Luxury property boom in South Africa

Although South Africa’s post-2008 property market remains weak overall, the luxury and super-luxury segments have consistently outperformed, particularly in provinces such as Gauteng, KwaZulu-Natal, and the Western Cape.

This is according to Lightstone, which stated that South Africa’s property market has still not fully recovered from the 2008 financial crisis.

After a slow recovery that stalled around 2016, sales declined further during the Covid-19 pandemic, with only a brief post-pandemic rally showing early signs of fading.

“International markets such as the United Kingdom, United States and Australia have rebounded more strongly post-2008, while South Africa’s recovery has been more gradual,” said Lightstone managing executive Hayley Ivins-Downes.

“The data tells a story of resilience amid persistent headwinds from affordability pressures to economic uncertainty.”

Compared with selected global markets – the United Kingdom, United States, and Australia – South Africa’s recovery has been more sluggish, reflecting persistent economic, political, and affordability challenges.

Lightstone analysed transaction volumes, luxury market performance, provincial disparities, and how South Africa compares to international markets.

They excluded subsidised properties from our South Africa analysis, as their irregular introduction skews cyclical trends.

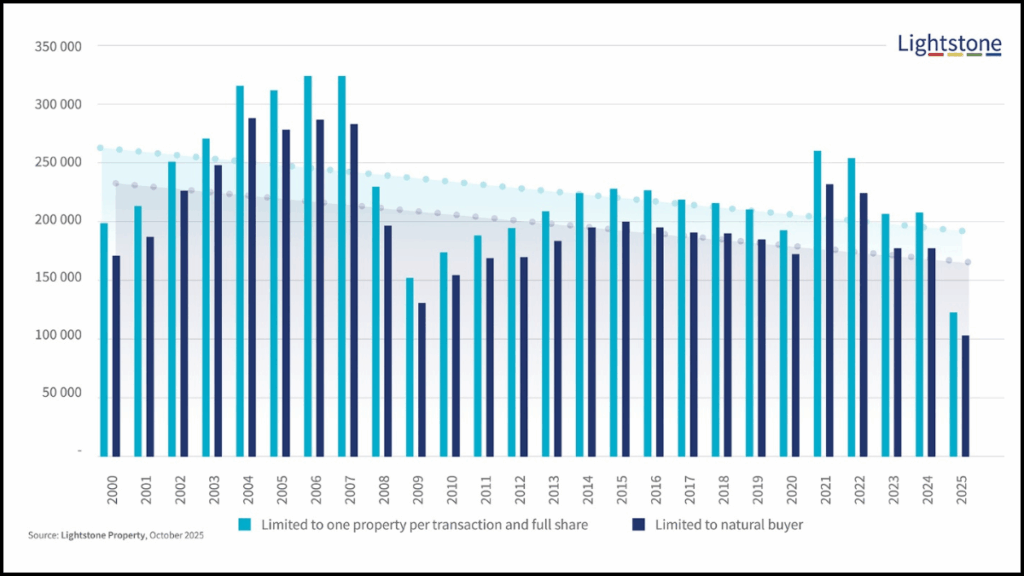

Lightstone’s focus was on single-property full-share transfers, compared with transactions involving only natural buyers.

They define ownership by “natural persons” where the property is registered in the name of one or more individuals, as opposed to being registered in the name of a company or trust.

Lightsone found that there has been a decline in property transaction volumes from 2008 to 2025. Both transactions, which were “limited to one property per transaction and full share” and “limited to natural buyer”, showed a gradual buyer decline.

Both categories showed growth in the years before 2008, followed by a crash. While recovery had been sluggish, its momentum was further hit by Covid-19 and generally weak political and economic conditions.

While volumes have not recovered to pre-2008 levels nationally, Lightstone found that there have been exceptions.

The Western Cape leads in sales volume recovery, based on 2008 benchmarks. Most positive changes are from this province, with Limpopo also showing gains.

How South Africa stacks up globally

Lightstone also compared South Africa’s post-2008 property market performance to that of the United Kingdom, the United States and Australia.

In nominal terms, Australia and many US markets recovered more strongly and more quickly than markets like South Africa and some regions in the United Kingdom once the worst of the crash had passed.

However, when considering real (inflation-adjusted) growth, many countries saw modest gains, while others experienced negative growth for specific periods.

Lightstone found that affordability deterioration was a common theme across the markets. Buyers face higher house prices-to-income ratios, and a greater burden from mortgage costs or down payments, especially when interest rates rise.

This also shows the importance of interest rates and regulations. Post-crisis credit reforms, interest rate shifts – both direction and magnitude – and central bank policy have had large effects on the market’s health and speed of recovery.

According to Lightsone, big capital cities, such as Sydney and London, tend to see more pronounced booms and more volatile swings. However, rural or less economically active regions often lag.

Supply constraints and demand pressure – from population growth, urbanisation, and migration – have played large roles in pushing up prices.

This is especially the case in Australia, specific United States coastal markets, the United Kingdom’s South East, and the Western Cape in South Africa.

