From zero to R410 billion in three decades

PSG Financial Services has grown its assets under management to R410 billion in thirty years, and the company is also reaping the benefits of its investments in insurance and wealth businesses.

Formerly known as PSG Konsult, the company was established in 1996 as a South African financial services provider as part of the PSG Group.

Apart from its historic investment in Capitec and the funding of Curro, PSG Group gradually built its financial services business into a behemoth with over R410 billion in assets in 2025.

While the PSG Group has been delisted from the JSE, PSG Financial Services remains and has outperformed the market since its listing in 2014.

Coronation analyst Zukisa Luswazi explained that this outperformance has been driven by strong execution and consistent investment in key underlying businesses.

Some of these, such as PSG Wealth and Western National, are well-positioned to drive further growth and justify PSG Financial Services’ lofty valuation.

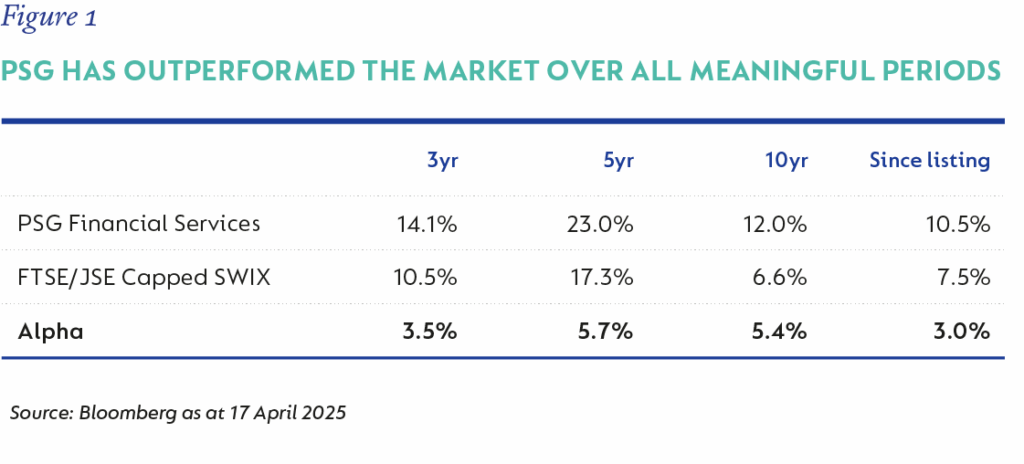

Since its listing, PSG has averaged an annual return of 10.5% compared to the JSE’s 7.5% and has consistently outperformed its fellow asset management peers.

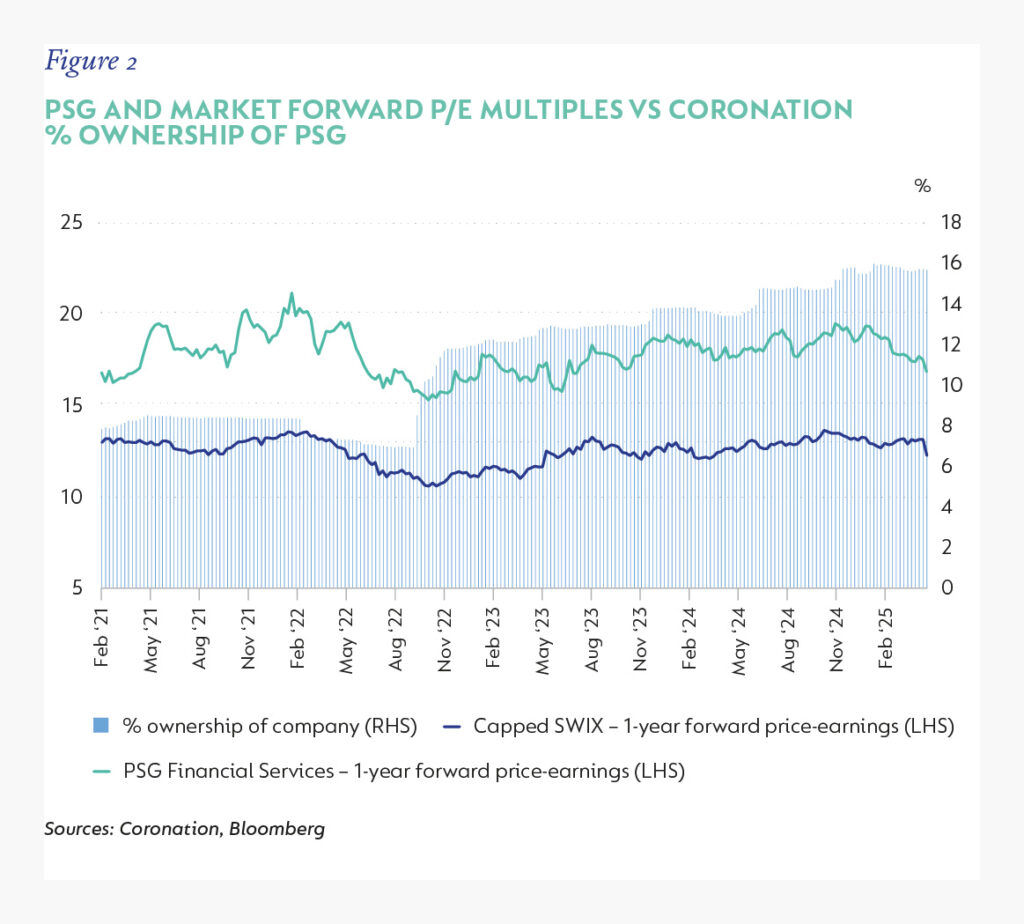

Even in recent years, forward price-earnings multiples looked expensive, trading at a notable premium to the market.

