Major threat to Checkers, Pick n Pay, and SPAR in South Africa

South Africa’s major retailers are increasingly running out of space for their ambitious expansion plans, with the market at risk of becoming saturated.

This may result in retailers overextending themselves and potentially hitting a cliff where growth slows and potentially even stalls.

South Africa’s five largest retailers opened more than 700 stores in 2024, with more than 230 being set up in the first five months of 2025.

The warning of increased saturation pressures has been made by several retail CEOs and has now been repeated by Absa’s Corporate and Investment Banking division.

In its latest Absa Merchant Spent Analytics report for August, the bank explained that this pressure is not spread uniformly across all retail segments.

While some are showing noticeable resilience and growth, others are coming under immense strain, pushing players to adopt more defensive strategies.

Absa used retail space per capita, which is measured in square metres of gross leasable area (GLA) per person, as an indicator of market saturation and infrastructure scale.

It compared South Africa’s retail space per capita to international peers to determine whether the local market is saturated.

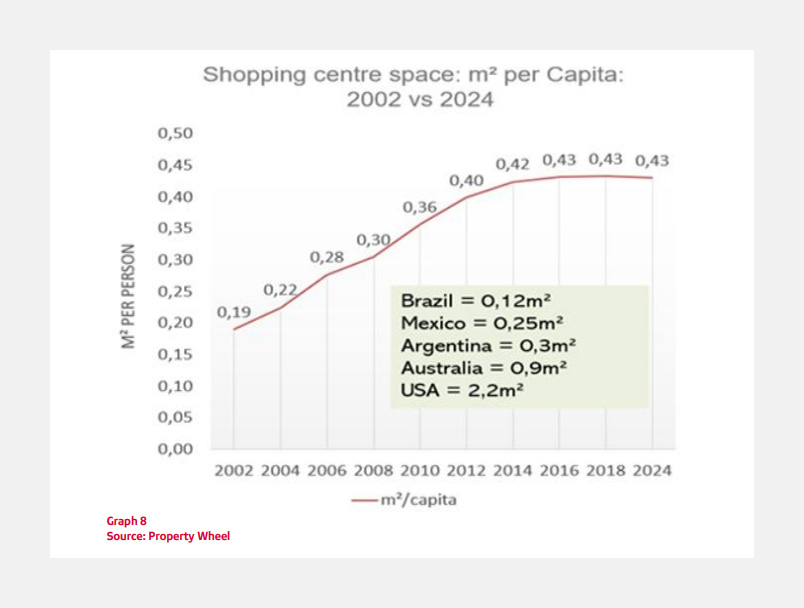

South Africa has around 23.4 million square metres of GLA across 1,960 shopping malls, placing it sixth globally for total retail centre supply.

However, on a per-person basis, this is lower than in developed markets. Absa said this reflected both rapid retail growth and limited population density support.

South Africa’s retail space per capita has been flat at around 0.43 m² since 2014. In contrast, highly developed retail markets such as the United States reach around 2.2 m².

This indicates potential room to grow further. However, the United States is a far larger economy with significantly greater consumer spending power.

Compared to its economic peers, South Africa is relatively highly developed in terms of retail space, with Brazil sitting at 0.16 m², Mexico at 0.28 m², and Argentina at 0.3 m². This points to the market not being saturated at a national level.

However, Absa said that digging deeper shows that certain market segments and areas are becoming saturated, threatening the rollout of some stores.

