The American retail giant already taking on Pick n Pay, Woolworths, and SPAR

American giant Circle K is slowly but surely gaining a foothold in South Africa’s convenience retail space, with it operating five stores in Gauteng.

The retailer is set to expand into the Western Cape with stores in Goodwood and Mowbray in the near future as it builds out its offering in South Africa.

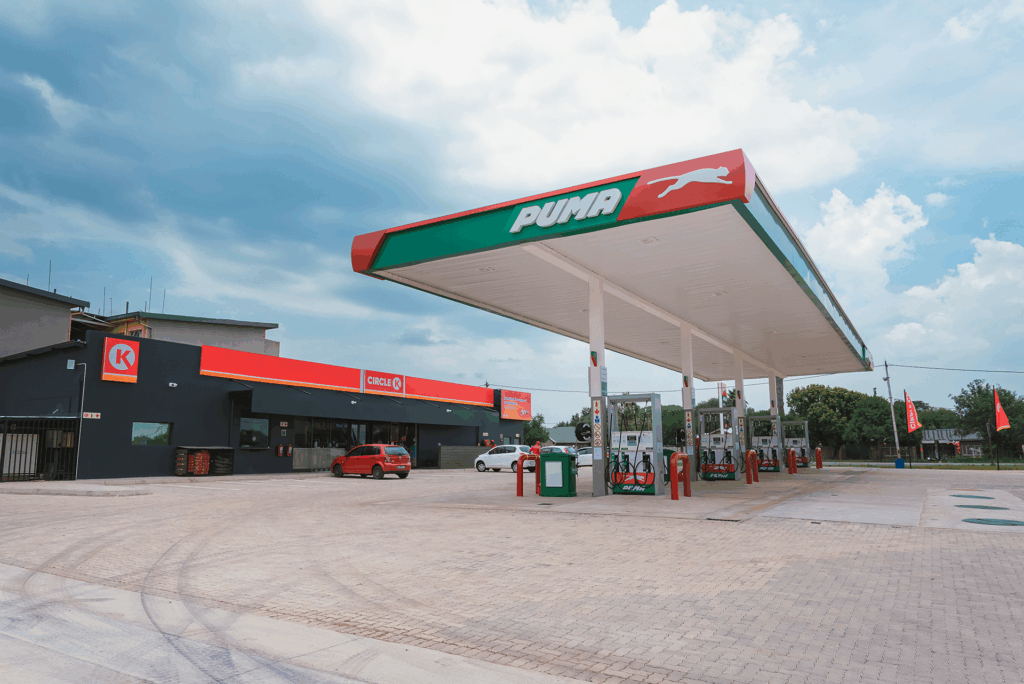

It currently has a deal with Puma Energy to operate stores in the brand’s petrol station forecourts around South Africa. Ultimately, this should give Circle K access to over 100 retail sites in the country.

This may receive a significant boost in the near future, with Puma Energy owner Trafigura being in talks to acquire Shell’s downstream assets in South Africa.

If this deal goes through, Puma Energy will have one of the largest petrol station networks in South Africa, giving Circle K significant room to expand.

The brand also has ambitions to expand beyond petrol station forecourts, with it operating a standalone store at the University of Johannesburg.

Operated by Millat Convenience, Circle K is run under a Master Level Agreement with the Alimentation Couche-Tard subsidiary. Millat has the right to open and operate Circle K franchises throughout South Africa as the exclusive franchisee.

Circle K is a formidable company, with the brand having over 14,000 stores across its global network in over 25 countries.

Founded in Texas in 1951, the company has undergone a rapid expansion under Couche-Tard into South America, Africa, the Middle East, and Asia.

South Africa’s convenience retail market is dominated by traditional food retailers such as Pick n Pay, Woolworths, and Food Lover’s Market’s Freshtop.

These retailers focus on offering a curated range of products that one would find in a typical food supermarket, with the aim being to leverage their brand to attract customers.

Circle K offers something different in its focus on hot, fresh food in a convenience retail format, with products such as breakfast burritos, burgers, vetkoek, pizza slices, and baked goods.

These are offered alongside more traditional convenience store products, which centre around hot and cold beverages, confectionary sweets, and snacks.

Circle K currently has five stores in Gauteng, with plans to open two in Cape Town in the near future. The company says footfall at its stores has exceeded expectations.

“Unlike other forecourt operations, where petrol often takes precedence over stores, we have inverted the model with the intention of our outlets becoming sought-after destinations in themselves,” Millat Group CEO Hamza Farooqui said at the company’s launch in 2022.

“Apart from a welcoming ambience and décor, we will offer a variety of freshly made (on-site), chef-inspired food as well as several new imported candy and confectionery brands.”

Intense competition

Circle K faces intense competition in South Africa, with traditional retailers and specialised operators investing heavily to capture the country’s growing convenience retail market.

Petrol station forecourts are particularly intense battlefields, with the retail sales from these stores being estimated at over R33 billion a year.

Crucially, in a stagnant economy, this sector is growing quickly, and retail sales are outpacing fuel sales at petrol stations across the country.

Petrol station forecourts have evolved in recent years to adapt to this need, becoming sites of increased retail activity and diverse offerings.

Some players, such as bp, have plans to even include licence disc renewals and battery rentals at their forecourts to reduce their reliance on fuel sales.

In effect, petrol station forecourts have become one-stop shops for convenience retail in various forms, including courier services and eCommerce players.

Traditional retailers such as Shoprite, Pick n Pay, Woolworths, and SPAR have expanded into this sector in recent years.

Trade Intelligence estimates that around 849 petrol station forecourts in South Africa host branded retail stores, a 26% increase over five years.

Research shows that forecourt shoppers prefer supermarket-branded stores over fuel-branded ones for their familiarity and quality.

However, at over 330 stores, FreshStop dominates the market, with the forgotten player successfully cornering over a third of the market.

This is due to its partnership with Caltex/Astron Energy, which gives the retailer a presence in hundreds of its petrol stations.

Circle K is trying to replicate this success with its partnership with Puma Energy. However, the fuel brand has a far smaller network than Astron’s 800-plus forecourts.

The American brand also lacks a well-developed supply chain in South Africa, with FreshStop leveraging that of its parent company, Food Lover’s Market, to be able to offer fresh food across the country.

FreshStop has also proven to be able to adapt to the needs of diverse communities across South Africa.

While its mainstay is offering fresh, healthy food in a convenience format, FreshStop has not abandoned the established ‘five Cs’ of petrol station retail – chocolate, coffee, carbonated soft drinks, chips, and cigarettes.

Competition is also stiff from traditional retailers wanting a slice of the fast-growing convenience retail pie.

Pick n Pay has hitched its wagon to bp petrol stations in South Africa and has rapidly grown its footprint across the country.

Woolworths’ Foodstop brand is present in many Engen garages. However, unlike other Woolworths stores, these are all franchisee-owned.

SPAR has partnered its express brand with Shell, despite the Anglo-Dutch petroleum giant having its own convenience offering under the Shell Select brand.

Shoprite-owned OK Express is the market leader among traditional retailers, as it has partnerships with Puma and TotalEnergies.

OK Express stores are also becoming more prominent in Sasol petrol stations around the country as the historic retail brand reinvents itself.

Images of Circle K in South Africa

Comments