Johann Rupert’s golden child winning big as South Africans invest in luxury jewellery

South Africa’s 2025 luxury market is shifting toward “smarter” buying, with consumers favouring high-value, investment-worthy brands such as Rolex and Richemont-owned Cartier and Van Cleef & Arpels.

This was revealed in Luxity’s 2025 State of the Luxury Market in Africa report, which found that South African luxury consumers aren’t buying less, they’re buying better.

According to Luxity, 2025 marked a decisive pivot toward value-dense categories like bags, jewellery, and iconic timepieces, as shoppers focused on investment rather than indulgence.

The appetite for “forever pieces” over trend-driven goods defined this new phase of the market, as the “rational collector luxury” category continues to rise.

“Luxury buyers are becoming strategic,” said Luxity co-founder Michael Zahariev. “They understand when to buy new, and when pre-owned gives them better value or faster access. It’s less about the rush of owning and more about the return on owning.”

The luxury sector stabilised at a strong base, with the Clur Shopping Index showing a 1% decline in Luxury sector shopping from 2024 to 2025. This came after a 168% growth from 2019 to 2025.

Pre-owned Luxury continued to outperform, with Luxity growing 27.86% from 2024 to 2025 and 594.15% since 2019.

With luxury buyers now focusing more on durability and resale value, the strongest momentum came from categories that combine emotional value with financial endurance, pieces that age well and resell even better.

In 2025, bags and jewellery took the lead as shoppers redirected attention from fast-turnover fashion toward tangible assets.

Bags advanced to 21.59% of search share, up 14.6% year on year. Jewellery climbed to 8.93%, a 43.8% year-on-year increase.

These categories embody consumers’ shift toward investment-grade fashion, high utility, durability, and inherent tradeability.

By contrast, more transient purchases saw softening. Shoes slipped to 22.46%, a 10.2% decline from the previous year, and wallets declined by 21.3%.

This reweighting toward permanence shows a shopper base maturing and prioritising pieces that hold or grow in value rather than fade with the season, Luxity said.

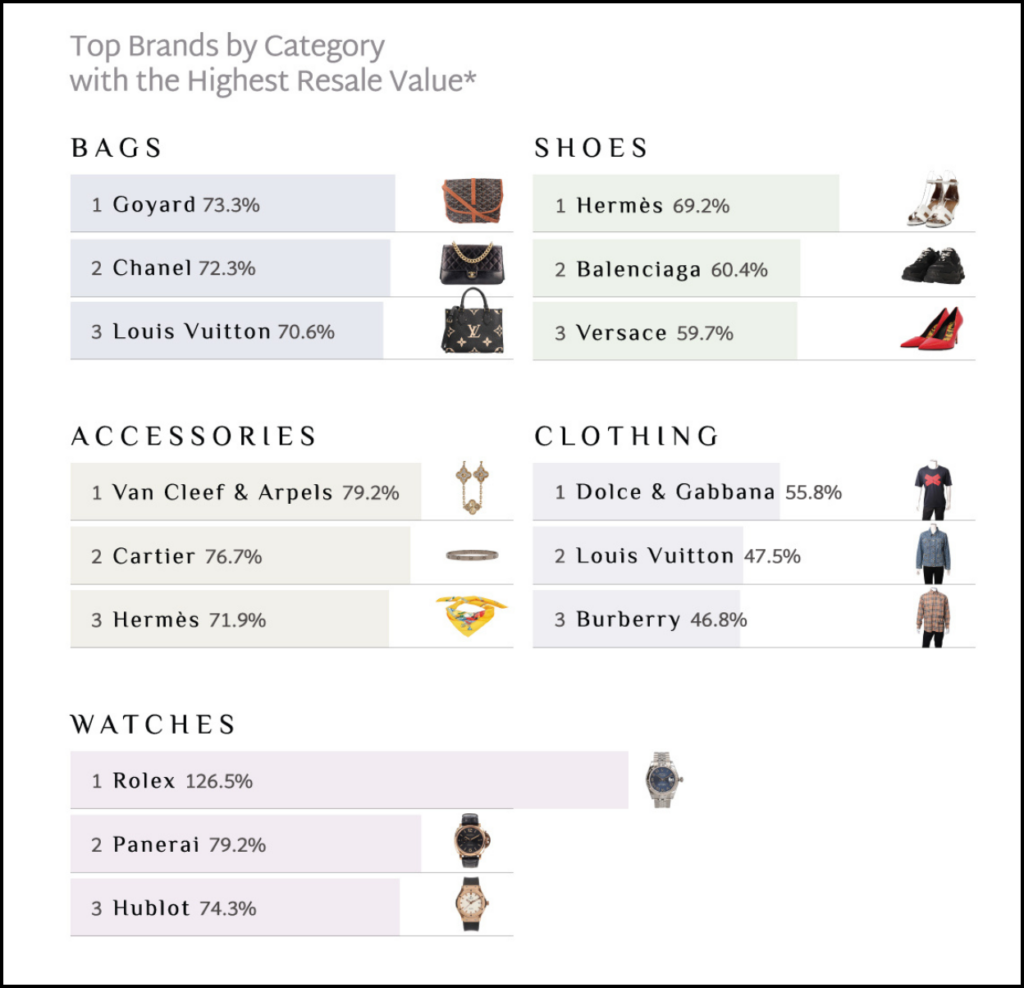

South Africa’s favourite luxury brands

Rolex set a record, reselling at an average 126.5% of retail, up more than 20% year-on-year, cementing watches as South Africa’s most stable luxury asset class and a strong alternative investment.

