South Africa goes from zero to hero in a year

South Africa has had a year of two halves in 2025, with the first half characterised by extreme volatility and heightened pessimism. In contrast, the second half has been full of positivity, with some analysts saying the country’s lost decade has come to an end.

This is a remarkable shift in sentiment and perception, which appeared to occur overnight. However, economists have been quick to point out that it has been years in the making.

The turnaround in South Africa’s financial health dates back to 2021, when Enoch Godongwana was appointed finance minister and implemented fiscal consolidation in earnest.

At this time, discussions also kicked off between the National Treasury and the Reserve Bank about lowering the inflation target to 3%. This shift was officially announced during Godongwana’s most recent Medium-Term Budget Policy Statement (MTBPS).

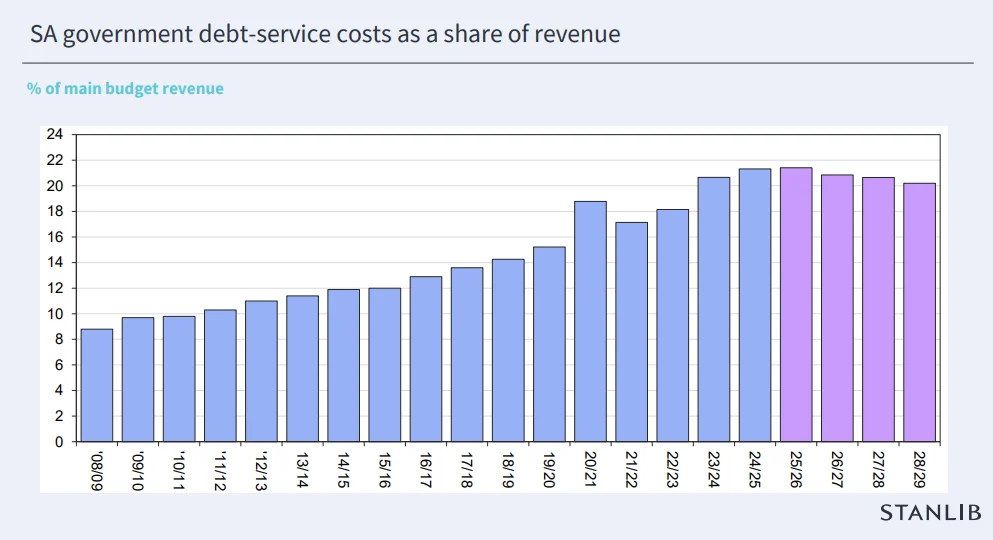

The MTBPS has become the symbolic marker of South Africa’s turnaround, with it revealing that government debt as a share of GDP will peak at 77.9% in the current financial year, the state will post a wider primary surplus, and significant infrastructure investment.

It was followed by South Africa’s first credit ratings upgrade in a decade from S&P Global and occurred in a year where the JSE All Share Index had returned close to 50% in dollar terms.

Head of South African macroeconomic research at Standard Bank, Dr Elna Moolman, outlined South Africa’s years of two halves and why positivity is picking up after the country’s lost decade.

“The first half was characterised by extreme levels of uncertainty, underpinned by a combination of local and global developments,” Moolman said.

“Globally, there was uncertainty from the abrupt adjustments to US import tariffs. Domestically, we had three iterations of the Budget before we could finally pass the 2025 Budget, creating uncertainty about fiscal policy and the durability of the government.”

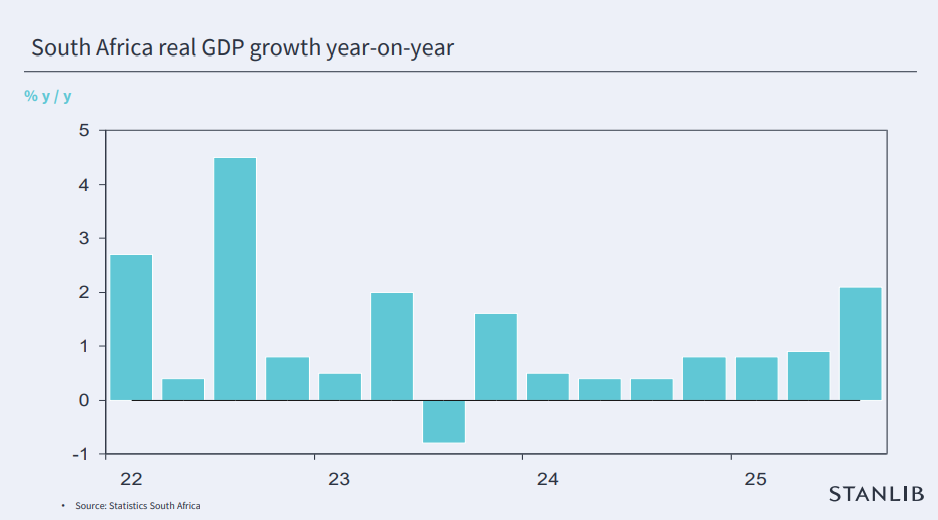

This elevated level of uncertainty resulted in the consensus forecast for South Africa’s economic growth being slashed from 2% to 1% by the middle of the year.

The period also saw South Africa experience substantial swings in the value of the rand, local assets plunge in value, and fears of the government’s financial health continuing to deteriorate.

Godongwana’s Budget revealed debt-servicing costs had crossed R1 billion per day and consumed 22% of tax revenue.

The tide turns

In the second half of the year, the script was effectively flipped, with negativity replaced by positivity and volatility by stability.

Importantly for South Africa, this was despite ongoing tension between the country and the United States and times of elevated geopolitical uncertainty.

This points to increased positivity around the country’s economic fundamentals and the realisation that the impact of US trade shifts is unlikely to be as severe as some had forecasted.

“Things have turned around in the second half of the year. We started seeing some upward revisions to economic growth forecasts,” Moolman said.

“South Africa was removed from the greylist, and we had our credit ratings upgraded by S&P. We saw further evidence of the government’s commitment to fiscal consolidation with a peak in the debt-to-GDP ratio this year.”

Perhaps most crucially, there was increasing evidence that the government’s ongoing reform of the electricity and logistics sector through Operation Vulindlela was gaining momentum.

The task team has expanded its focus to include the water sector, as well as finding ways to tackle the collapse of local government.

“We also had a change in the Reserve Bank’s inflation target from a 3% to 6% band to a 3% point target, with a one percentage point tolerance either way,” Moolman noted.

“This was coupled with ongoing interest rate cuts, which should support growth not only in 2025, but throughout 2026. This is one of the tailwinds behind consumer spending growth.”

Moolman said consumer spending and economic growth have generally exceeded expectations in 2025, with household finances holding up better than expected.

“This should continue into 2026, when we should see further monetary policy relief that will be supportive of consumers.”

Moolman explained that the picture is not all good, with private sector fixed investment remaining weak, preventing faster economic growth.

Fixed investment is key for sustained faster economic growth, with investment in machinery, equipment, and infrastructure leading to productivity growth, which can be self-reinforcing.

This is desperately needed to result in faster economic growth over the next few years, Moolman said.

Comments