Bad news about inflation and interest rates in South Africa

The Reserve Bank is unlikely to cut interest rates further in 2025 as inflation is expected to rise throughout the rest of the year as beneficial base effects roll out.

Furthermore, the ‘unofficial’ shift to a lower inflation target means that inflation is already at the Reserve Bank’s 3% goal.

Another complicating factor is the impact of US tariffs on South Africa’s economy, as it clouds the outlook for local production and demand.

This is feedback from Old Mutual Wealth’s chief investment strategist, Izak Odendaal, who outlined a longer-term view of interest rates after the Reserve Bank shifted its target unilaterally.

Odendaal explained that an interest rate cut was widely expected last week, with the market only really moving due to the announcement that the Monetary Policy Committee (MPC) will aim for 3% inflation.

The National Treasury must approve a formal lowering of the inflation target, and discussions in this regard are still ongoing. Indeed, the Finance Minister did not seem pleased with the “unilateral” announcement.

However, strictly speaking, the MPC is simply shifting its focus within the existing target range, as it has done before.

When inflation targeting was introduced in 2000, the upper end of the range was generally seen as the de facto goal for many years before the MPC explicitly started aiming at the midpoint around 2018.

There are short and long-term implications of moving to a lower inflation target, even if unofficially, Odendaal said.

In the near term, interest rates are unlikely to fall further as inflation is now in line with the new goal, meaning the July cut is likely to be the last one for the year.

Headline inflation rose slightly to 3.1% year-on-year in June, but core inflation, which excludes food and fuel prices, fell to 2.8%, the lowest since 2021.

Inflation is likely to rise modestly in the next few months, partly as the favourable base effect rolls out and the impact of higher electricity tariffs becomes clearer.

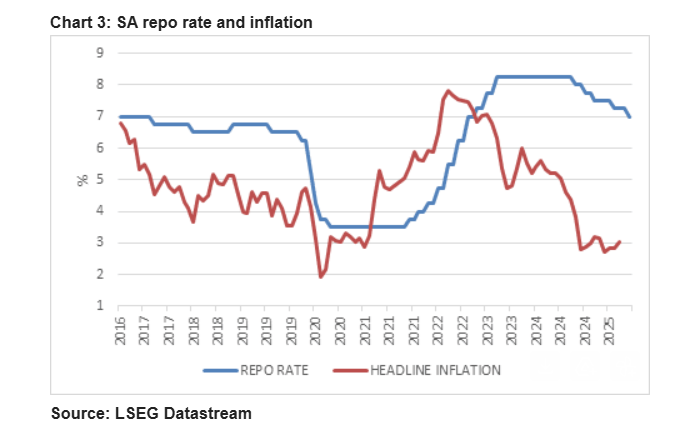

South Africa’s repo rate and headline inflation can be seen in Odendaal’s graph below.

Benefits of a lower target

A lower inflation target is expected to bring immense benefits over the long run, with faster economic growth and healthier government finances being touted as advantages.

These advantages will be achieved primarily through lower interest rates from the Reserve Bank as inflation moderates around a 3% target.

Over the long term, interest rates will trend lower if the Reserve Bank manages to anchor inflation and inflation expectations around 3%, Odendaal said.

Success is not guaranteed, particularly because most of the inflationary pressures are from the supply side, notably municipal and utility costs, which are not responsive to interest rates or broader economic conditions.

Administered prices, such as electricity and water tariffs, have become increasingly unanchored from inflation, creating significant upward pressure on inflation.

The Reserve Bank has consistently warned that elevated administered price increases, particularly electricity tariffs, complicate the process of lowering interest rates.

Another major source of upward pressure will come from the government’s deteriorating financial health, which has pushed the risk premium upwards over the past decade.

The Reserve Bank has to compensate for this risk premium to attract capital to the country and support the value of the rand.

As the risk premium grows, interest rates have to compensate further by being relatively higher. This limits economic growth by keeping lending subdued.

It is also important to remember that inflation will always move in cycles, even if the trend is structurally lower.

Nonetheless, the progress in anchoring inflation expectations around 4.5% suggests that 3% will be doable over time.

This will have a positive long-term impact on South African bonds, equities and property, since lower interest rates will make these longer-duration assets more valuable.

The depreciating trajectory of the rand against hard currencies will also bend lower, since the weakness of the currency is tied to the gradual loss of competitiveness that the theory of purchasing power parity implies.

Comments