How much money the South African Reserve Bank makes

The South African Reserve Bank (SARB) is one of the country’s best-run state institutions, consistently running at a surplus and maintaining a strong balance sheet.

The Reserve Bank opened its doors on 30 June 1921, making it the oldest central bank in Africa. Before it was established, commercial banks issued banknotes to the public, which had to be backed by gold.

However, a problem with this system arose when, due to unusual conditions created by the First World War, the price of gold in the UK rose higher than in South Africa.

Therefore, one could profit by converting banknotes into gold in South Africa and selling the gold in London, forcing local banks to buy gold from London and re-import it at a loss.

Commercial banks asked the government to release them from the obligation to convert banknotes into gold on demand to protect their financial viability.

Their pleas led to the Gold Conference of October 1919, which resulted in a recommendation by a Select Committee of Parliament that the government establish a central bank.

Parliament accepted the recommendation, and the SARB issued its first banknotes to the public on 19 April 1922.

South Africa eventually abandoned the gold standard in 1932, when the country opted to link the value of the local currency to the pound sterling.

South Africa introduced the rand on 14 February 1961, three months before the country left the Commonwealth and became a republic.

After the South African Reserve Bank Act of 1989 was signed into law, the SARB accepted a formal mission statement for the first time the following year.

This statement declared that the Reserve Bank aimed to protect the rand’s internal and external value, an objective that was later included in the country’s Constitution.

With the adoption of the Constitution in 1996, the SARB’s independence was also enshrined.

The Constitution gave the SARB a clear mandate – to pursue and maintain price stability for balanced and sustainable economic growth.

In 2000, South Africa became the 13th country to adopt an inflation-targeting monetary policy framework, targeting a consumer inflation band of between 3% and 6%.

The Reserve Bank continues to use this model in fulfilling its mandate of protecting the value of the rand.

South African Reserve Bank revenue

Some of its work to achieve this mandate generates revenue for the SARB, although the organisation is not profit-driven.

This revenue funds the organisation’s operating expenses, and the surplus of the SARB’s earnings is paid to the government. The Reserve Bank generates revenue in several different ways.

In its latest annual report for the 2023/24 financial year, the SARB reported a total revenue of R49.51 billion.

The bulk of this income comes from managing foreign exchange reserves, which generated R16 billion in revenue for the SARB in the 2023/24 financial year.

The organisation also earned R509 million in interest from managing market operations in pursuit of implementing monetary policy.

The SARB and its subsidiaries further generate revenue through settlement commissions, bulk cash service fees, government bank charges, management fees, and licence fees.

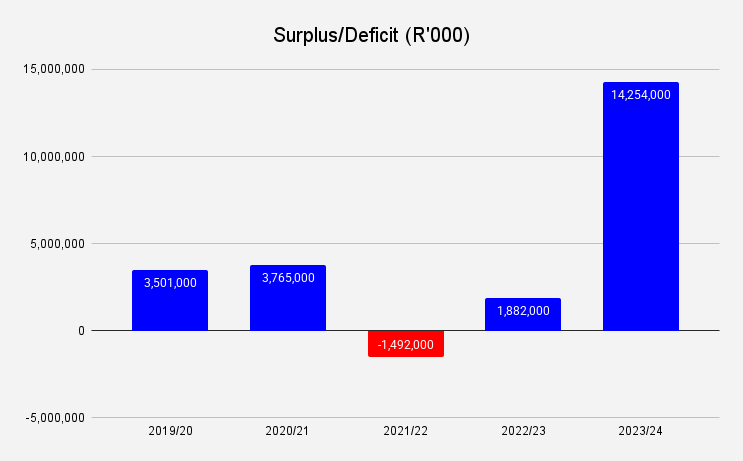

The Reserve Bank has run at a surplus for the past five financial years, excluding 2021/22, when significant movements in the yields in the markets where the SARB invests foreign exchange reserves hurt its investment income.

In that year, the SARB’s net investment income, derived mainly from foreign investments and accommodation to banks, decreased by R5.5 billion to R2.8 billion.

At the same time, its operating costs increased to R7.1 billion, resulting in a loss after tax of R2 billion for the year that ended on 31 March 2022. The SARB reported a deficit of R1.49 billion for that year.

However, excluding this year, the SARB has consistently made a surplus.

Its latest results for 2023/24 showed the Reserve Bank made a surplus of R14.25 billion, up significantly from the prior year’s R1.88 billion, primarily due to a substantial increase in net investment income.

In addition to its strong revenue generation, the SARB’s balance sheet has also been healthy over the past few years.

The Reserve Bank has reported positive net assets for at least the past five financial years, starting in 2019/20.

The organisation has also achieved clean audits for every one of those years – a rare sight for a state entity.

The Reserve Bank’s impressive financial performance can be seen in the graphs below.

SARB shareholders

Many South Africans don’t know that the SARB has had shareholders since its establishment. Today, the SARB has just over 800 private shareholders.

These shareholders have no rights or involvement in determining monetary policy, financial stability policy or regulation and supervision of the financial sector.

Their rights are limited to considering the SARB’s annual financial statements, electing seven of the Reserve Bank’s non-executive directors, appointing external auditors, and approving their remuneration.

The SARB’s shares are traded on an over-the-counter share transfer facility (OTCSTF) market coordinated within the bank.

Shares in the SARB are priced in a tiered model, whereby buying fewer shares costs more per share than buying a higher number of shares. This can be seen in the table below.

Only the shareholders who reside in South Africa are entitled to vote at the bank’s annual general meeting (AGM), and they are allowed one vote for every 200 shares held.

There is no limitation on shareholding, except for the provision of the South African Reserve Bank Act that no shareholder shall hold, or hold in aggregate with his, her or their associates, more than 10,000 of the total number of 2 million issued shares.

Renowned economist Dawie Roodt is one of the SARB’s 800 shareholders, having bought shares in the bank when it was still listed on the JSE.

Roodt told Daily Investor that he owns 200 shares in the Reserve Bank, the minimum needed for voting rights.

He said there are little to no tangible benefits to being a SARB shareholder, but also very few requirements.

Shareholders may attend the SARB’s AGM, and some have voting rights if they own enough shares. Dividends are also not very attractive, with Roodt saying he only received around R8 in dividends last year.

“You go to the annual general meeting, you can vote for half of the directors, you can get certain information which is basically public knowledge already, like certain documents about statistics and so on about economics,” Roodt explained.

“And that’s the reason why I became a shareholder to start off with. But apart from that, not really that significant benefits.”

“The dividends that I receive – it’s really not worth the investment. I guess it’s a bit prestigious to say that I’m a shareholder of the central bank, but apart from that, I can’t really think of any specific benefits.”

Comments