Warning for South Africans investing offshore

Equities in the United States are priced to perfection, with elevated expectations likely to lead to significant disappointment as the global environment becomes less stable and tariffs hobble global growth.

Old Mutual Investment Group chief investment officer Siboniso Nxumalo outlined the asset manager’s view on equities at the end of the first quarter of 2025 to the media at the beginning of April.

Nxumalo explained that lofty valuations in the United States have posed a problem for asset managers since March 2024, with a significant gap opening up between expectations and performance.

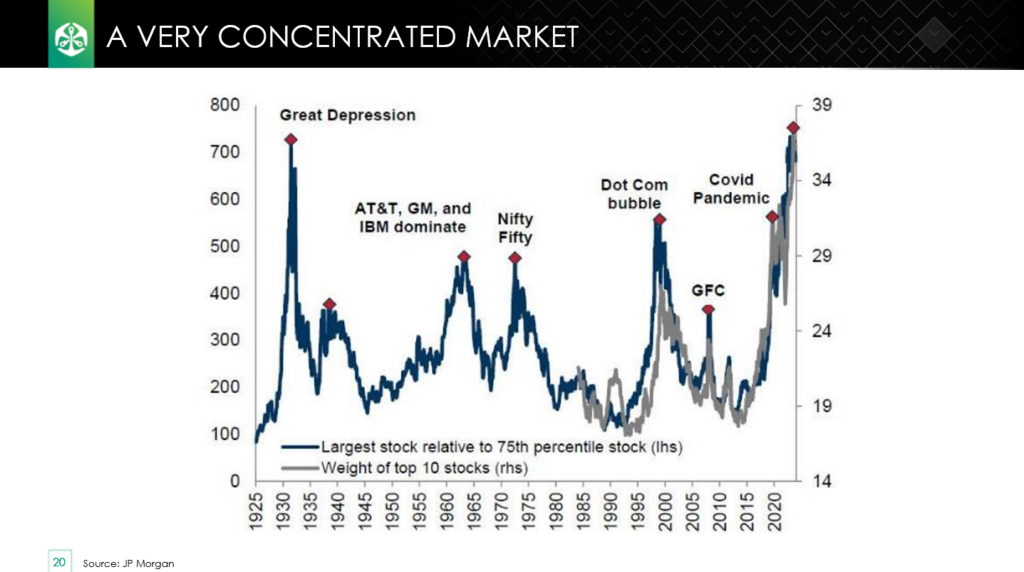

Adding to the concern is that the returns of the US equity market have been driven by a handful of companies, the Magnificent 7 – Apple, Microsoft, Google, Amazon, Meta, Nvidia, and Tesla.

The relative outperformance of these companies has created the most concentrated stock market in US history, with the top 10 stocks making up nearly 39% of the entire S&P 500.

These companies are beginning to underperform their lofty valuations, with their year-on-year growth slowing throughout 2024.

As a result, the US equity market has had a poor start to 2025, underperforming many of its peers as investors look elsewhere for returns.

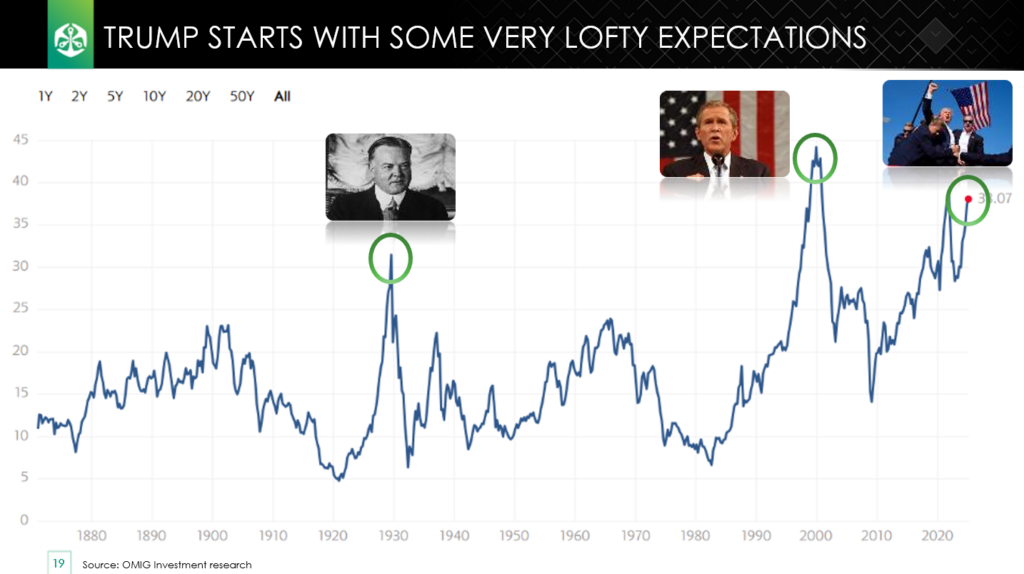

US President Donald Trump ascended to the White House at the end of January, and the stock market had its second-highest-ever price-to-sales ratio.

