Pick n Pay on the right track

Pick n Pay’s recent rights offer has proven to be a significant boon for the retailer, allowing it to reduce the company’s heavy debt burden and reinvest in its business.

This was revealed in Pick n Pay’s results for the interim period ending August 2024. This also marks the first period after Pick n Pay concluded its R4 billion rights offer.

On 5 August this year, Pick n Pay announced that it had completed its Rights Offer. The retailer raised R4 billion in capital with a high subscription rate and overwhelming market support.

Pick n Pay said the Rights Offer was 106% oversubscribed, with total subscriptions reaching over R8 billion. It said 98.7% of shareholders followed their rights, and the retailer received R4.3 billion in excess applications.

The rights offer was implemented to decrease Pick n Pay’s debt, which became a drag to the group. R3 billion of the rights offer capital was used to repay debt, with the remainder used for capital investment.

Pick n Pay allocated R600 million to capital expenditure, half of which was allocated to Boxer store openings.

The rest was spent on Pick n Pay Clothing, refurbishing essential Pick n Pay stores and online platforms.

The group’s net capital expenditure was less than half of what it allocated in the previous period to improve its liquidity.

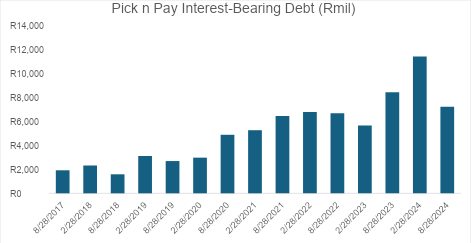

Over the past few years, Pick n Pay has become a victim of a massive debt problem. In seven years, the retailer’s debt increased from R1.9 billion to R11.5 billion, which put significant pressure on its finances.

Over this period, Pick n Pay’s capital structure also changed – initially, 10% of its assets were financed by debt; in February this year, this figure stood at around 25%.

The rights offer, therefore, brought significant relief to the group, aiding in the overall reduction of its interest-bearing debt from R11.4 billion to R7.2 billion. This can be seen in the graph below

However, even though Pick n Pay’s debt was significantly reduced, it still had to cover the interest expense for most of the interim period.

This caused Pick n Pay to reach a record-high interest expense, which amounted to R1.42 billion over the past six months and R2.8 billion over the past twelve months. This can be seen in the graph below.

The retailer’s debt burden is the main reason for Pick n Pay having reported a R1 billion loss before tax in the interim period. This marked a significant increase from the R880 million loss the previous year.

The rights offer also allowed Pick n Pay to move out of technical insolvency, increasing its equity from -R183 million to R2.89 billion.

It also improved its debt ratio from 100% of Pick n Pays assets being financed by liabilities to 94% being financed with liabilities.

Before the rights offer, Pick n Pay could only cover 78% of its short-term liabilities with short-term assets (liquid). It can now cover 89% of its short-term liabilities.

It could also only cover 21% of its current liabilities with cash, but it can now cover 22% with cash.

Although still far from its industry peers like Shoprite, the money that investors provided to Pick n Pay during the rights offer significantly improved the company’s debt position.

The concluded rights offer marks Pick n Pay’s first stage of its recapitalisation plan. Its second stage is set to offer even more relief for the struggling retailer.

The second stage involves Boxer’s unbundling and listing on the JSE, which is expected to bring in around R8 billion to Pick n Pay.

The proceeds from Boxer’s listing will be used to settle the group’s outstanding debt, which currently amounts to R7.2 billion.

Eliminating Pick n Pay’s debt will have a positive impact on the group’s profitability for the following reporting period.

In addition, the company will have money left over after clearing its debt, which will allow the retailer to reinvest in its business and focus on growth rather than survival.

Without a R1.4 billion interest expense, Pick n Pay also has a much lower hurdle to overcome in order to report a profit.

Pick n Pay CEO Sean Summers told investors at the company’s interim results that “the worst is now behind us”, and the retailer can now focus on growth and becoming more competitive.

Therefore, with the rights offer concluded and the listing set to happen soon, the retailer is in a far better financial position that at the start of this year, which can be seen in the table below.

| Metric | February 2024 | August 2024 |

| Equity (R mil) | -R183 | R2,880 |

| Current Ratio | 0.79 | 0.89 |

| Debt Ratio | 1.00 | 0.94 |

| Cash Ratio | 0.21 | 0.22 |

Comments