End of an era for the United States dollar

The United States dollar is undergoing a notable shift, as investors are losing faith in the currency and dollar-based assets.

While the US dollar will remain the world’s reserve currency, experts broadly believe 2025 will mark the start of a shift in its behaviour and role in capital markets.

Nedbank chief economist Nicky Weimar, who recently spoke at the Nedgroup Investments Treasurers’ Conference, said the dollar has been weak in 2025 so far,

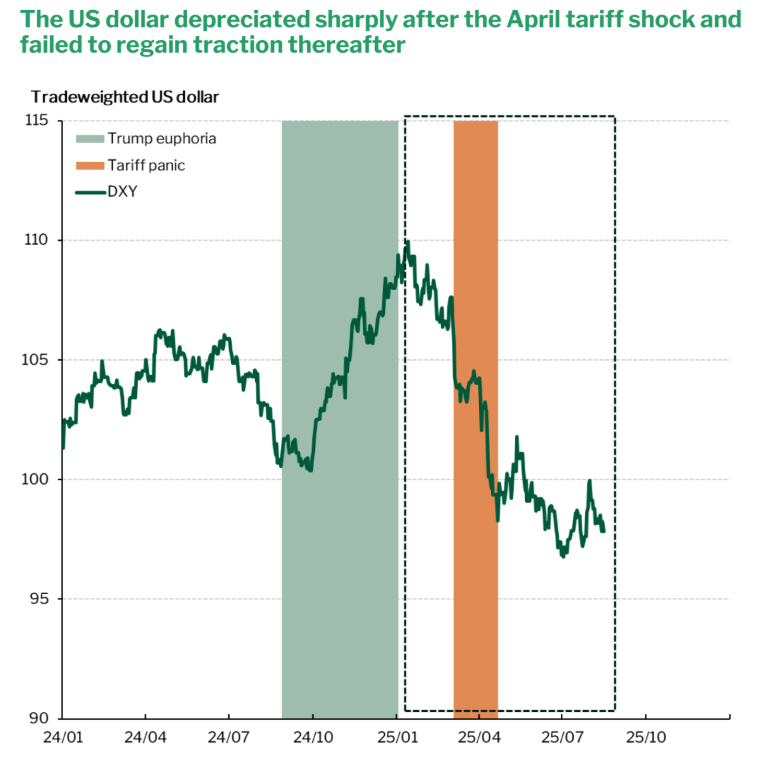

The start of this year has been the worst for the US dollar since 1973, with the currency down over 11% against the euro and over 7% weaker against the British pound in the year to date.

Weimar pointed out that this is unusual, as the protectionist measures implemented by the United States in 2025, particularly the Trump administration’s tariff policies, would normally strengthen the dollar.

However, this has not happened, and after US President Donald Trump’s so-called ‘Liberation Day’ on 2 April, the dollar has come under immense pressure and has not found its way back to stronger levels since.

One factor Weimar attributed this pressure to is market expectations for an interest rate cut in the United States later this year, as the country’s economic growth is expected to slow.

The interest rate differential another rate cut would create between the United States and other countries could be behind the pressure on the dollar.

