Plan to save South Africa’s finances

South Africa needs to implement an ambitious programme of fiscal and structural reforms to stabilise the government’s debt load and reignite the local economy.

This includes removing structural barriers to growth, such as onerous regulations and inefficient logistics, while also significantly reducing the government’s reliance on debt to fund its spending programmes.

The Organisation for Economic Co-operation and Development (OECD) laid out this plan as part of its latest economic survey on South Africa.

It outlined some of the country’s significant economic challenges and the reforms needed to boost the local economy.

One of the major issues the OECD identified was the continued rise in the government’s debt burden, with debt-servicing costs beginning to crowd out spending in other areas.

“To reduce fiscal risks and place public debt on a downward trajectory, an ambitious programme of fiscal and structural reforms that achieves higher primary surpluses and GDP growth is necessary,” the organisation said.

Structural barriers to growth, which result in low fiscal spending multipliers and the potential crowding-out of private investment, combined with an already high debt-to-GDP ratio, limit the government’s ability to raise more debt to fund its programmes.

Likewise, the narrow tax base combined with sluggish growth implies that relying on simple tax rate increases will likely be ineffective at increasing revenues and generating primary surpluses.

Thus, key areas of focus for the government must be economic growth and fiscal consolidation, as only by combining both can the debt load be stabilised and reduced.

Faster economic growth will lead to higher tax revenues, without the need to increase the burden on individuals and companies.

Fiscal consolidation, on the other hand, will ensure that the government spends less than it brings in, excluding debt-servicing costs, enabling it to slow the rise in the debt load.

However, even with both of these programmes being successful, it will not be enough, the OECD warned.

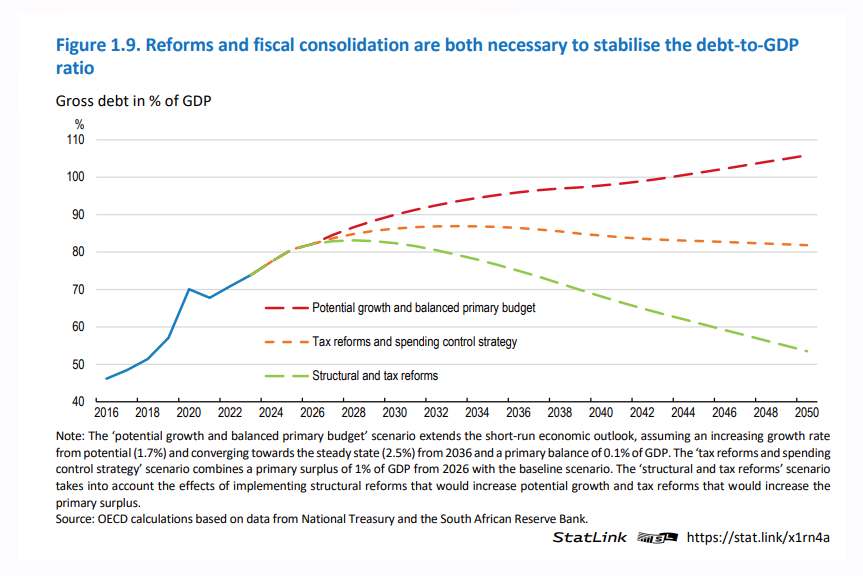

The potential growth and balanced primary budget scenario assumes that the economy operates at a potential growth rate of 1.7% as electricity shortages are resolved, allowing growth to gradually reach a steady state of 2.5%.

The government is also expected to follow through with planned fiscal consolidation, resulting in a modest primary balance surplus of 0.1% of GDP.

This scenario assumes recent reforms will materialise, hence growth and the deficit would deviate significantly from the past decade’s average economic growth of 0.9% and primary balance deficit of 1.3% of GDP.

Yet, this scenario would likely be insufficient to stabilise the debt-to-GDP ratio, which could reach almost 110% by 2050. This can be seen in the graph below.

Tax reforms and spending control

The OECD stated that South Africa needs to be more aggressive in implementing structural reforms and spending controls to begin reducing its debt burden.

This programme of tax reform and spending controls involves stronger fiscal reforms, including a substantial reduction in transfers to state-owned enterprises (SOEs).

Crucially, this also involves a significant broadening of South Africa’s tax base to raise additional revenue, instead of tax increases on the current narrow base.

While the OECD praised the National Treasury’s efforts at fiscal consolidation, it also noted that spending controls need ot made much stricter.

All of these programmes could result in the primary surplus increasing to 1% of GDP over the long term, stabilising government debt at its current high level.

“A meaningful and sustained reduction in the debt-to-GDP ratio would require a more comprehensive scenario of structural and tax reforms,” the organisation said.

This would entail a concerted fiscal effort to boost government revenues, primarily through spending controls and measures focusing on increasing the tax base rather than overall tax rates.

This approach also requires an ambitious structural reform programme to enhance business dynamism and job creation by easing product market regulation and better supporting workers to upskill.

Limiting transfers to failing SOEs where private actors can be attracted, particularly in the electricity and transport sectors, is another key aspect. Improving spending efficiencies while increasing infrastructure investment will also be important.

Furthermore, greater economic dynamism combined with consolidation efforts would help generate higher revenues, leading to larger primary surpluses than in the previous scenario.

This will help to not only stabilise the government’s debt burden but also begin driving it down aggressively, freeing up capital to be used in more productive areas than servicing the state’s debt load.

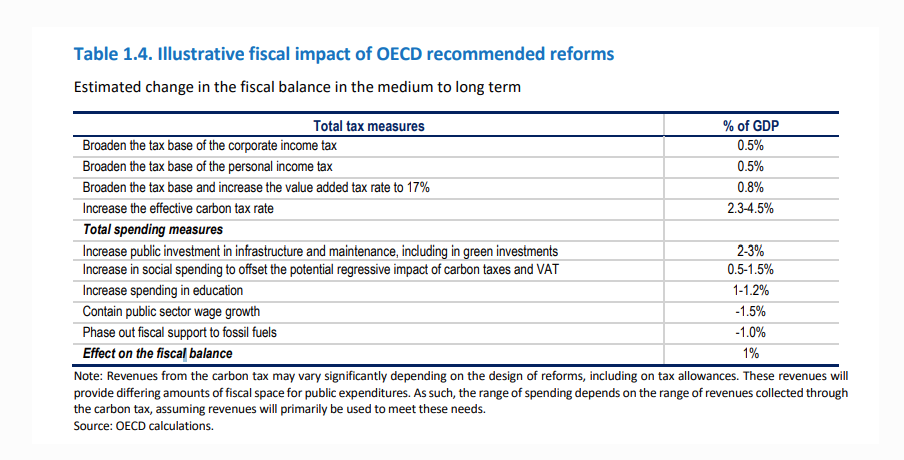

The impact of various reforms outlined by the OECD can be seen in the table below.

Comments