Reserve Bank Governor Lesetja Kganyago’s interest rate headache

Reserve Bank Governor Lesetja Kganyago finds himself between a rock and a hard place ahead of the Monetary Policy Committee’s (MPC) next meeting in May.

The inflation risks stemming from the Middle East war have led many experts to pencil in an interest rate hike, yet doing so could harm South Africa’s still-fragile economic recovery and dampen growth.

PPS Investments’ head of portfolio management and analytics, Mark Phillips, explained that South Africa’s CPI inflation rate is expected to rise in the coming months.

This is despite a subdued inflation print in March, which saw CPI rise modestly to 3.1% compared to February’s 3%.

Phillips explained that, although still modest, this increase was mainly due to higher housing, utility, and insurance costs.

However, with fuel prices now likely to climb further in April due to ongoing geopolitical tensions stemming from the US/Israel-Iran war, inflation may continue rising.

Phillips said that the recent escalation of conflict in Iran has intensified concerns about inflation, especially through its impact on oil prices.

However, he said these higher oil prices may also prompt officials to lower growth forecasts due to their negative impact on both global economic growth and local spending.

Dampened local spending could, in turn, help ease inflation if overall demand decreases, he explained.

This puts the Reserve Bank’s MPC in a difficult position, as it may need to act in the face of rising inflation, yet does not want to risk harming economic growth.

Phillips pointed out that Kganyago previously warned that markets might be underestimating how long refinery disruptions could last and how much they could constrain oil supplies.

“He also stressed that any reduction in fuel levies meant to cushion petrol and diesel price surges should only be temporary,” Phillips said.

“Governor Kganyago emphasised that policy actions should focus on ensuring that the current inflation shock is temporary, not lasting.”

“He also remarked that central banks, which previously delayed addressing inflation shocks, ultimately had to implement more forceful measures.”

While this stance and the MPC’s typically cautious approach to monetary policy suggest a high likelihood of an interest rate hike in the coming months, this may not be the best decision for South Africa.

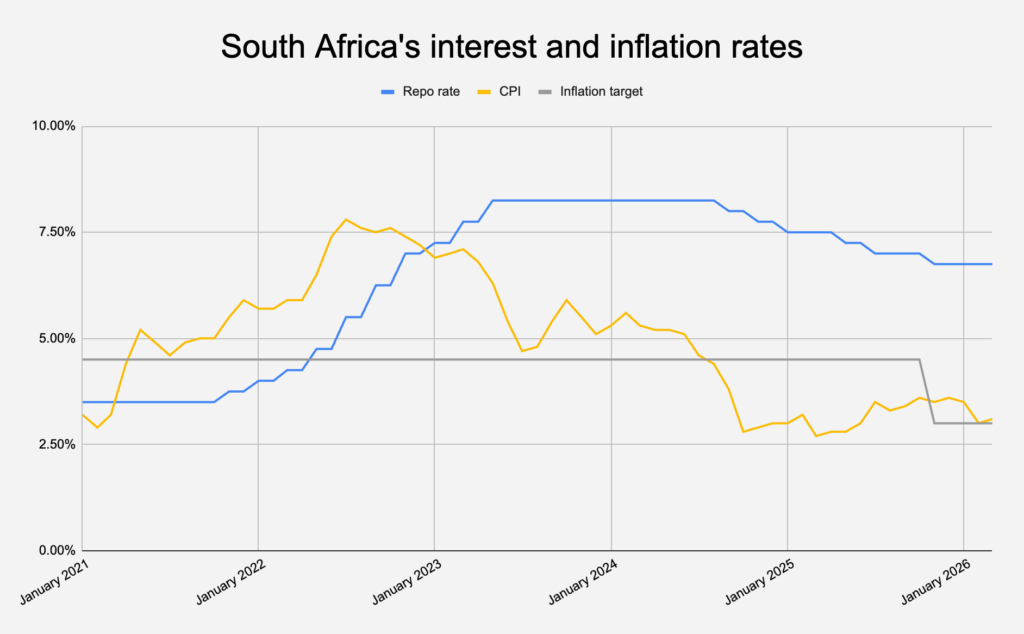

The graph below shows the trend in South Africa’s inflation and interest rates from January 2021 to March 2026.

Wait-and-see

NWU Business School economist Professor Raymond Parsons explained that adjusting to external economic shocks is never painless or easy.

He said South Africa will be lucky if it escapes the current shock with a minor setback to growth and a temporary bout of inflation in 2026.

However, he said that while there are clear upside risks to the inflation outlook in South Africa, the country’s recently lowered inflation target and ongoing fiscal consolidation have created resilience.

These factors have reduced the country’s risk premium, and South Africa’s inflationary expectations were also previously at the lowest level in years.

“South Africa has a few more economic buffers at its disposal now than it had a couple of years ago,” Parsons said.

Despite these buffers, he explained that highly elevated uncertainty has become the dominant feature in all economic narratives and decision-making, both globally and domestically.

“On monetary policy, many central bankers, while becoming cautious about the likely upside inflation risks, have remained wary about suddenly raising interest rates, lest it unnecessarily damages economic growth,” Parsons explained.

He used the example of International Monetary Fund managing director Kristalina Georgieva, who urged central banks to be vigilant without rushing interest rate changes.

Georgieva essentially advocated for a “wait-and-see” approach, encouraging central banks to tailor their responses to incoming data.

“Much depends on how long the conflict still lasts, where the global oil price eventually settles, and what the likely ‘pass through’ costs are in different national economies,” Parsons explained.

Therefore, based on the evidence currently available, South Africa’s Reserve Bank may not need to rush to judgment on whether interest rates should already be raised at its May meeting.

“Monetary policy is still somewhat in restrictive territory, and South Africa has a vulnerable economic recovery to nurture,” he said.

“The SARB remains data-driven and therefore needs to assess whether the ‘second-round effects’ that central bankers always fear are indeed emerging in the economy by the time the MPC meets.”

If these effects do emerge, Parsons said the MPC will naturally need to act in accordance with its chief mandate and maintain its credibility.

However, he pointed out that the Reserve Bank already enjoys strong credibility and can therefore afford to adopt a ‘wait-and-see’ stance for the time being.

This, Parsons said, will also allow the central bank to remain agile as it navigates an abnormal and highly uncertain world.

Comments