Dark clouds gather over one of South Africa’s most important employers

South Africa’s manufacturing sector is coming under increasing pressure from elevated tariffs on exports, rising electricity prices, and logistical bottlenecks.

This is coupled with a stagnant economy and a lack of business confidence, resulting in minimal investment in the sector and limited local demand for its products.

The collapse of South Africa’s manufacturing sector puts millions of jobs at risk and makes the country increasingly reliant on imports for basic goods.

Crucially, the manufacturing sector can absorb unskilled or semi-skilled workers, which make up the majority of the country’s unemployed, relatively quickly.

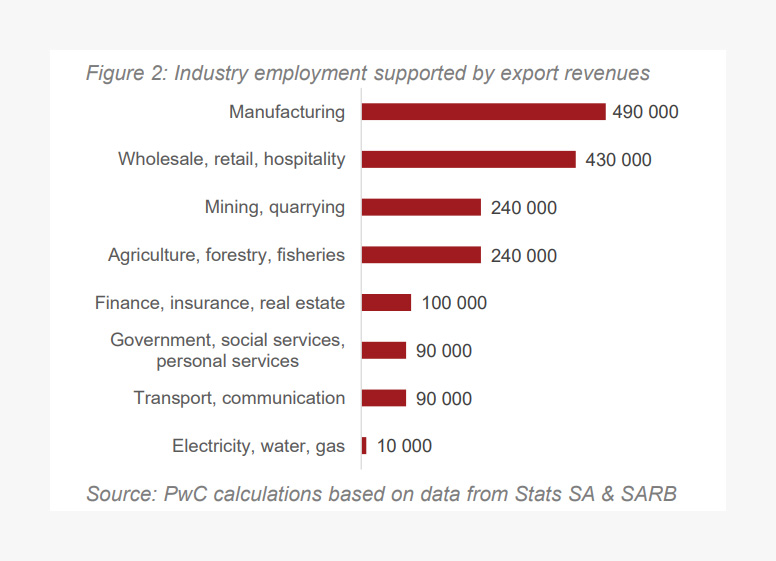

Manufacturing employment is the most exposed to geopolitical tension and tariffs from the United States, with around 490,000 jobs in the sector sustained by export revenues.

This is around a quarter of the 1.7 million jobs sustained by exports in South Africa and double the share of mining, which is traditionally seen as the most important export sector.

PwC explained that South Africa is a small, highly open economy, which makes it vulnerable to external shocks like changing political relationships and technological innovation.

An added layer of vulnerability is the country’s dependence on trade and foreign investment for economic growth, both of which have come under immense pressure in recent years.

As a result, global uncertainty and volatility from trade tariffs have a direct impact on the local economy and thousands of jobs.

For South Africa, PwC said decisions made in Washington, Beijing, London, and Brussels are almost as important as those taken in Pretoria.

Decisions made in developed economies have a direct impact on the local economy and particularly export prospects.

Increased US tariffs, for example, make South African products less competitive by increasing the cost of goods in the American market.

For example, South Africa’s automotive exports to the US declined by R2.7 billion in the second quarter of 2025 to R4.9 billion. This is a 35% decline year-on-year.

Other countries and economic blocs are considering trade barriers of their own. The European Union’s (EU) Carbon Border Adjustment Mechanism is an example of this.

This mechanism is set to impose a carbon price on high-emission imports into the EU to encourage businesses to limit emissions.

Such a change could have dire consequences for South African exports to the EU, with the country still heavily reliant on coal-fired power plants for energy and road transport.

The graph below, courtesy of PwC, shows how many jobs are dependent on exports in various sectors of South Africa’s economy.

Local investment in the doldrums

The international headwinds impacting South Africa’s manufacturing sector are compounded by a lack of local investment in the industry.

South African businesses are hesitant to invest in a stagnant economy and amid elevated uncertainty, especially in a sector with a declining output.

The local manufacturing sector is one of the biggest casualties of this unwillingness to invest, with current levels of capital expenditure insufficient to even maintain existing equipment and machinery.

This means the capital stock of the sector is going backwards after years of declining output amid load-shedding and logistical inefficiencies.

