End of an era of pain for South Africa

South Africa’s ‘lost decade’ from 2015 onwards appears to be coming to an end, as the government’s finances show signs of improving, the rand is strengthening, and economic growth is slowly picking up.

This is expected to result in better returns in the coming years for investors on the JSE, particularly from so-called SA Inc. stocks that derive most of their earnings from South Africa.

The rally seen on the JSE this year, as well as the minor bounce after the formation of the Government of National Unity (GNU), indicates that local assets are rerating.

This is feedback from Symmetry’s chief investment strategist, Izak Odendaal, who explained why South Africa’s lost decade may be over in a recent research note.

Odendaal explained that South Africa’s lost decade began sometime in the mid-2010s, depending on which event you look at.

Some argue it began after the pride and excitement of the 2010 FIFA World Cup faded, while others point to the country’s credit rating dropping into sub-investment grade territory, also known as junk status.

Odendaal argued the Nenegate scandal provides a good marker to date the lost decade, as it was the moment when both local and international investors realised that something was fundamentally wrong.

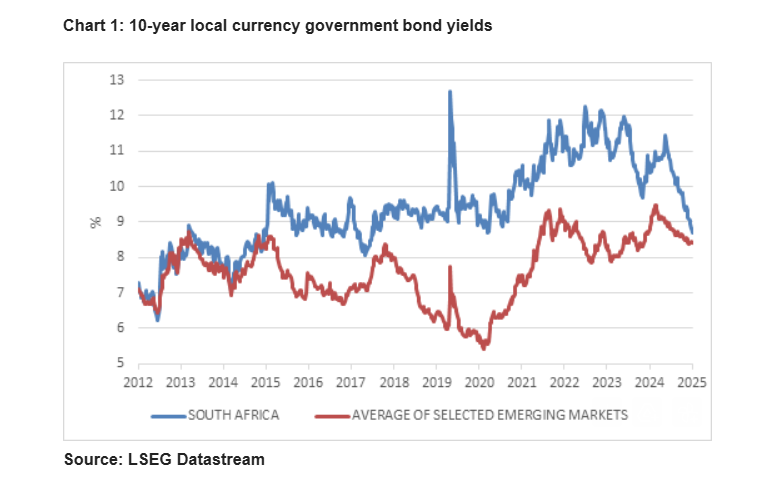

South Africa was not only downgraded by ratings agencies after Nenegate, but was also instantly downgraded by the market. It began trading at a discount to its peer countries, with its borrowing costs soaring.

The consequence of earlier mismanagement, notably loadshedding, a logistics crisis and elevated government debt levels, proved to be persistent.

Things are now beginning to look up for South Africa, a decade later, as substantial reforms in key sectors of the economy and fiscal consolidation begin to bear fruit.

The country has not experienced severe loadshedding since early 2024, and painful fiscal consolidation has eased anxieties over government debt levels.

A few weeks ago, S&P Global upgraded South Africa’s credit rating. Moody’s did not follow suit at its scheduled review on Friday but will likely come around eventually.

Though there is much work to be done in improving governance and fighting corruption, the removal from the FATF grey list is another marker of improvement.

The gap between South African and peer country borrowing costs has now basically disappeared – a decade after it first opened.

South African assets coming alive

South Africa’s stock market has had one of its best years on record in 2025, with the JSE All Share Index returning close to 50% in dollar terms.

This has been boosted by a strengthening rand, but is nonetheless a positive outcome for local capital markets and the broader economy.

Odendaal explained that this has largely been driven by the returns of precious metals miners, which do not directly improve economic activity.

However, the rise in commodity prices will bolster state finances through increased corporate income tax receipts and a stronger rand.

Indirectly, this should translate into faster economic growth, and if coupled with sound fiscal policy and continued reforms, may create a positive feedback loop.

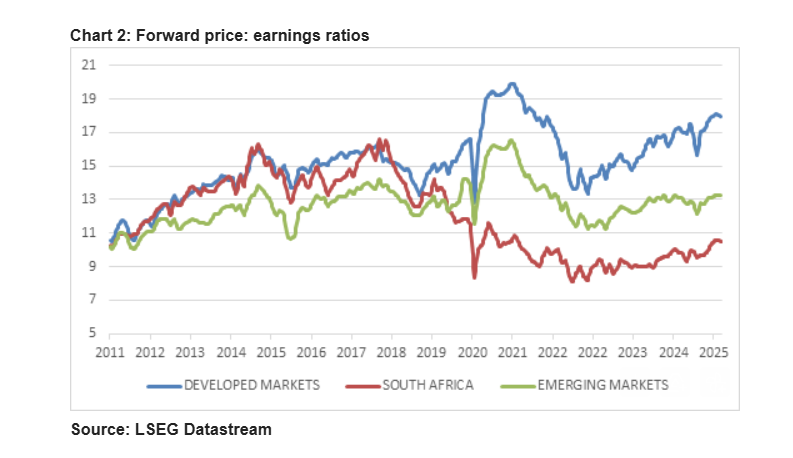

Odendaal explained that South African equities traded on a similar price-earnings multiple to developed and emerging markets prior to 2018 but suffered a severe derating thereafter. This was a substantial drag on returns.

