South Africa dodging tax hikes

South African taxpayers have more than likely avoided the worst-case scenario of tax increases in the 2026 Budget thanks to the government’s lower borrowing costs.

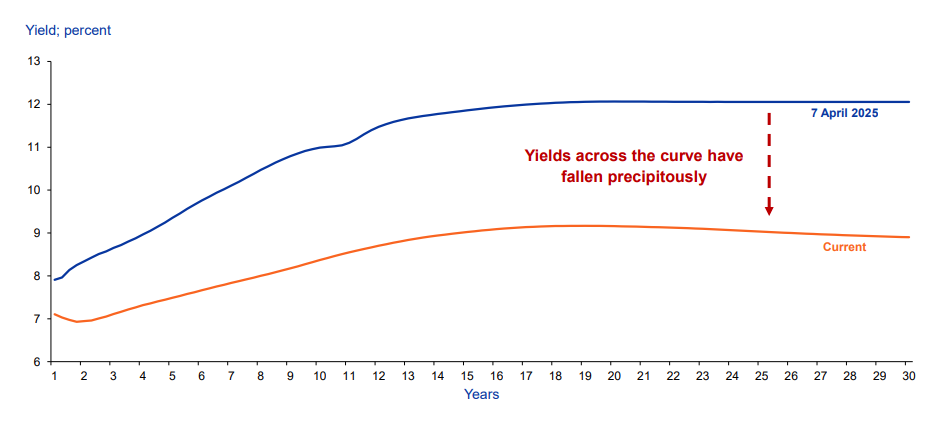

This has been a result of the strong performance of South Africa’s bond market amid expectations of improved government finances and a tax windfall from mining profits.

As investors, both local and foreign, have piled into South African government debt, the yield to attract investment in these assets has fallen.

Crucially, the yield has fallen steeply across the yield curve from short-term borrowing to long-term debt, significantly reducing the government’s debt-servicing costs.

This should eliminate the need for the government to raise taxes in the 2026 Budget, with it warning in 2025 that it may need around R20 billion in additional revenue to fund its spending commitments.

Standard Bank chief economist Goolam Ballim explained how the strong performance of the South African bond market has resulted in this potential tax relief.

Speaking at the bank’s Economy 2026 event, Ballim explained that despite consumers and businesses, except large corporates, participating in the bond market, it still has a significant impact on the entire country.

“Developments in the bond market are worth noting. Consumers don’t participate in the bond market per se. They do not borrow in this arena,” Ballim explained.

“This is mostly government and large corporates. They borrow 5-year, 10-year, 15-year, and even 30-year money as they describe it in the financial market.”

As this is so far removed from the ordinary individual, the impact of reduced yields across those time frames is often not understood.

Ballim explained that the bond market is often seen as purely financial, with its benefits only accruing to select individuals and companies. However, this is not the case.

“It is also a real economy story. This is a real economy story because now the government is borrowing at a measurably cheaper rate, lowering its debt-servicing costs,” Ballim said.

“When I say it is a real economy story, the revenue flow to the authorities because of the relatively healthy economy and lower debt-servicing costs will turn out to be better than expected.”

Ballim said Standard Bank’s research indicates that revenues in the current fiscal year will overrun by around R15 billion.

While small, this is significant because the National Treasury suggested there would be a need for a tax increase from February 2026 to plug a fiscal hole left by the failed implementation of a VAT hike in the 2025 Budget.

“Because of the declines in the interest rate paid on debt, it is entirely plausible that, in fact, the extent of tax hikes or raising taxes at all may not come to pass as a function of lower funding costs,” Ballim said.

Investment boost

A further benefit of declining interest rates on debt sold in the bond market is that they are likely to result in increased investment in the local economy.

Ballim explained that, as corporates can raise debt more cheaply alongside the government, the hurdle to investment in South Africa is reduced.

In other words, the rate of return required to make an investment in South Africa profitable is significantly lower now than it was at the beginning of 2025.

This is true for the government and, more importantly, for businesses, with it likely to result in increased fixed investment, which is vital for sustained economic growth.

“Companies are now also funding their growth at much lower levels in terms of longer-term borrowing, helping to reduce the hurdle rate for investment and generally increasing the propensity for investment,” Ballim said.

Lower interest rates, more broadly, are also likely to result in increased investment as it becomes less attractive to hold cash in the bank, with the return decreasing as rates come down.

While this is not a significant hurdle to investment at the moment, corporates are sitting on R1.8 trillion in cash in the bank, making any reduction helpful.

Stanlib chief economist Kevin Lings has explained that elevated interest rates are not the main hurdle to investment from corporates in South Africa.

Rather, it is due to low business confidence in the economy amid declining service delivery, policy uncertainty, and flat economic growth.

Lings has pointed out that this does not mean that companies are not investing in South Africa. Rather, they have not been investing in growing their operations.

Companies in South Africa have been engaging in what is termed ‘subsistence investment’ to keep their doors open and not necessarily grow.

This investment is characterised by capital going towards alternative energy sources, backup water systems, and increased security.

These kinds of investments do not directly result in the company making more money or employing more people – they simply keep it operating.

“The current investment level is mainly maintenance capex and kind of treading water, with companies waiting for a better environment,” Lings said.

“Instead of deploying capital into growth or hiring, corporates are parking it in money market funds or call accounts.”

Lings has explained that this is largely a function of declining confidence from corporates in the South African economy.

“So generally it is a confidence thing. Confidence is a leading indicator of increased investment. Without it, funds do not flow into the local economy,” Lings said.

“We find around the world that in order to inspire more private sector investment, you must first get the confidence.”

“What we really need in South Africa is what we call expansion capex, and that tends to be a function of confidence.”

Comments