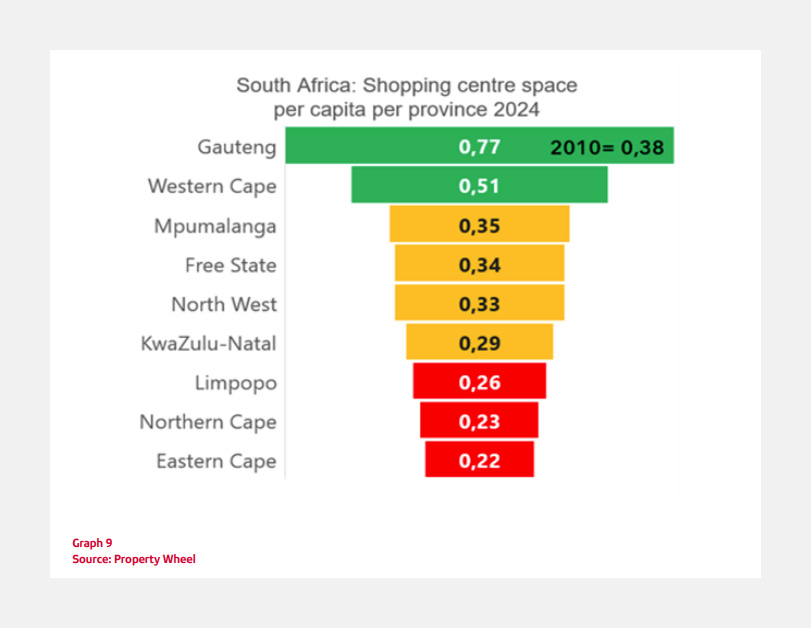

“Theoretically, South Africa is not overbuilt compared to global standards. However, the existence of large clusters in provinces like Gauteng, plus high vacancy rates in over-supplied regions, suggests localised oversaturation,” Absa’s report read.

“While national per capita floor space remains modest, dense pockets of retail in urban centres may generate a perception of oversupply while broader regions still have capacity.”

Absa said that pockets of growth remain, particularly in luxury retail and well-positioned super-regional malls. On the other hand, urban nodes appear saturated.

This points to future growth coming from tailored luxury stores and discount retailers, which is also evident in the expansion plans of South Africa’s largest retailers.

Shoprite has placed a big emphasis on its plan to double the footprint of its low-cost Usave brand in the next five years, while its main competitor, Boxer, has plans to open 500 more discount retail stores in the same period.

This indicates that the market served by traditional retailers, such as Pick n Pay, SPAR, and Woolworths, is saturated, with growth coming elsewhere.

Absa made it clear that this does not mean retailers will not continue to perform well, but that this continued performance will require improved economic conditions, better infrastructure, and more efficient space management.

CEOs raise the alarm

Several retail CEOs have raised the alarm about saturation in the South African market, warning that companies will not be able to continue rolling out stores at the same rate as they have historically.

Pick n Pay CEO Sean Summers said retailers are opening too many new stores, which will put their financial viability at risk.

Summers is well-placed to make this judgement, with Pick n Pay having gone through a painful process of closing poorly performing stores from a period of rapid expansion.

These stores operated at a loss despite the initial expansion thesis being sound, with many of the forecasted assumptions not playing out in reality around increased consumer spending and demand.

“South Africa is about to equal, or squeak past, the United States on the square metre per capita of retail,” Summers told Bloomberg.

“If you have got retailers who are prepared to just open stores at any cost, then a shopping centre works. But, I would question the medium-to-long-term wisdom of the strategy.”

This is particularly prevalent in South Africa’s low-growth environment, with GDP growth averaging an annual rate of 0.8% over the past decade.

While this is expected to improve, the increase is not meaningful in terms of reducing unemployment and boosting consumer spending.

Due to this low economic growth, South Africa’s per capita spending power is relatively low, making its sales densities meagre compared to countries with similar retail space per person.

SPAR CEO Angelo Swartz echoed Summers’ warning, expecting slower store growth over the next year as retailers refocus on increasing the efficiency of their existing real estate.

Swartz explained that the rapid rollout of retail space in South Africa’s low-growth environment has raised questions about sustainability and financial viability.

“Ultimately, retailers always need to make sure that they are opening quality stores,” Swartz told Bloomberg earlier this year.

“At the rate at which retail stores are opening in this country, it is hard to see that all of them will be sustainable.”

While there appears to be much more room to grow towards the lower end of South Africa’s retail market, questions are beginning to be raised in this regard, too.

Camissa Asset Management associate analyst Katlego Dinake recently explained that the aggressive rollout of discount retailers in the form of Boxer stores and Usave outlets will run into significant competition from spaza shops and informal traders.

Boxer has said it believes that it can win market share from these traders by offering proximity, scale, and affordability. This is far easier said than done.

Incumbents remain formidable, benefiting from deep community ties, an in-depth understanding of local demands and needs, as well as extreme proximity to consumers.

Comments