The brand held South Africa’s top spot in the luxury watch and jewellery category. Cartier, which came in second, remains the everyday value anchor.

Van Cleef & Arpels took third spot for its enduring desirability and resale resilience across signature lines.

Both Cartier and Van Cleef & Arpels are owned by billionaire business Johann Rupert’s Swiss luxury goods holding company, Richemont.

Other hard-luxury brands like Bulgari and Hermès also continued to outperform, reinforcing the “value floor” that anchors the market.

Luxity explained that collectors are treating these names less like accessories and more like portable stores of value.

In the atelier category, Hermès, Chanel, and Louis Vuitton continued to dominate with deep liquidity and strong value floors.

Notably, for the first time, discovery spread noticeably beyond the “big two” of Louis Vuitton and Gucci. Their share of brand searches dropped from nearly 30% to just over 21%.

Overall, Luxity said demand is broadening, and the market is becoming less top-heavy. Smaller houses like Bulgari, Givenchy, and Montblanc, also owned by Richemont, are now finding new audiences.

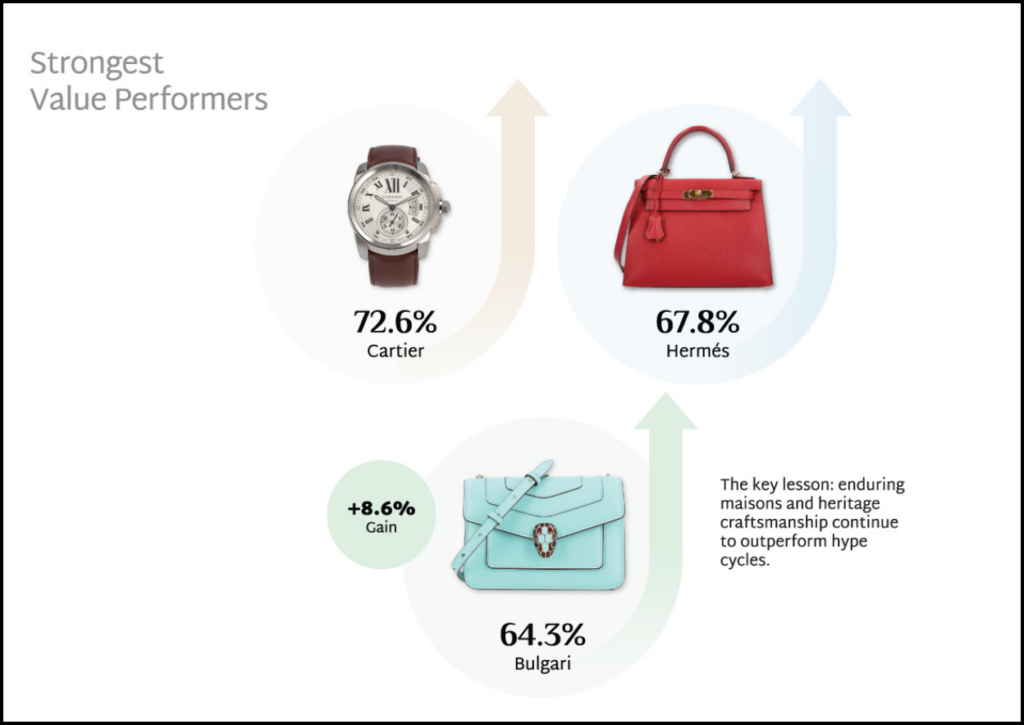

The strongest value performers remained remarkably consistent, as Cartier (72.6%) and Hermès (67.8%) led the pack, both inching upward.

Bulgari experienced an 8.6% gain, joining the elite “value floor” tier. Meanwhile, names like Marc Jacobs and Bottega Veneta cooled, reflecting the correction from pandemic-era fashion exuberance.

Brands with the best resale value

Luxity observed similar trends in brand searches, with South Africans exploring a broader range of luxury brands in 2025.

While flagship names like Louis Vuitton and Gucci continued to dominate awareness, their collective grip on search activity loosened slightly.

Search concentration fell, with the top 10 brands accounting for 53.85% of total search share, down from 61.70% the previous year. Louis Vuitton and Gucci together declined to 21.5%, down from 29.6% in 2024.

Luxity said this signals a growing consciousness and appreciation for a variety of brands, and a move away from a focus on staple luxury brands.

Notably, they also pointed out that the correlation between brand search volume and retained value was weak.

This revealed a tactical opportunity in under-discovered brands like Bulgari, Givenchy, and Montblanc, which delivered strong resale metrics but remain under-marketed.

On the other hand, over-hyped names such as Prada and Burberry over-indexed on attention but underperformed on resale.

At the summit, Cartier reclaimed its lead with an average resale value of 72.6% of retail and an average sale price of around R44,700, affirming its dominance in the multi-disciplinary hard-luxury segment.

Hermès followed closely at 67.8%, continuing its long-standing reputation for unmatched scarcity and desirability.

Chanel (64.4%), Bulgari (64.3%), and Louis Vuitton (64.2%) formed a tight cluster, evidence of a stable “value plateau” across the most sought-after fashion maisons.

New entrants such as Balenciaga (60.7%) and Montblanc (59.1%) broke into the top ten, signalling that well-priced contemporary and accessory-driven luxury can compete on retention when brand equity is consistently managed.

Comments