Biggest threat to investors

The biggest risk to an investor is overpaying for an asset as the starting price often determines the performance of an investment.

This is feedback from Old Mutual Wealth investment strategist Izak Odendaal, who said the more an asset’s value is dependent on a clear outlook, the further it is likely to fall in a downturn.

An investment, such as a share or a rental property, can deliver strong and growing cash flows and still generate a disappointing total return if the starting price is too high.

Cheap shares, for example, do not escape a general sell-off or a recession, but they usually have less room to derate.

With no margin of safety, the slightest disappointment in reported or expected earnings growth can cause share prices to fall.

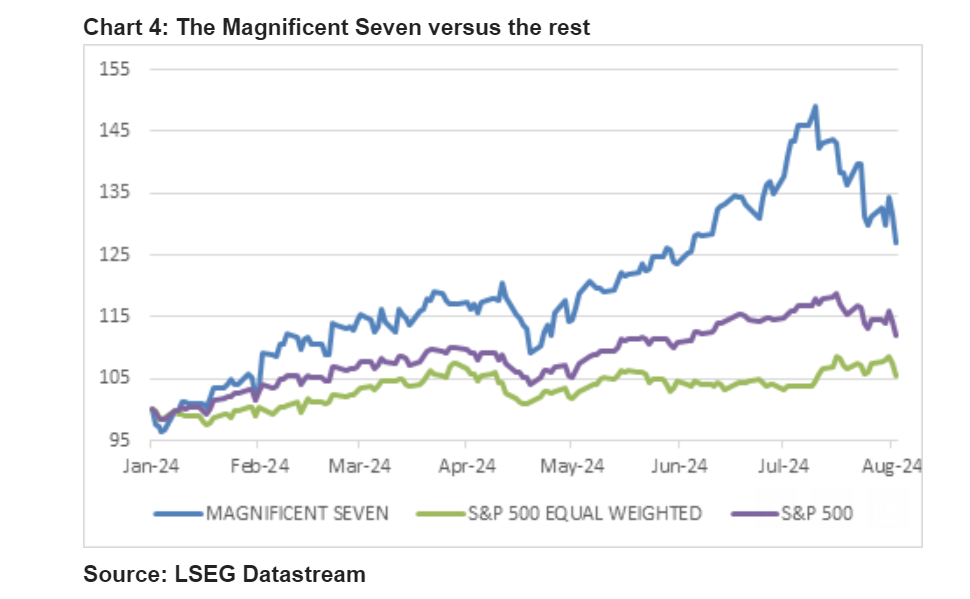

That has been the case with the mega-cap tech companies, grouped as the Magnificent Seven – Apple, Microsoft, Google, Amazon, Nvidia, Meta, and Tesla.

Since these companies now dominate global equity benchmarks, they are relevant to practically all investors.

Several of these companies reported results to the market in the last few weeks that showed ongoing strong earnings growth yet still disappointed a market that expected more.

Phenomenal companies that they are, they were seemingly priced for perfection. A lot depends on whether artificial intelligence turns out to be a truly revolutionary technology or merely evolutionary, offering incremental productivity gains.

The last time the US stock market traded at a forward price, with an earnings ratio of around 21, in 2002, the subsequent returns were flat for a decade.

It was much more of a speculative bubble back then compared to today – the Magnificent Seven are all very profitable – but the warning still stands. A high starting valuation is a headwind to longer-term returns.

The outperformance of these companies versus the rest can be seen in the graph below.

Fortunately, other areas of the global equity market are not as expensive, and investors still have much to choose from. In 2002, non-US developed market equities traded at valuations similar to US ones.

Only emerging markets were not caught up in the dotcom bubble and enjoyed a rerating and stellar returns thereafter.

Today, however, the MSCI World Ex US Index (non-US developed markets) trades at a substantial discount to the US, as do emerging markets apart from India.

It is probably a factor in the sell-off of the past few weeks. US equities have been trading at elevated valuations, implying investors were pricing in a very rosy future.

And after their incredibly strong run, no one should be surprised that there has been a pull-back, though the timing may be surprising.

This warning echoes one made by Coronation’s Chris Cheetham and Neil Padoa earlier this year.

They said investors’ fixation on the Magnificent 7 stocks is distracting them from other compelling investment opportunities and threatening the performance of their portfolios.

Other companies share characteristics of the Magnificent 7, including the ability to sustain above-average revenue growth while compounding returns on capital at an elevated rate.

Other factors are also shared, such as strong moats and sustainable competitive advantages leading to attractive rates of real earnings growth over the longer term.

However, they are not nearly as well-known and trade on attractive earnings multiples.

Market volatility is never pleasant, but one benefit is that it forces investors to grapple with the assumptions they’ve previously held.

If those assumptions have changed, it might call for a different asset allocation. If not, it is best to just stay the course, Odendaal said.

The biggest mistake is usually to react to the market volatility itself instead of to perceived changes in the fundamentals.

A US hard landing still seems unlikely, but economic growth is cooling. Elsewhere in the world, such as South Africa, it is picking up speed.

As noted above, a valuation-based approach does not protect against such volatility in absolute terms, but it does help to avoid some of the big air pockets. It also helps investors to keep an eye out for opportunities where the market overreacts.

Comments