The derating was driven by sector-specific issues, but also broadly because global investors demanded a greater margin of safety for deploying capital here while locals were still desperate to get their money out.

Reserve Bank data shows a cumulative R480 billion net acquisitions of foreign assets by domestic firms between 2013 and 2019.

This trend of offshore acquisitions at the cost of domestic investment, which seems to have turned, was both a consequence of and a contributor to a period of economic stagnation.

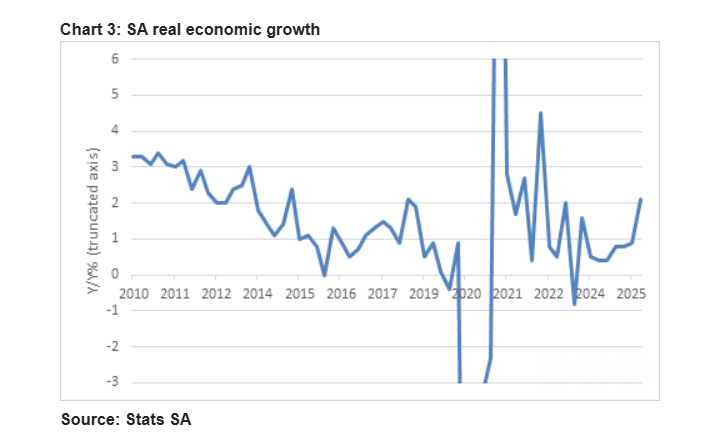

South Africa’s real economic growth rate averaged 2.8% between 2010 and 2013, but downshifted dramatically from 2014 onwards to average only 0.7% over the subsequent decade.

This is lower than the population growth of around 1.3% per year, meaning the country has been getting poorer on a per-person basis.

2025 is already looking better, despite headwinds from US tariffs. The third quarter real gross domestic product (GDP) was 0.5% higher than the second quarter.

Household spending has recovered strongly from a period of high inflation and high interest rates, hitting 3% year-on-year. Looking ahead, real growth in household spending is likely to ease slightly from its current high base to around 2%.

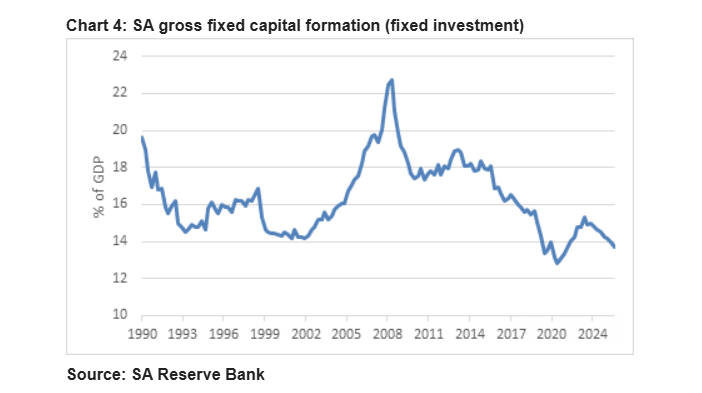

For overall economic growth to continue rising, however, fixed investment spending must rise, Odendaal explained.

This has been depressed for several years as a lack of funding has limited public sector capex, while low business confidence, policy uncertainty, infrastructure bottlenecks and the focus on international expansion have weighed on private spending.

Fixed investment averaged around 18% of GDP between 2010 and 2015, but in the wake of Nenegate, it collapsed sharply to 14%, well below the 25% to 30% level needed to sustain rapid economic growth.

To turn this around, the National Budget is gradually shifting the mix of spending from salaries to capital spending, while efforts are underway to unlock private investment in infrastructure.

This is not straightforward, but it is a priority for the government. Experience in other countries shows that once the blueprint has been established for crowding private capital and expertise into infrastructure projects, it can be rolled out at speed and scale.

Private companies should also increase investment in their own businesses when they become more confident about growth prospects. Lower borrowing costs will also help.

This should translate into much faster economic growth in South Africa, with corporates sitting on over R1.8 trillion in cash which can be deployed relatively quickly into the economy.

Comments