Despite this, Coronation has meaningfully increased its stake in PSG Financial Services over the years due to its conviction that the market has never fully appreciated the size and quality of the business it will become.

Even on what looks like a full rating today, Coronation believes it remains attractive and considers the 16 times forward price-earnings multiple undemanding, given the size and durability of its long-term growth prospects.

Importantly, it is under the stewardship of a strong and experienced management team aligned with shareholders.

PSG Financial Services also operates in a relatively capital-light industry, with high recurring revenue, healthy margins, and strong shareholder returns.

The table and graph below show PSG’s historic outperformance of the JSE and its earnings multiple over time.

The secret sauce

PSG is an advice-led financial services group that operates in wealth management, insurance, and asset management.

Founded almost 30 years ago, it has grown a strong wealth management franchise in PSG Wealth, built well-regarded insurance operations (distribution and underwriting) in PSG Insure, and nurtured a respectable asset manager in PSG Asset Management.

While the business was tremendously successful during this period, Luswazi explained that the company’s rapid growth resulted in it becoming a sprawling enterprise with some inefficient operations.

The current CEO and CFO took over the company in 2013 and began cleaning up, institutionalising, and investing in its businesses.

Crucially, the executives closely aligned their personal interests with those of the shareholders through long-term incentives and notable personal stakes in the company.

This also gives PSG an edge over competitors, as its management is able to think long-term and execute its stated strategy over time.

This is beneficial not only for shareholders but also for the company, with management able to play the long-term game and win.

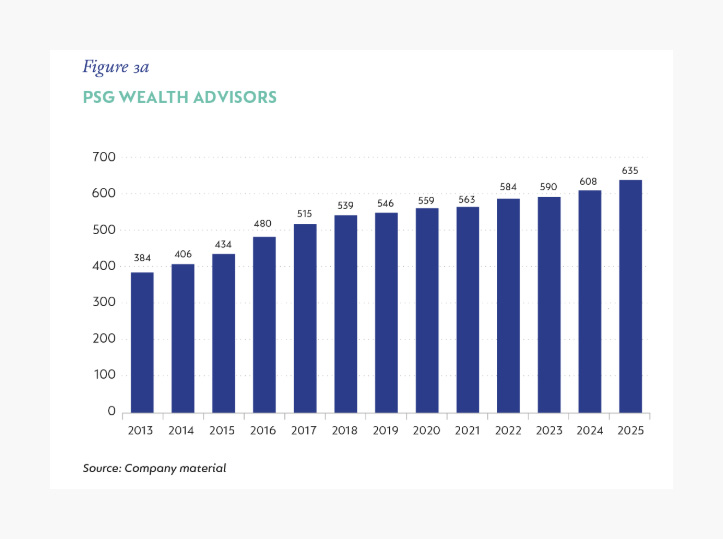

Today, PSG is a high-performing company, and its largest business, PSG Wealth, is extremely well-positioned for superior long-term growth, Luswazi said.

This company generates around 60% of PSG’s current earnings and has the largest independent advisory force in South Africa that is not tied to a bank or life insurer.

It runs a time-tested revenue-sharing business model with its advisors. This respects their autonomy and allows them to build independently run advisory practices within the PSG stable.

In addition, they benefit from the support of a strong centre that takes away the administrative burden of running advisory practices. This frees advisors up to do what they do best – serve clients well and grow their practices.

The business model is attractive to independent financial advisors (IFAs) and bank-tied wealth managers alike. IFAs are attracted because growing regulatory and compliance pressures on financial advisors are compelling them to find a home for their practices.

Wealth managers are driven by the superior economics of being a wealth advisor within PSG compared to being bank-tied.

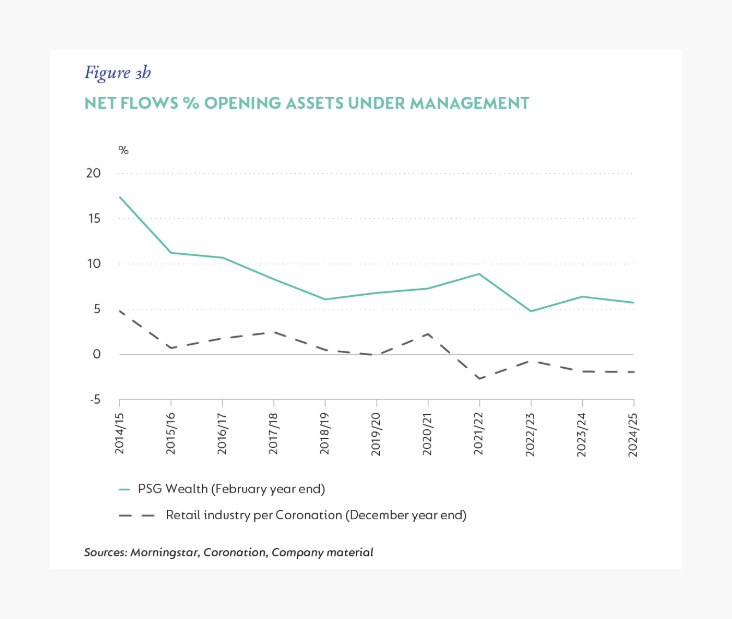

This model has greatly benefited PSG, with it translating into significant growth in its advisory base and greater flows into its asset management business than its peers.

