One investment has returned 800% for Allan Gray clients in three years

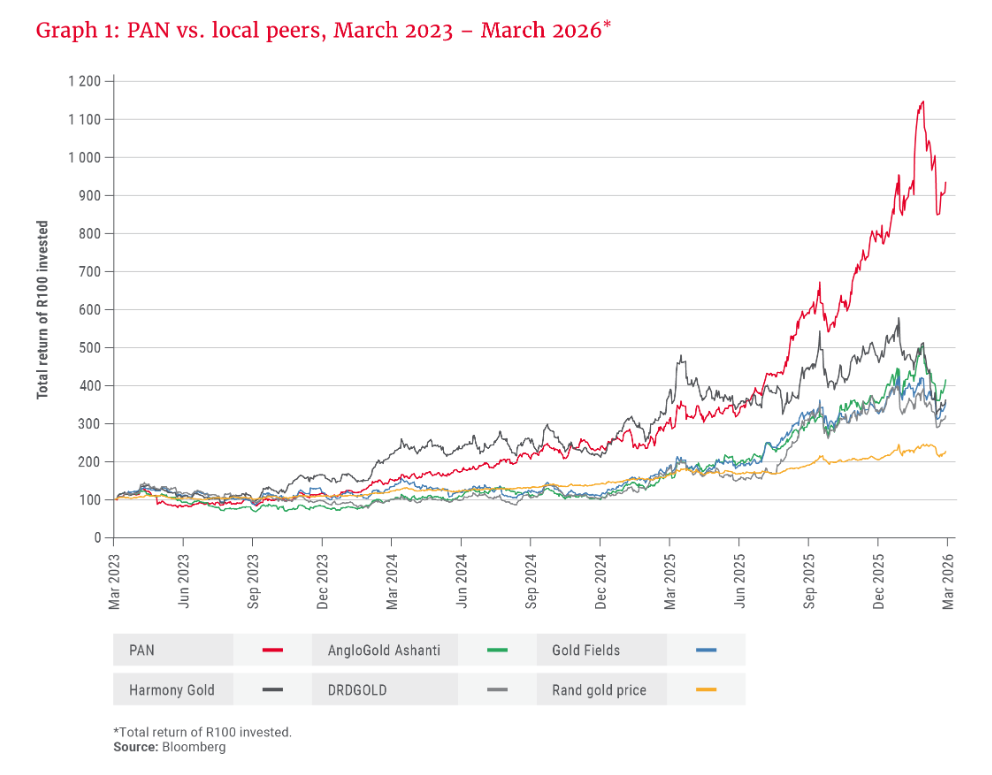

Since Allan Gray invested in Pan African Resources three years ago, its share price has skyrocketed from R3.68 per share to R31.50 per share – a ninefold (800%) increase including dividends.

This means the money invested in Pan African has doubled year-on-year for three consecutive years.

The company remains Allan Gray’s preferred exposure to the gold mining sector, analyst Andrew Boulton explained in a recent research note.

Boulton said the asset manager views Pan African’s expansion into Australia positively and expects it to continue delivering strong returns in the future.

Since listing on the JSE, Pan African has outperformed its peers, generating a compound annual return of 23% for the past 19 years.

This is higher than the market average of 11% per year over the same time frame and significantly higher than gold mining peers Gold Fields, AngloGold, and Harmony.

Notably, its performance has become increasingly decoupled from the rand gold price, indicating that business fundamentals are driving performance more than commodity fluctuations.

Boulton explained that this is down to Pan African’s so-called secret sauce, which is the reprocessing of gold tailings dumps left behind after decades of mining on the Witwatersrand.

This opportunity stems from the company’s acquisition of the Barberton gold-mining complex in South Africa, which included a group of conventional underground mines that have operated since the 1880s.

These mines, at the time of the purchase in the late 2000s, were producing 80,000 to 100,000 ounces of gold per year.

The mining complex had generated significant tailings dumps over its history, which are typically waste stockpiles generated by gold processing.

These piles often contain significant amounts of low-grade gold, partly due to historically inefficient recovery methods.

Advances in technology, combined with in-house technical expertise, allowed Pan African to extract this gold at favourable economics.

Crucially, this method of producing gold is largely mechanised, limiting operating costs and making the extraction extremely efficient.