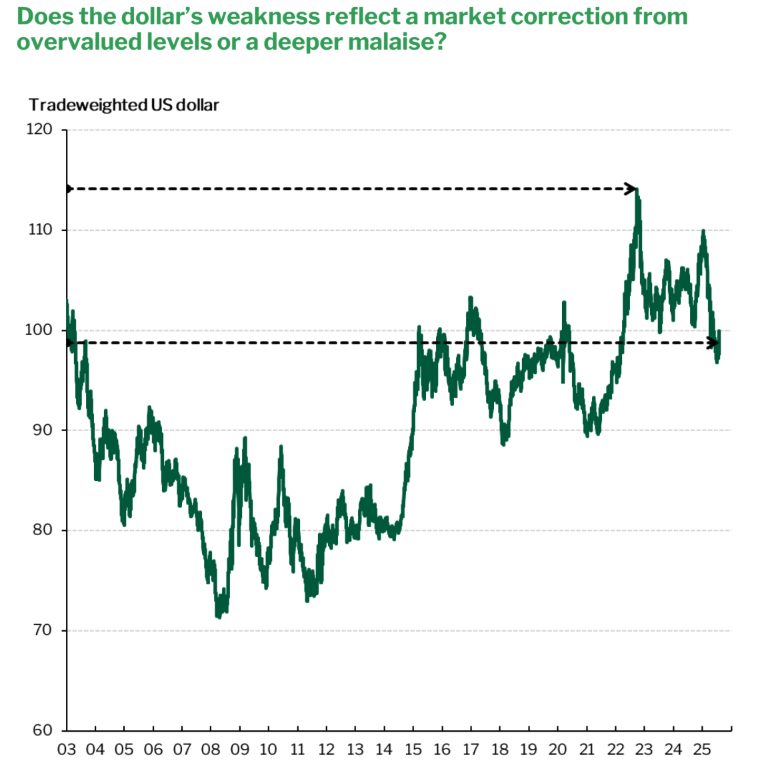

In addition, she said the dollar’s weakness in 2025 to date could be attributable to a market correction from overvalued levels.

However, Weimar said this could also be a sign of a deeper malaise – the gradual loss of faith in United States’ economic policy.

Since the Trump administration took office, uncertainty and volatility have become commonplace, with trade policies waxing and waning and no country truly sure of what the next executive decision could bring.

In light of this instability, Weimar explained that investors and the business community are “diversifying out of US dollars”.

The graph below, courtesy of Weimar, shows the US dollar’s fluctuations since the start of 2024.

Dollar dominance here to stay

Weimar emphasised that this does not point to a complete shift away from dollars, but rather investors hedging against the impact of a volatile currency.

“We will always be using dollars. It is still the world’s deepest, most liquid market. But at the margin, which is what impacts foreign exchange rates, people are switching out of US dollars,” she said.

“They are hedging their bets. The Swiss franc is very popular, the euro is popular, the British pound if they must, and the central banks are stocking up on gold.”

This response means the dollar is unlikely to weaken much further, but it will also not bounce back to the strong levels it once saw.

Weimar’s view was shared by the Reserve Bank’s head of market operations and analysis, Bafundi Maronoti, who also spoke at the Nedgroup Investments conference.

Maronoti attributed the dollar’s weakness in 2025 to two factors – a broad-based loss of confidence and a shift in the United States’ economic realities.

The first factor, a broad-based loss of confidence in the US dollar, results from prevailing uncertainty in the United States.

This uncertainty led to the “hedging” actions Weimar described, which has added fuel to US dollar weakness.

Maronoti said it has been interesting to see that institutional investors, especially from Asia, who had unhedged exposures to the US, did not necessarily sell out of the US.

Rather, they have opted to put FX swap and FX forward overlays on these positions to protect themselves against further weakness in the US.

“I think that’s what has been one of the biggest struggles of this weakness that we’ve seen in the US dollar,” he said.

With regard to the second factor, a shift in US economic realities, Maronoti explained that the risk of stagflation in the United States is a notable concern.

The graph below, courtesy of Weimar, shows the trade-weighted US dollar index from 2003 to 2025, with a focus on its recent decline.

Cracks starting to show

Like Weimar, Maronoti emphasised that the US dollar is here to stay despite questions surrounding the greenback’s continued dominance as a reserve currency.

“I think this has had an impact, especially on surface-level sentiment because if there’s any indication that there’s gonna be a move away from the dollar structurally, then the dollar becomes weak,” he said.

“What we have been thinking about here is whether we are now starting to see or are in the early stages of a regime shift in how the dollar behaves because of the structural shifts in the role that the dollar plays in global capital markets or the economy itself.”

“Personally, I don’t necessarily think we are there yet. The dollar still plays a very dominant role in global financial markets, whether it’s in FX transactions, whether it’s where the dollar is in use as a currency trade or as a share of global FX reserves.”

Maronoti explained that the dollar’s dominance in this regard is also a “pillar” supporting the currency’s strength.

He said there are no indications that some structural levers supporting the US dollar have shifted meaningfully in a way that would put the greenback on a sustained path to weakness.

In addition, he said the sheer size of the US capital markets and the ability to substitute that within a relatively short space of time make a meaningful move away from the dollar difficult.

“While we do see that there are changes in the popularity of the US dollar and that there is diversification that’s taking place, I think it’s gonna be a while still before we see meaningful shifts in those structural drivers of the dollar,” he said.

Comments