The forgotten way the United States can hurt South Africa

The bursting of the artificial intelligence (AI) bubble in American technology stocks can have severe consequences for the South African economy and its financial stability.

American technology giants, particularly the Magnificent 7 of Apple, Google, Microsoft, Meta, Amazon, Nvidia, and Tesla, have seen their valuations soar in recent years since the launch of ChatGPT in November 2022.

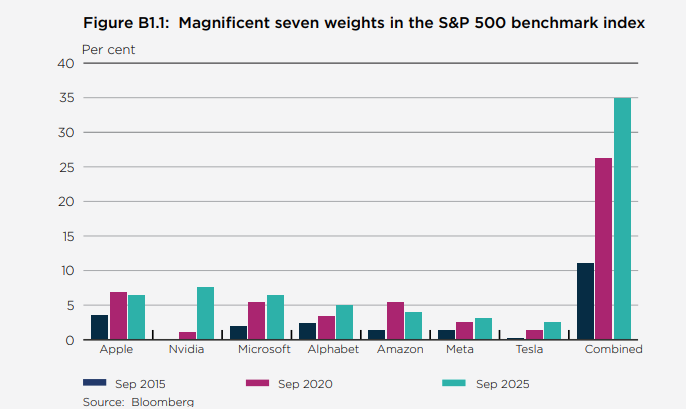

This has made the fortunes of global stock markets increasingly tied to this handful of companies, which now make up 35% of the S&P 500 index.

With American equities making up over 60% of global market capitalisation, this means the world is increasingly exposed to the performance of these companies.

While these companies may seem far removed from the South African economy and financial system, the old saying that no events are unconnected in markets rings true.

This was emphasised by the Reserve Bank in its latest Financial Stability Review, which outlined how the increased concentration of global markets poses a threat to South Africa.

The Reserve Bank noted that a sharp decline in the value of the Magnificent 7 could trigger a tightening in global financial conditions as risk aversion rises.

“Historically, such episodes have been unfavourable for emerging markets, leading to portfolio outflows, weaker exchange rates, and higher risk premia,” it said.

South Africa is particularly vulnerable to these external shocks, given the country’s stagnant economy, high government debt burden, and the fact that it is a very open economy.

“For South Africa, these spillovers could amplify domestic market volatility and weigh on asset prices, particularly in the equity, fixed-income and currency markets,” the Reserve Bank said.

The United States plays an outsized role in global financial markets due to it having the largest economy and the world’s deepest capital markets.

This is the reason why the Reserve Bank, for example, watches the movements of the US Federal Reserve so closely when making its own decisions.

With regard to investing, the United States’ equity markets have sucked up global liquidity over the past 15 years due to its relentless economic growth, innovation, and deep capital markets.

While this picture may be changing slightly as investors look elsewhere for safety, the American equity market remains dominant, and its tech giants command trillions of dollars in market cap.

For investors searching for returns or to participate in the AI boom, it is hard to look beyond the United States and its technology giants.

The AI bubble

The Reserve Bank analysed whether the AI-driven boom in shares of certain companies is justified in its Financial Stability Review.

It noted that the recent surge in equity valuations has been driven by a small group of leading technology giants in the United States, with the Magnificent 7’s combined market capitalisation accounting for 35% of the S&P500 index at the end of September.

This is more than three times their share of 11% in 2015, with the concentration highlighting the increasing dependence of global equity markets on the performance of a small group of companies.

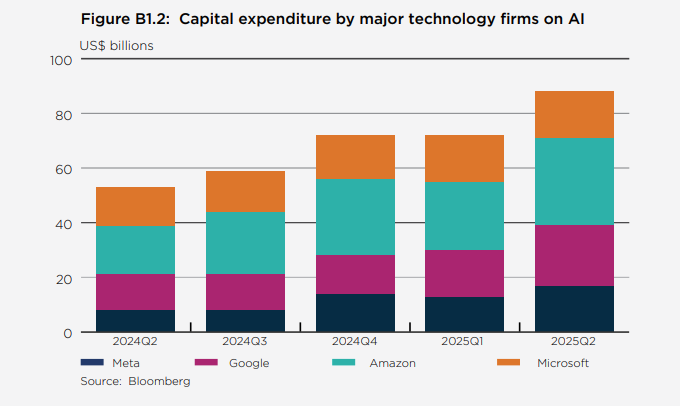

Since the second quarter of 2024, these leading technology companies have significantly increased their investments in AI-related infrastructure.

This investment has been made in anticipation of future profits, which are likely to come with the only questions being how long and how much.

These outlays have fuelled investor optimism and have emphasised the concentration of market performance and corporate spending within a handful of firms.

The Reserve Bank warned that this increases systemic exposure should AI profits undershoot expectations, even by a small margin.

There are signs that point to the AI-related spending not translating into profits as yet, with a recent MIT study finding that 95% of firms have a year to realise measurable returns on their AI investments.

This has raised questions about the sustainability of current valuations and how long these technology companies can continue to invest heavily in infrastructure without much return.

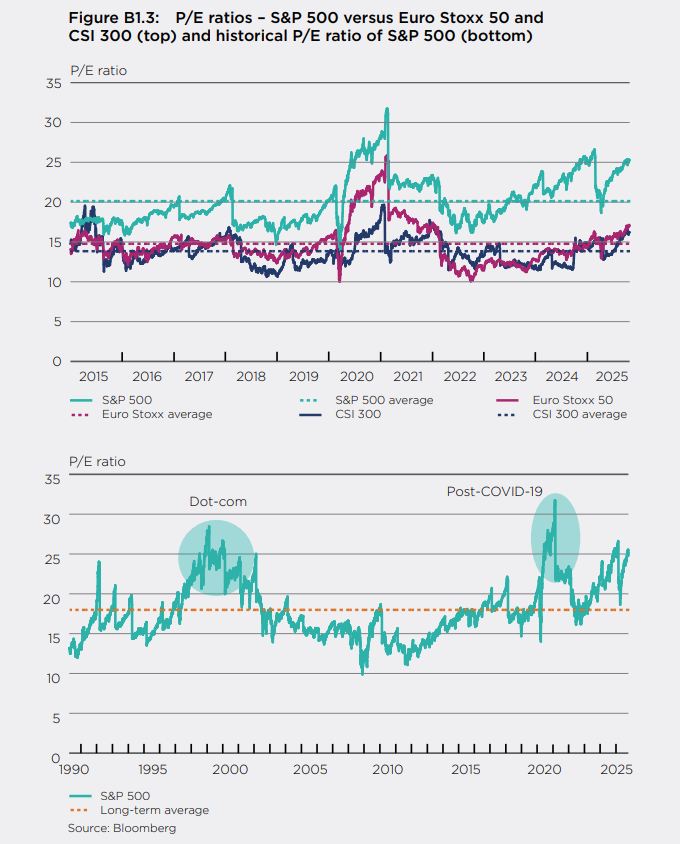

The concentration of capital in the Magnificent 7 has led to the broader US equity market trading at an elevated price-to-earnings ratio compared to historical norms and global peers.

However, valuations still remain below the peaks seen during the dot-com bubble and in the immediate aftermath of the Covid-19 pandemic.

With US equities accounting for over 60% of global market capitalisation, the consequences of a correction would extend far beyond America.

A sharp reassessment of valuations could trigger a tightening in global financial conditions, as risk aversion rises and liquidity conditions deteriorate.

Comments