These metrics can be seen in the graph below.

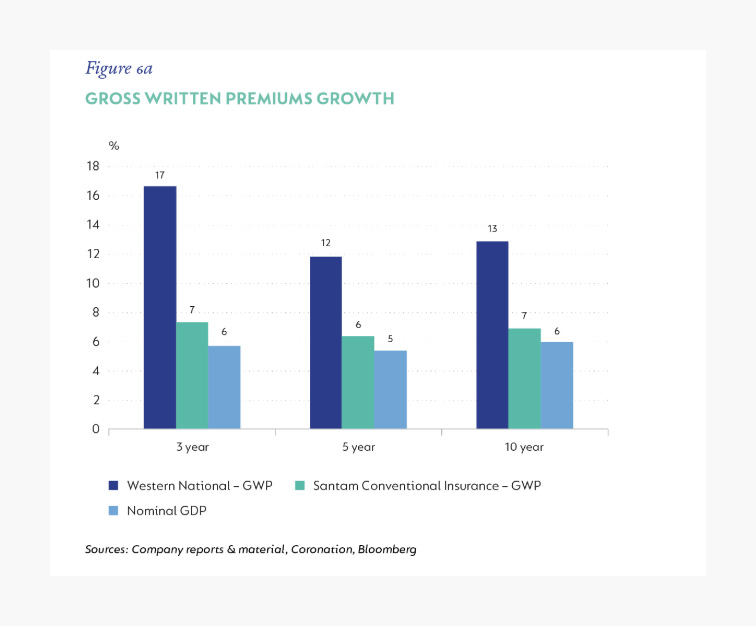

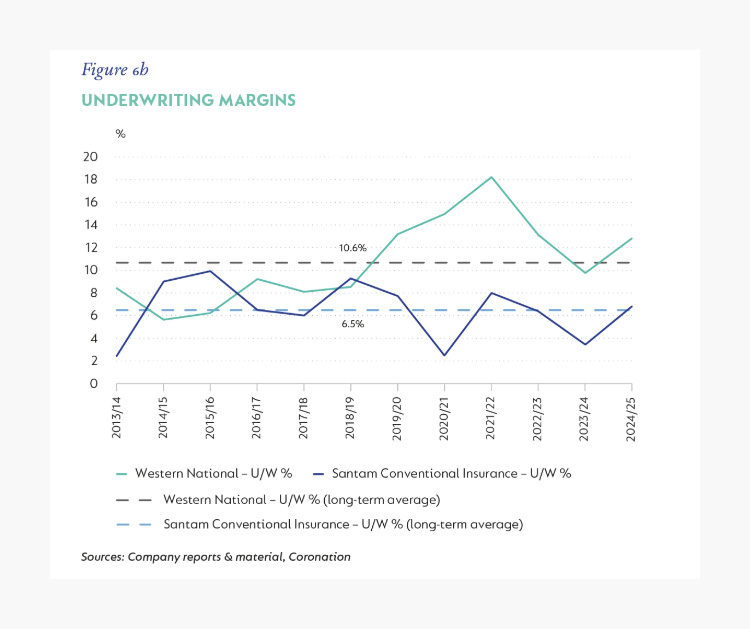

The strong and steady growth of PSG’s asset management business has been coupled with the rapid acceleration of its insurance underwriting business, Western National.

It is a small player in commercial insurance, with a differentiated service model that has earned commendable long-term gross written premium (GWP) growth off a low base.

First launched in Namibia in 2004, the company quickly grew into South Africa in 2007, following strong growth.

Bought by PSG Financial Services in 2012, the company has gone from strength to strength, using PSG’s established adviser network and credibility to drive growth.

Execution over the years has been excellent, with significant reinvestment into the business to improve its quality and deliver sustainable growth.

The company operates through a network of qualified insurance brokers, intermediaries, and carefully selected underwriting managers.

Having a flat management structure and decentralised servicing model enables efficient service and quick decision-making, an exceptional advantage in the highly competitive short-term/non-life insurance market.

Reassuringly, growth has been accompanied by rising underwriting margins, which helps support our view that the quality of underwriting has been good and that market share gains are sustainable.

Going forward, given its low industry share, we expect this business to continue to deliver above-average GWP growth as it continues to scale its winning service model.

The graphs below show how Western National is growing premiums faster than the market (using industry bellwether Santam as proxy) and at healthy, improved margins.

Comments