Major South African banks face R338 billion threat

South Africa’s fintech market is projected to reach R337.65 billion in the next five years, posing a significant challenge to the country’s major banks.

While South Africa’s banking industry has always been dominated by big, established banks, they are now facing increased competition from smaller, more agile companies.

These younger players have more flexibility and can be more accessible to new-to-credit (NTC) consumers, but this means they also face increased risk.

These findings were revealed by TransUnion’s latest South Africa Research Report, Decoding FinTech Consumer Profiles.

Based on an analysis of 4.3 million consumers with at least one open fintech obligation, this report found that fintechs are set to play a far larger role in South Africa’s credit market in the coming years.

According to TransUnion, South Africa’s fintech market is projected to reach $19.5 billion (R337.65 billion) by 2030. The report said this signals a major shift in how local consumers engage with credit.

It found that, while fintech borrowers tend to be younger and riskier, they are not necessarily underserved.

Interestingly, fintechs are not the preferred entry point for NTC consumers, as they account for 17% of NTC originations, while the majority (69%) enter the credit ecosystem via retailers.

In addition, among 0 to 1-month term borrowers, 44% of fintech consumers hold two to three products while 27% hold four or more.

“This challenges the assumption FinTech borrowers have limited access to credit,” the report explained.

Concerningly, the analysis further found that fintech borrowers underperform on repayment, with these customers having the highest delinquency rates.

Delinquency rates stand at 74% for 0- to 1-month loans and 45% for 2- to 12-month loans, compared to lower rates among bank and nonbank lenders.

TransUnion said this underscores the need for stronger risk management among fintechs, as their borrowers tend to be more risky compared to traditional lenders.

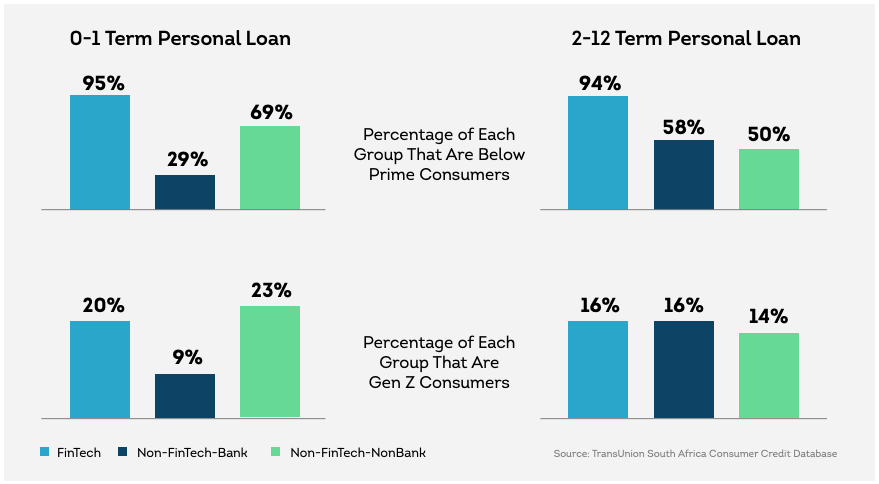

This heightened risk exposure can also be seen through the fact that fintech borrowers are significantly more concentrated in subprime risk tiers –

- For 0- to 1-month term loans, 95% of fintech borrowers are below prime compared to 29% for banks and 69% for non-bank lenders.

- For 2- to 12-month loans, 94% of fintech borrowers are below prime versus 58% for banks and 50% for non-banks.

However, TransUnion pointed out that there are signs of score improvement among fintechs, suggesting the potential for recovery.

For traditional lenders to remain competitive, TransUnion suggested they develop targeted consumer strategies that attract, retain and grow relationships with digitally engaged borrowers.

The difference in risk between fintechs and traditional lenders can be seen in the graphs below, courtesy of TransUnion.

Risky business

The Reserve Bank’s economics research department released a working paper earlier this year titled ‘Fintech and financial system stability in South Africa’.

This study covered the period from 1998 to 2020, which coincides with an era when South Africa experienced significant growth in fintech firms.

It found that the boom of fintech firms in South Africa presents significant risks to the country’s incumbent financial institutions, particularly big banks.

While local fintechs have created new opportunities to make financial systems more efficient, they have also created challenges that could affect the country’s financial stability.

“Their ability to innovatively use technology to find alternative solutions to banking clients’ needs is putting pressure on incumbent retail banks,” the paper explained.

“The traditional banks realise that the disruption by these non-traditional competitors is threatening their survival.”

The research paper explained that the threat to incumbents’ operating models and the increased competition not only negatively affect profitability, but also, consequently, result in threats to systemic stability.

It said that, as banks lose market share to fintechs, they may be forced to take bigger risks to adapt, and adaptation is far costlier for big institutions than small start-ups.

“Similarly, there is evidence that fintech firms are partnering with banks and other financial institutions, which creates systemic risks because of potential disruptions to these third-party services,” the researchers said.

This is largely due to the vulnerabilities this interconnectedness could create to cyberattacks or operational failures.

Comments