An additional benefit is that the reprocessing of these sites enabled the land to be rehabilitated, enabling it to be used for more productive purposes after the reprocessing.

This makes Pan African one of the most efficient producers of gold in the world, which has seen its share price appreciate significantly on the back of improved fundamentals.

The flywheel of higher gold prices

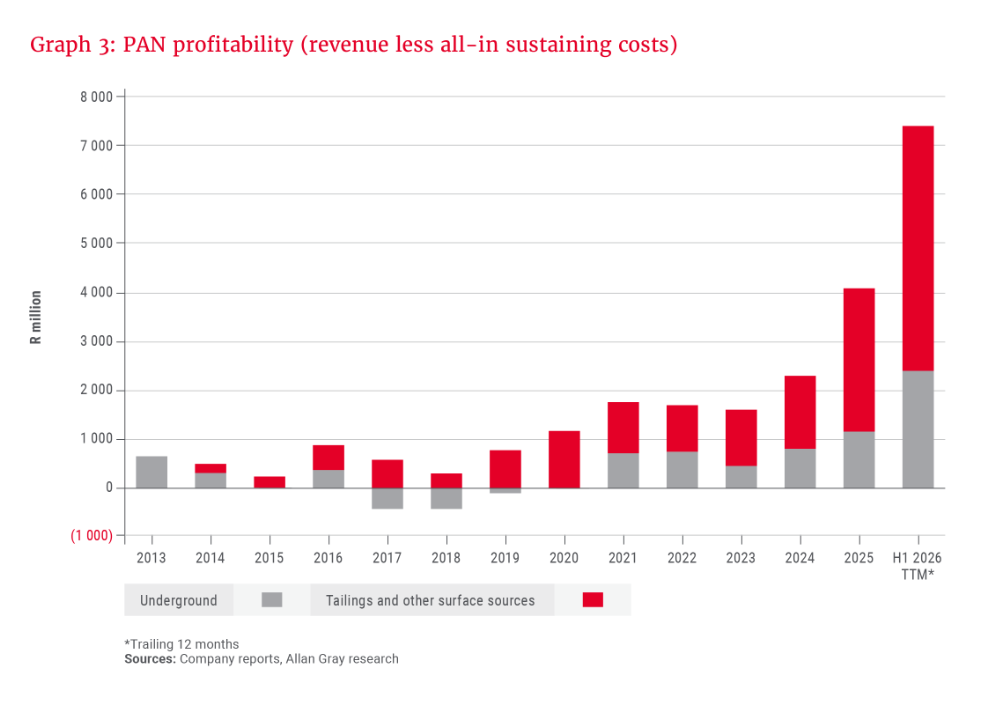

Pan African’s efficient extraction of gold came into its own in recent years, with the surge in gold prices giving it immense operating leverage.

While the costs of operation remained relatively flat due to their mechanised nature, the price the company could sell its product for rose exponentially.

This produced an extreme outcome, in that Pan African’s profit surged from around R1 billion in 2020 to over R7 billion in the last 12 months.

With the share price following fundamentals, it appreciated nine times over in the past three years, generating significant returns for Allan Gray’s clients.

Boulton said Allan Gray has realised some of these gains, with its holding of Pan African shares declining in percentage terms. The asset manager has been exposed to the company since 2009.

Pan African’s success also comes from its being able to leverage this flywheel across an extensive footprint, with it gradually expanding its operations since listing on the JSE in 2007.

The company has mimicked its success at the Barberton complex at the historical Evander complex, which had larger tailings dumps.

While Barberton tailings only produced around 20,000 ounces of gold annually, Evander tailings have produced 50,000 ounces per year since 2018.

More recently, it acquired the Mogale tailings dumps in 2023, which is producing gold at a similar annual rate to the Evander operations.

In 2025, Pan African snapped up the Tennant Creek mining complex in Australia to expand its tailings processing globally.

As a result, the increase in gold produced by Pan African from tailings has been so significant that it now exceeds the amount of gold produced from underground mines

Given that production from tailings is lower-cost, it generates a higher profit per ounce of gold and improves the company’s overall profitability.

Boulton explained that Allan Gray does not pay much attention to the short-term fluctuations in the gold price, but it will continue to watch Pan African’s expansion.

Comments