South Africans can reduce monthly home payments

In the current economic climate, many South Africans may be struggling to meet their mortgage obligations. However, experts suggest that there are ways to reduce monthly payments.

These include negotiating a lower interest rate with their bank, renting out a portion of their home, and contributing additional funds towards their home loan when possible.

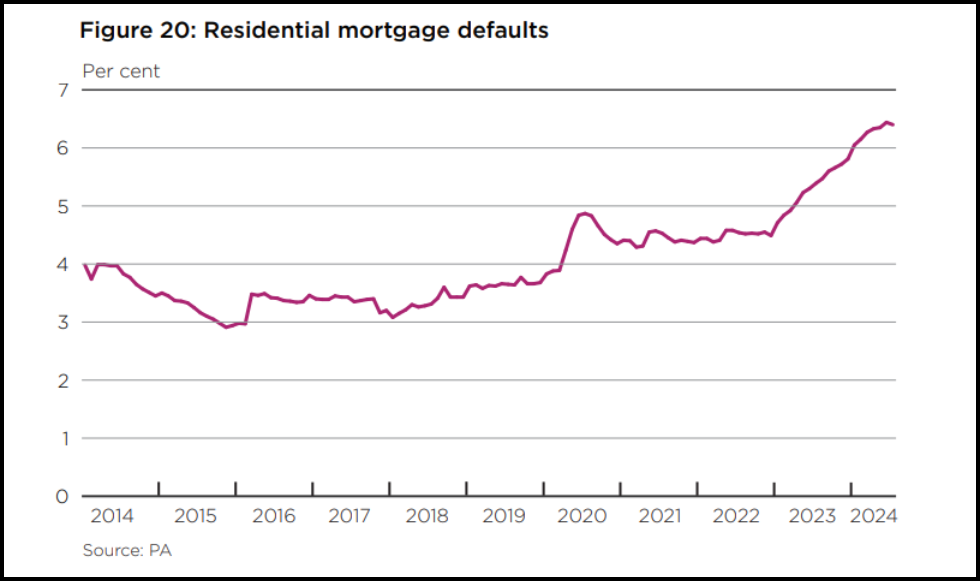

In the Reserve Bank’s latest Financial Stability Review, released in November 2024, it revealed that residential mortgage defaults have risen strongly over the past two years.

The pressure on households has been evident since interest rate increases began in November 2021. Following a 475-basis-point increase in interest rates, by mid-2022, borrowers faced growing challenges in fulfilling their loan repayments.

Homeowners have been particularly affected by these high interest rates, experiencing a significant surge in their monthly repayments due to the Reserve Bank’s attempts to control inflation.

Notably, interest rates have increased by 475 basis points since November 2021, reaching a 15-year peak and substantially raising the cost of home financing.

For example, the monthly repayment on a R1.5 million home had climbed by R4,600 before the Reserve Bank initiated its rate cuts in September 2024.

It has also been observed that many homeowners purchased properties beyond their financial means during the pandemic, taking advantage of the Reserve Bank’s low interest rates aimed at economic stimulation.

Consequently, there has been a sharp rise in residential mortgage defaults over the last two years, reflected by an increase in homeowners unable to make their monthly payments within a 90-day period.

Data from the Prudential Authority confirms this trend, indicating that residential mortgage defaults have surpassed 6% of all home loans, nearly doubling the historical average.

Even though the Reserve Bank has since entered a rate-cutting cycle, many households are still feeling the strain.

TransUnion’s Q1 2025 Consumer Pulse study revealed that 42% of respondents stated that their household income is not keeping up with inflation, despite inflation being at the lower end of the Reserve Bank’s target range.

Worryingly, 38% of respondents in Q1 2025 said they could not pay at least one of their current bills and loans in full, up from 35% in Q4 2024.

Lowering home loan repayments

With many households struggling to meet their debt obligations, Adrian Goslett, Regional Director and CEO of RE/MAX of Southern Africa, explained that there are strategies homeowners can consider to lower their home loan repayments.

In the first place, they can approach their bank to negotiate a lower interest rate, which would lead to reduced monthly payments.

If your loan is in good standing and your property’s value has increased, the bank might view you as a lower-risk borrower and offer a more favourable rate.

Extending the repayment period of your home loan can decrease the monthly instalment amount. However, Goslett warned that this should only be considered as a last resort.

For instance, resetting a 20-year loan back to 20 years or extending it up to 30 years spreads the debt over a longer period, reducing each payment. However, this will result in paying more interest over the life of the loan.

Another practical way homeowners can reduce their monthly home loan instalments is by generating rental income through renting out a portion of their home.

Converting a spare bedroom, cottage, or separate entrance into a rental unit can provide an additional revenue stream that significantly offsets home loan payments.

This not only alleviates the financial burden but can also accelerate the repayment of the loan principal, helping homeowners achieve financial freedom sooner.

As counterintuitive as it may sound, Goslett said that contributing additional funds towards your home loan can significantly reduce the principal amount.

This will result in lower interest charges, a shorter loan term, and a smaller instalment amount on future repayments.

Paying extra in the months when finances are available can help make the repayments more manageable in the months when finances are limited.

Whatever strategy homeowners choose to implement, Goslett stressed that the most important thing is to avoid falling behind on the home loan repayments. Even temporary setbacks can quickly escalate into serious financial difficulties.

“Missing instalments not only incur penalties and additional interest charges but can also negatively impact one’s credit score, limiting future financial opportunities.”

In cases where homeowners foresee challenges in meeting their repayment obligations, Goslett advises them to proactively communicate with their financial institution to discuss possible solutions.

“Taking early action can help prevent manageable issues from spiralling into long-term financial distress, ultimately safeguarding the homeowner’s property and financial stability.”

Comments