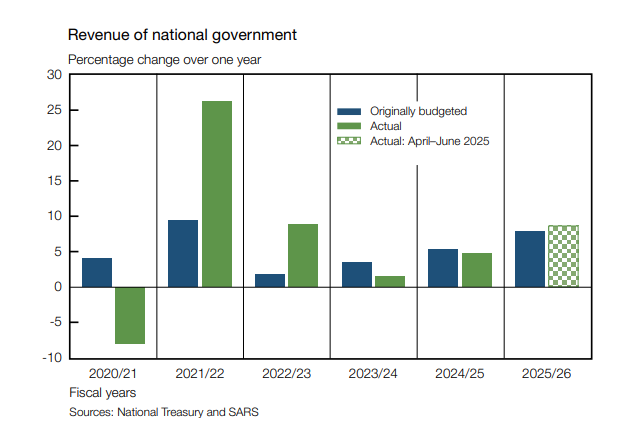

The increase in VAT receipts has played a role in the government’s tax revenue being ahead of target for the year so far.

It also appears as though this strong revenue performance has continued in recent months, with receipts for August up 11.4% year-on-year.

The strong increase in VAT collections is despite the Finance Minister’s initial two-percentage-point increase in the tax rate not going through due to stiff opposition from within the Government of National Unity (GNU).

Stanlib chief economist Kevin Lings explained that the increase in VAT collections is largely due to a decrease in VAT refunds.

This is a result of SARS taking a stricter stance on VAT refunds and a reduction in the time period for submitting the refunds.

The National Treasury is relying heavily on SARS to increase revenue collection in a stagnant economy by closing South Africa’s estimated R800 billion tax gap.

This gap is the difference between the value of taxes levied and those actually collected in South Africa, which has ballooned over the past decade as SARS’ capacity was gutted during the state capture era.

SARS has proven effective so far in squeezing more revenue from a stagnant economy, with personal income tax (PIT) revenue also rising substantially so far in 2025.

PIT revenue rose by 7.9% year-on-year during the first quarter, with the growth accelerating to 8.4% year-on-year in August.

Corporate income tax growth remains subdued, but is expected to pickup due to the rise in commodity prices translating into greater profits for local mining companies.

An increase in the general fuel levy has seen revenue from this tax rise by 12.6% year-on-year, with the government expecting to collect R96.6 billion from this source in the 2025 financial year.

The table below, courtesy of the Reserve Bank, shows the year-on-year growth in tax revenue during the first quarter of the government’s financial year year compared to the full-year projections in the May Budget Speech.

Tight lid on spending

Crucially, government expenditure is below budget as the National Treasury has managed to keep a tight lid on spending increases.

This should translate into a larger primary budget surplus than initially expected, supporting the Treasury’s efforts to stabilise the government’s debt burden in the current financial year.

A primary budget surplus occurs when the government collects more in tax revenue than it spends, excluding debt-servicing costs.

As a result, a primary budget surplus should, over time, result in debt growth slowing and stabilising as a share of GDP.

The Reserve Bank’s data currently points to a primary budget surplus worth 1% of GDP, greater than the 0.8% projected in the Budget Speech.