Stanlib chief economist Kevin Lings recently outlined the lacklustre investment in the sector and why companies are so hesitant to invest.

South Africa’s historical sources of employment, manufacturing and mining, have seen investment plummet in recent years.

“There is substantial underinvestment in the ‘productive sector’, as economists call it. In manufacturing, investment levels are terrible,” Lings said.

“The capital stock is going backwards. In other words, in the manufacturing sector, corporates are not investing enough to maintain the machinery and equipment they already have in place.”

This points to an industry in significant decline, with companies barely investing enough to keep their doors open.

Data from the Reserve Bank indicates that only 77% of the country’s manufacturing capacity is used, reflecting weak demand in the local economy.

Lings explained that companies are hesitant to invest due to a lack of confidence in the local economy.

The main drivers behind their caution are the country’s poor economic growth, ongoing political uncertainty, and elevated interest rates, which boost the returns of money market funds and call accounts.

Some areas where companies are investing include renewable energy, backup water supply, warehousing, and services.

South Africa’s automotive industry is particularly vulnerable due to the development of local and international factors in recent years.

BDO South Africa Automotive Sector Leader Siyabonga Mthembu said South Africa’s automotive sector is at a crossroads, with the decisions made today likely to determine the industry’s chances of survival in the coming years.

Infrastructure challenges, particularly related to ports, which are still ranked as among the worst performing, and rail efficiency, as well as policy and regulatory uncertainty are the most significant headwinds the industry currently faces.

“Of concern is that, as a country, we’ve not yet effectively addressed the basics that are critical to ensuring a conducive investment climate for the automotive manufacturing sector,” Mthembu said.

“As if this wasn’t enough, the sector now faces an onslaught from imports of Chinese and Indian vehicle models.”

As a result, the country’s Completely Knocked Down unit mix has deteriorated by more than 11% since 2018, from 60% to 54% in 2023, due to more vehicles being imported rather than produced locally.

Localisation levels have reduced by 10% since 2021, from 42% to 38% in 2023, with Tier 2 and lower suppliers significantly underdeveloped.

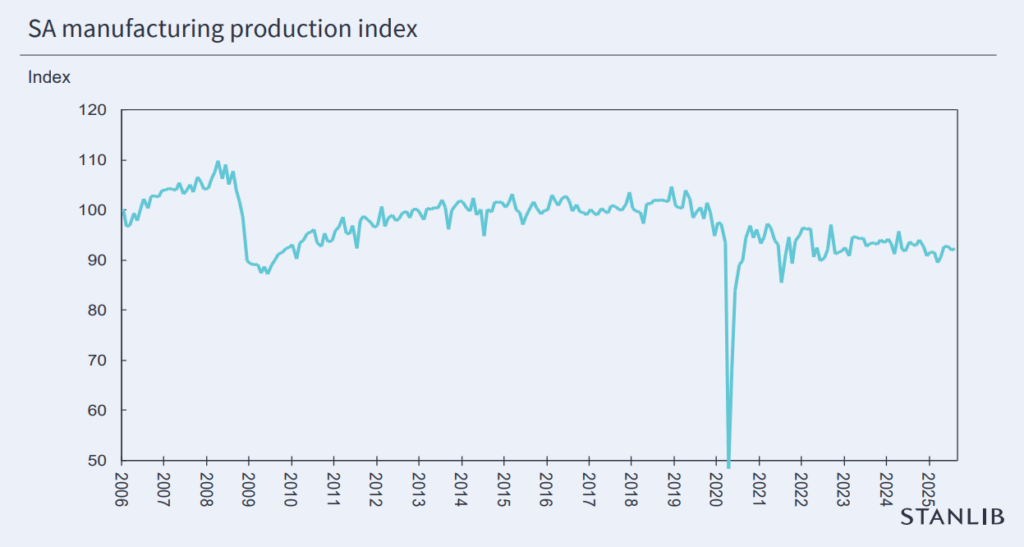

The graph below, courtesy of Stanlib’s Kevin Lings shows the steady decline in the output of South Africa’s manufacturing index.

Comments