Gold mining has lost its shine in South Africa

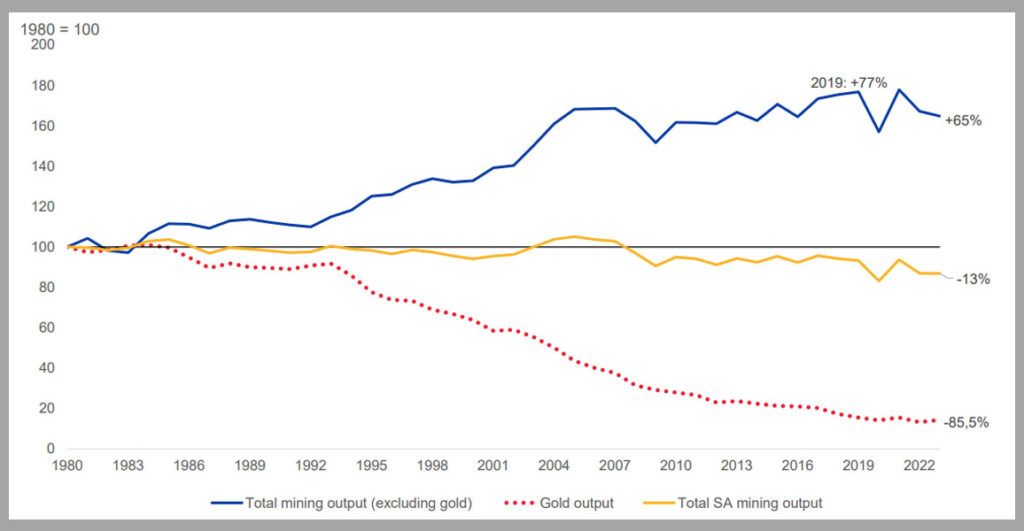

Gold mining output significantly affected South Africa’s total mining output in 2023, having declined by over 80% over the past three decades.

This was revealed in a presentation by Minerals Council of South Africa chief economist Hugo Pienaar at the Mining Indaba this week.

Pienaar explained that mining was not only the backbone of South Africa’s economy in the past but still matters today.

The sector employs over 477,000 South Africans and pays the government over R140 billion in tax and royalties annually.

South Africa’s total mining output has decreased by 13% since 1994. Excluding gold, production has increased by 65% over the past three decades.

This is because gold production has dropped significantly over the past few decades – by as much as 85.5%.

Gold and diamonds are the only commodities that have seen their output decline on average over the past thirty years.

Other commodities – like platinum group metals, coal and iron ore – have seen increased output over that period.

Diamond output has declined by 0.1% on average, while gold output has dropped by 5.8% on average.

While gold output has declined, the commodity’s price has significantly climbed over the past three decades to where it is now worth over $2,000 per ounce.

This is largely due to uncertainty and gold’s status as a “safe haven” asset to hedge against inflation and geopolitical shocks.

The declining output can be attributed to South Africa almost having depleted its gold reserves.

PwC’s South Africa Mine 2023 report warned that South Africa has, on average, less than 50 years of mining of gold, platinum, iron ore, and coal left.

The report, which analysed 29 domestic mining companies, showed that combined net income slumped to R108 billion in their latest financial year from a record R206 billion last year.

PwC said this was because of lower commodity prices, crippling power cuts, rail network constraints and rising costs.

While South Africa’s mining sector faces many challenges, one is often overlooked – the country’s dwindling reserves.

The gold industry, in particular, is only expected to exist in South Africa for approximately 27 years, with many mines coming to an end before 20 years.

South Africa has approximately 68 Moz of gold reserves left, with 84% concentrated in Gauteng.

The country’s historic heart of mining, Gauteng, has ten gold mines in operation and one mine in development.

The Free State has only six years of gold mining left at current rates, with five gold mines in operation and one project in development.

In Mpumalanga, there are currently seven operational gold mines, with one mine in development. The North-West has two gold mines.

The closure of gold mines will likely have a significant economic impact on the affected regions. For example, the five gold operations in the Free State directly employ roughly 24,000 people, and the wider economic ecosystem and supply chain will also be impacted.

Challenges relating to the effective rehabilitation of gold operations, the re-skilling of individuals, and the possible restructuring of operations for gold producers remain uncertain.

Comments