Dis-Chem showed strong growth – but it came at a cost

Dis-Chem has shown strong growth over the last few years, but because it involved a series of acquisitions, it came at the cost of a significant increase in debt.

Husband and wife team Ivan and Lynette Saltzman founded Dis-Chem in 1978. They established a small pharmacy with a capital investment of only R10,000.

The business expanded rapidly in Johannesburg and Pretoria in the nineties, using the tried-and-tested formula of discounted medicine and non-pharmaceutical offerings.

The Dis-Chem stores were also always bigger than their competitors, further adding to their appeal.

The business continued to diversify and expand, adding its private-label offerings in 1997 and opening its first franchise in Namibia in 2014.

By 2016, the company had opened its hundredth store and was generating annual revenue of R15.5 billion.

The management team decided to list Dis-Chem on the JSE, which garnered a lot of excitement from investors.

The business continued to show strong growth after listing. Over the last financial year, Dis-Chem generated R36.3 billion in revenue, up from R32.7 billion the previous year.

The retailer increased net profit after tax from R966 million to R1.02 billion and increased equity from R3.9 billion to R4.5 billion.

Dis-Chem is undoubtedly one of South Africa’s biggest success stories. It is a household name and is trusted by millions of people.

Dis-Chem expansion

Since Dis-Chem was listed on the JSE in November 2016, the retailer embarked on an aggressive expansion strategy.

Dis-Chem started to target the market share of its main competitor, Clicks, as part of this expansion.

In 2016, Dis-Chem held 40.3% of the combined Clicks and Dis-Chem market share, with Clicks holding the remaining 59.7%.

Over the course of ten years, Dis-Chem closed the market share gap, holding 46.6% of the combined market, with Clicks holding 53.4%.

Dis-Chem achieved its growth through a series of acquisitions, including TLC Pharmacy, CJ Distribution, Quenets, and Baby City.

As part of its growth strategy, the company also acquired Kaelo, Healthforce, Medicare, and Columbia Falls Properties.

Through these acquisitions, Dis-Chem significantly expanded its operations. It also invested significant resources into distribution centres.

Dis-Chem had to finance many of its acquisitions and expansions through debt, which means it started carrying far more debt on its balance sheet.

Since it was listed on the JSE, Dis-Chem’s debt rose substantially, from around R1 billion in 2017 to R2.6 billion in 2024.

Dis-Chem’s rapid expansion did not achieve significant economies of scale, which is one of the benefits of such a strategy.

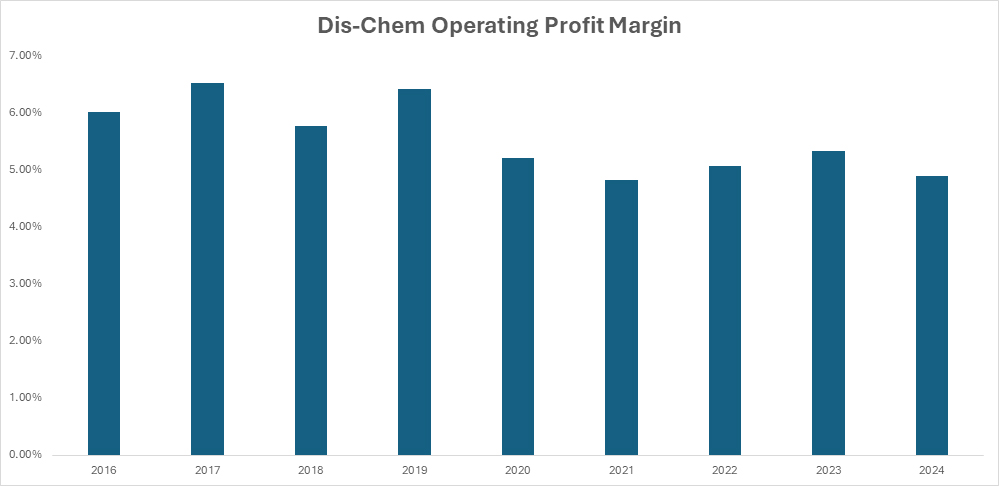

Since 2016, Dis-Chem’s profitability has been under pressure. The group’s operating profit margin fell from over 6% to 4.9% in its most recent report.

This indicated that Dis-Chem has not yet been able to decrease its operating expenditure relative to its revenue growth.

With aggressive acquisitions, larger companies often achieve operational synergies and efficiency improvements, increasing profitability.

However, this has not yet been the case with Dis-Chem, as shown in the chart below.

Although Dis-Chem’s debt levels have increased significantly, it managed to keep its financing expenses relatively constant in relation to its revenue.

This means the relative increase in finance costs to revenue has remained constant, and finance expenses have been maintained at around 1% to 1.6% of revenue.

The only drawback is that its main competitor, Clicks, has virtually no interest-bearing debt in its books.

Clicks has also acquired other businesses, expanding its footprint, though less aggressively than Dis-Chem.

The big difference is that Clicks opts to expand organically and only uses internal capital for its expansion.

This gives Clicks a 100 to 160 basis points edge on net profitability over Dis-Chem.

Clicks CEO Bertina Engelbrecht said they make sure they can extract value from businesses before they acquire them.

She stated that Clicks ensures that they can generate high returns from the target by making sure that the business is well run by its management.

Additionally, she stated that the company always ensures synergies can be gained from an acquisition and that Clicks’ management can manage the business better than its current management.

This strategy has worked well for Clicks, with its operating profit margin increasing from 7.5% in 2017 to 8.7% in its most recent reports.

Comments