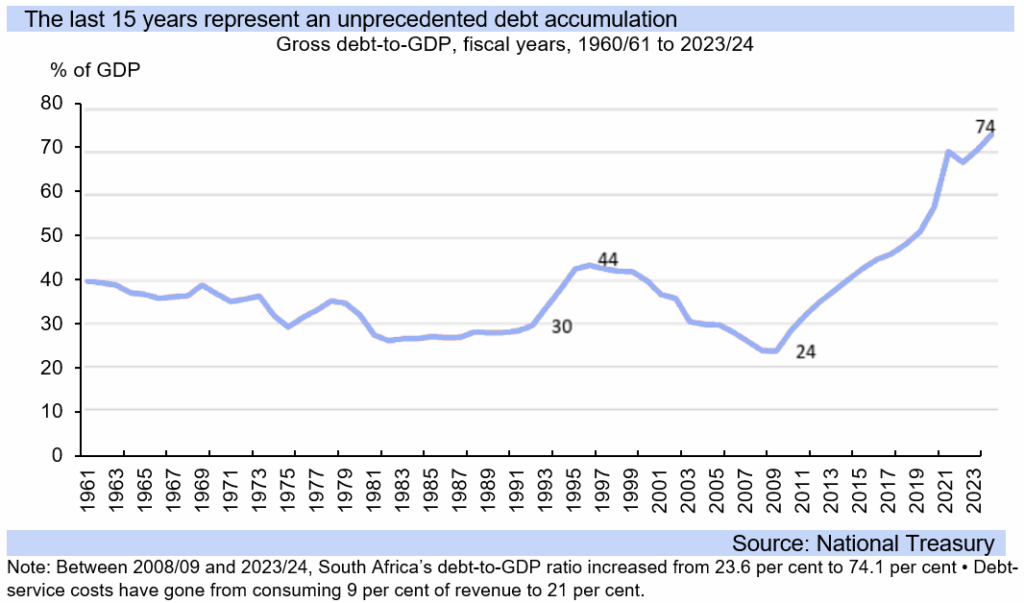

However, this has not resulted in slowing growth in the government debt stock, which is up 8.5% year-on-year through the first quarter of the government’s financial year.

The government’s debt burden currently sits at R5.8 trillion or 78.1% of GDP. Godongwana projected only a 7% rise for the full financial year to 77.4% of GDP.

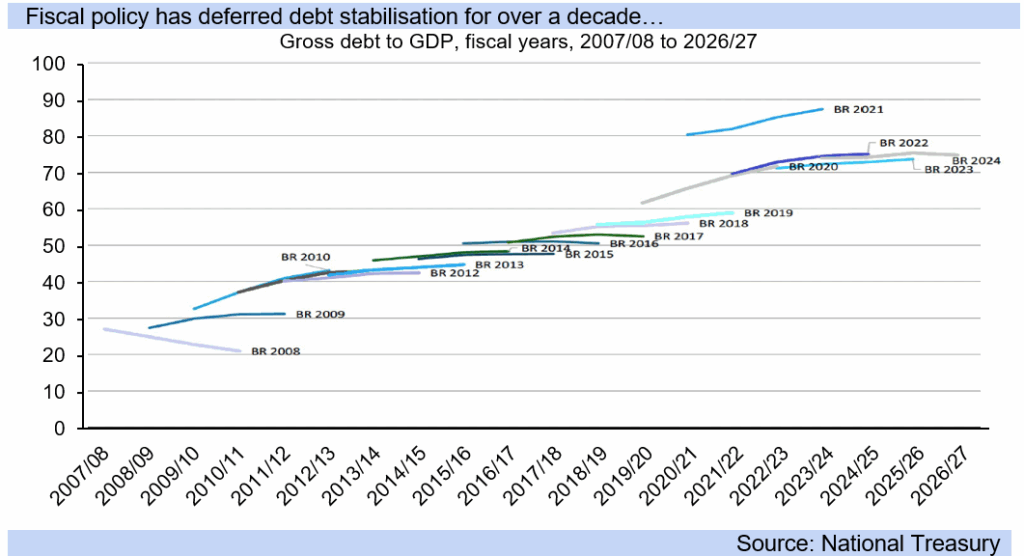

South Africa’s National Treasury has a history of being overly optimistic regarding its budget projections for economic growth and its debt burden.

It has consistently forecast a stabilisation in the government’s debt burden in the near future. However, this has not played out following the several forecasts made since 2009.

Since the last full budget surplus in the 2008/09 financial year, nearly every budget has projected that the government’s debt would stabilise in the near future.

However, the stabilisation target has been repeatedly postponed and revised upwards, as the necessary adjustments were not made.

In particular, the government rapidly increased its spending, without a corresponding rise in economic growth as much of the funds went towards consumption and not productive areas, such as infrastructure investment.

The growth in South Africa’s debt burden and the repeated projections of stabilisation can be seen in the graphs below.

Comments