South African Reserve Bank dodges a bullet

A stronger rand and several external factors have made the Reserve Bank’s job of moving South Africa towards a lower inflation target significantly more achievable than it would have been under normal circumstances.

While moving to a lower target typically comes with severe short-term risks to the economy, the stronger rand and external factors have taken a lot of pressure off the Reserve Bank in trying to chase the new target.

The country’s move to a new, lower inflation target is set to hold immense benefits for the economy in the long term, including less volatile inflation, improved purchasing power and lower government borrowing costs.

Momentum Investments economists Sanisha Packirisamy and Tshiamo Masike explained that the firmer rand has rendered South Africa’s move towards this lower target far more tenable.

While South Africa’s pivot to the lower target has been promoted with the notable benefits it would bring to the economy, it was done knowing that there were some risks involved.

Considered a double-edged sword, moving to a lower inflation target carries short-term risks while promising long-term gains.

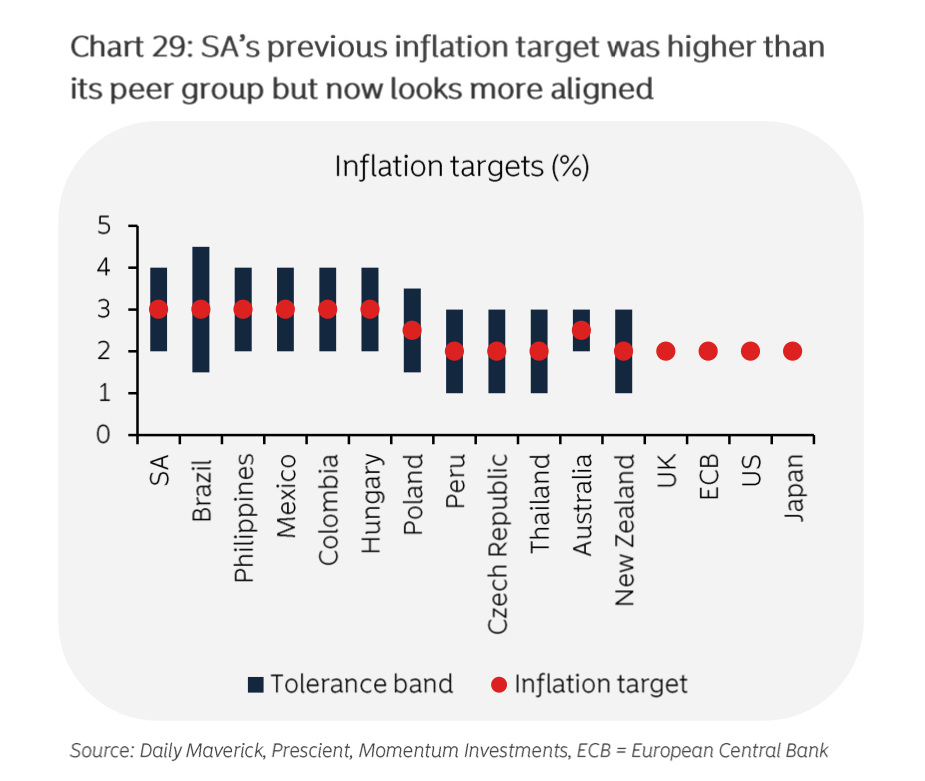

“Under normal circumstances, shifting to a stricter 3% inflation target would risk rattling markets and prompting doubts about policy resolve,” they explained.

Typically, the transition towards a lower target may negatively impact a country’s economic growth and increase pressure on households with debt.

This is because a country’s central bank may need to hike or keep interest rates higher for longer to reach and maintain inflation at the lower target.

In South Africa’s case, the Reserve Bank’s target was both lowered and narrowed, from a range of 3% to 6% to the new target of 3%, with a one percentage point tolerance band.

While the central bank has been a strong proponent of lowering the target for years, the National Treasury dug its heels in on the shift, citing concerns about the potential negative impact of making the switch.

Weighing the benefits and risks

In South Africa, the National Treasury sets the target, while the Reserve Bank chases it, meaning the Treasury’s hesitation saw discussions about lowering the target drag on for months.

Ultimately, Finance Minister Enoch Godongwana gave his nod of approval to lower the target in his Medium-Term Budget Policy Statement (MTBPS) in November 2025.

In announcing the new target, Godongwana noted the risks involved, warning that lower inflation will initially slow nominal GDP and revenue growth, given that tax receipts are linked to nominal GDP.

“This will reduce fiscal space, while the real value of public debt will decline more slowly,” he said.

Regardless, he said that, after careful consideration, the government concluded that the benefits of a lower inflation target outweigh the costs.

However, Packirisamy and Masike said, while there are normally notable risks involved when moving to a lower target, this was not the case for South Africa.

“This time, however, the external environment did much of the heavy lifting,” they said.

“A stronger rand, supported by a weaker dollar, firm precious-metal prices and relatively soft global oil prices, helped contain imported cost pressures.”

In 2025, the rand rose 2.5% against the US dollar on average, while the greenback weakened by 3.3%.

The rand’s strong performance was also driven by a commodity rally, particularly for precious metals like gold and platinum, which benefited the value of South Africa’s exports and, consequently, the local currency.

Packirisamy and Masike explained that the confluence of these factors created an unexpectedly supportive setting for the Reserve Bank’s move to a lower target.

This setting made the revised target appear more achievable, rather than an overreach, with the benefits set to come from the lower target clearly in sight.

In time, the economists said a lower inflation target should allow for less volatile inflation, improved purchasing power, increased housing affordability, a less stringent funding environment for corporates, and lower government borrowing costs.

Comments