The mid-2020s have faced headwinds, including rising interest rates to combat inflation, economic uncertainty, cost-of-living pressures, and inflation in supply chains and construction costs.

According to Lightsone, these factors are all contributing to a slowdown in growth or a softening in many markets.

Luxury property

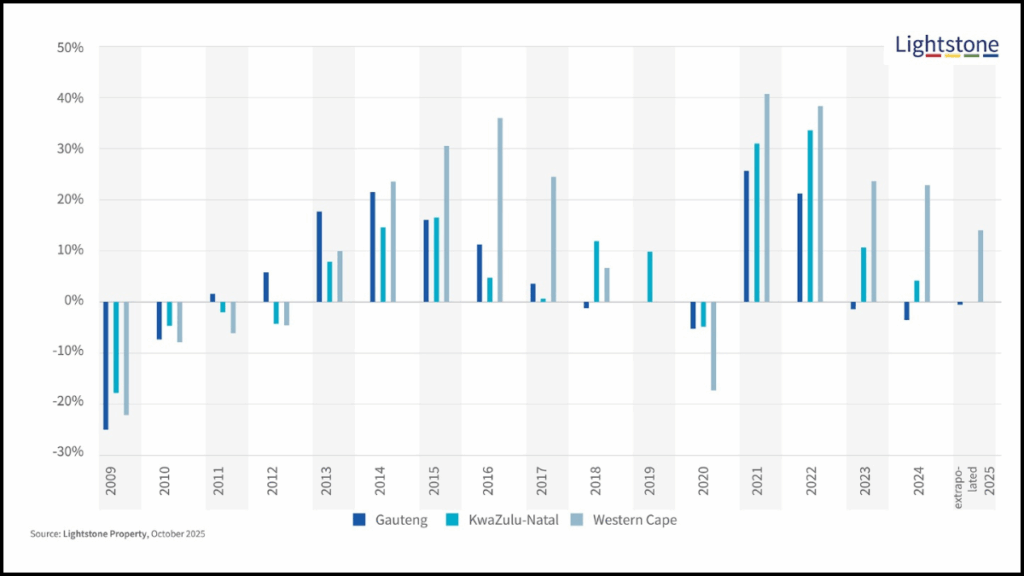

Interestingly, Lightsone found that the luxury market – which includes properties in the R2 million to R4 million range – in the three largest provinces, Gauteng, Western Cape and KwaZulu-Natal, all seemed to buck the trend.

These three provinces all recorded above 2008 sales from 2012 to 2017, and again in 2021 and 2022.

The Super Luxury house price bands – which include properties priced above R4 million – in Gauteng and KwaZulu-Natal spend more time on the market than the less expensive bands.

This trend is different in the Western Cape, however, where mid- and high-value band houses spend longer on the market in that province than luxury and super luxury properties.

Lightstone also looked at the time on market for the same value bands and provinces as it did on sales recovery.

It found a lower median time on market in the Western Cape, indicating higher demand and lower supply in that province. Houses spend most days on the market in KwaZulu-Natal, with Gauteng in between.

Pam Golding Property Group CEO Dr Andrew Golding also recently commented that there is a surging demand for luxury properties in South Africa, driven by improving economic sentiment, interest rate cuts and contained inflation.

“The outlook is further buoyed by an anticipated reduction in fuel prices and, notably, the country’s exit from the Financial Action Task Force grey list, all of which is positive for investor confidence in general,” Golding said.

“In the luxury and ultra luxury segment, the Western Cape and Cape Town in particular continues to experience high levels of demand, particularly in the City Bowl and Atlantic Seaboard,” Golding said.

In these areas, property sales of R50 million and even beyond R100 million are no longer unusual exceptions. “Prices are surpassing expectations amid significant interest from a mix of local, national, and international buyers,” he said.

Johannesburg‘s luxury market is also slowly but surely reviving, with high-net-worth buyers coming from South Africa and other African nations.

“These buyers are drawn to secure, amenity-rich estates or to established suburbs offering boomed, access-controlled streets that combine strong community appeal with enhanced security, without the constraints of estate living,” Golding said.

Proximity to leading schools, business hubs, and lifestyle amenities remains a key consideration, with Sandton, Fourways, and Midrand standing out as preferred nodes.

There is also a strong appetite for high-end coastal living in KwaZulu-Natal, where Pam Golding recently achieved R634 million in sales within just two days of launching the luxury Beachwood Coastal Estate.

Golding said this milestone sets a new benchmark for land values in the province, achieving over R10,000 per square meter.

Purchasers included primarily local buyers, as well as buyers and investors from upcountry, Dubai, and Tokyo. Villas sold for up to R25 million, apartments for around R15 million, and vacant erven reached R20 million for 1,700 m².

Below are properties for sale which fall within Lightsone’s “luxury” property price band in Gauteng, the Western Cape and KZN.

R4 million four-bedroom house in Fairland, Johannesburg

R4 million three-bedroom house in Kenilworth, Cape Town

R4 million three-bedroom house in Umdloti Beach, Durban

Comments