This exemplifies the scale of the growth expected to come from US companies. Nxumalo said these extreme expectations are likely to result in disappointment.

“This really concerns us. Whoever starts in the market at these levels generally ends up disappointing investors as assets are priced for perfection,” Nxumalo said.

The only other two times a US President began their term in office with such a high price-to-sales ratio, the market provided negative overall returns for their four-year term.

Nxumalo explained that these lofty valuations, combined with geopolitical uncertainty, elevated inflation, and fiscal fragility in the US, are likely to disappoint investors.

The graphs below show the elevated valuations attached to US equities and the extremely concentrated nature of the market.

Trump’s major challenges

Lofty valuations are not the only problem for major US companies, with the Trump administration inheriting an economy in a very difficult situation.

On the surface, the US economy looks strong, with very high GDP growth for a developed economy and unemployment hovering around all-time lows.

However, on more careful analysis, it is clear that the US economy has been propped up by significant government spending over the past few years.

Nxumalo explained that the federal government has run record deficits outside of wartime and has issued plenty of debt to fund these deficits.

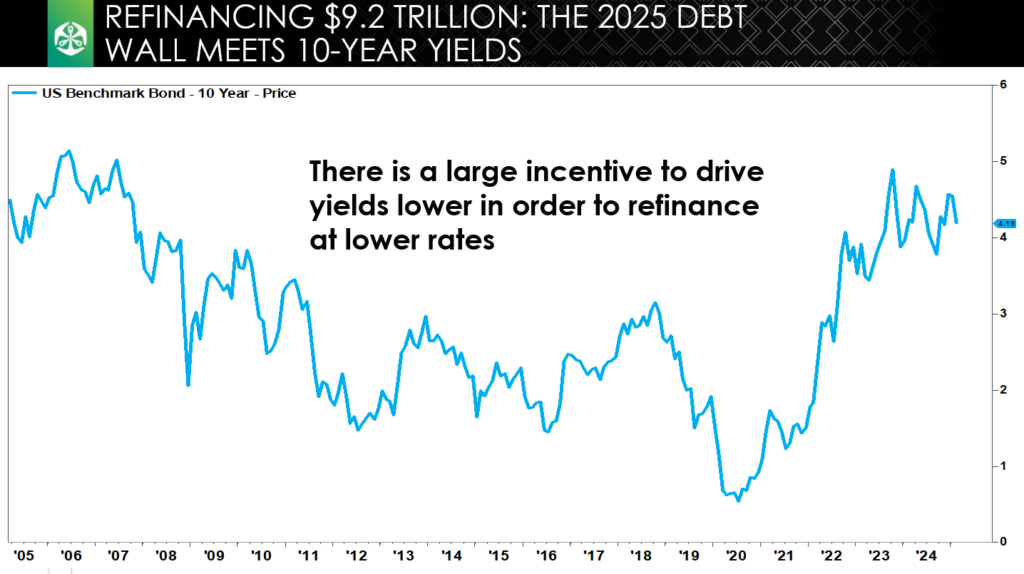

This has translated into a huge debt pile of around $36 trillion – far greater than the country’s GDP.

Traditionally, issuing large amounts of debt has not posed a problem to the US in the past two decades as it could issue Treasury bills at extremely low interest rates.

However, with inflation spiking after the pandemic and the Federal Reserve hiking interest rates, these debt payments are becoming increasingly burdensome.

The US government is now spending more money on debt repayments than on its military, with interest rates being ten times higher than during Trump’s first term.

This challenge, inherited by Trump, has been compounded by the fact that $9.2 trillion of US debt is maturing this year and will have to be refinanced at these higher interest rates unless drastic action is taken.

Nxumalo believes that this is the reason behind Trump’s planned imposition of tariffs, the creation of DOGE, and plans to cut government spending.

Trump simply has to cut costs and try to raise revenue without increasing taxes, which makes tariffs very attractive as they have been used in the past to generate revenue for the government.

Tariffs, at the scale Trump has proposed, will generate over $1 trillion in additional revenue for the US government in the next decade.

More crucially, they will knock consumer spending and economic growth, bring inflation down and push the Federal Reserve to cut rates.

This should enable the Trump administration to refinance the $9.2 trillion of debt maturing in 2025 at lower rates than the market is currently demanding.

However, all of this will slow economic growth and company earnings growth, putting pressure on US equity markets.

Combined with lofty valuations, Nxumalo said it is better to adopt a wait-and-see approach and focus on high-quality companies with pricing power rather than allocating money offshore for the sake of it.

Comments