End of an era of dominance for the US dollar

The US dollar’s expected rally in 2025 on the back of President Donald Trump’s America First policies did not materialise, with the greenback having one of its worst years on record.

While the US dollar has suffered periods of sharp weakness in the past, those are typically driven by short-term cyclical factors such as a commodity boom.

However, this time around, the dollar’s weakness appears to have been driven by large-scale currency hedging, as investors have not sold out of US assets in meaningful amounts.

This indicates that the dollar’s weakness is potentially more fundamental, with 2025 being the beginning of a decline for the greenback that will play out over decades.

Symmetry chief investment strategist Izak Odendaal explained that Trump’s policies were largely expected to result in higher interest rates in the US and thus, a stronger dollar.

The policies of reshoring manufacturing, elevated tariffs, and renewed tax cuts resulted in economists predicting elevated inflation in the world’s largest economy.

While some of these policies have only come into effect as of 1 January 2026, inflation has not only moderated in the US but also declined towards the end of 2025, contributing to the Federal Reserve cutting interest rates throughout 2025.

This has been coupled with increased investor uncertainty regarding the financial health of the United States government, with its debt continuing to soar.

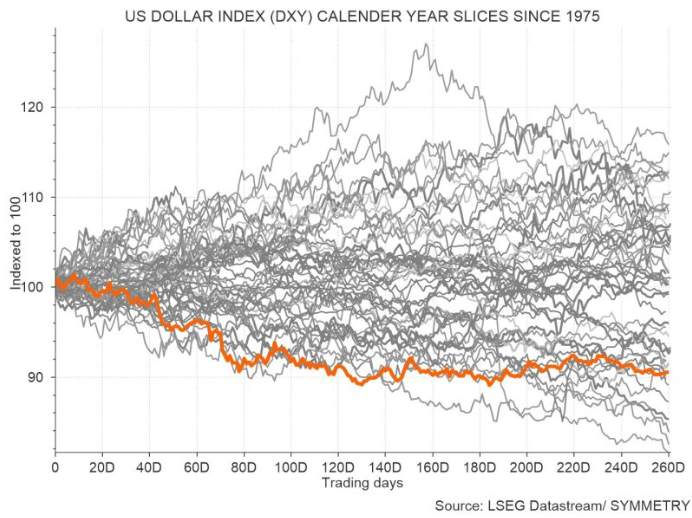

As a result, 2025 was one of the worst years for the trade-weighted dollar index in the last five decades, Odendaal said.

This was not because global investors sold out of US assets, with significant capital still being poured into American equities amid optimism regarding artificial intelligence.

Rather, Odendaal explained, it appears that for the first time in 15 years, large-scale currency hedging drove the dollar lower.

This indicates a shift in investors’ perception of the security of capital in the United States, with many thinking that inflation will be higher for longer in the future to inflate away the country’s debt.

Odendaal said interest rate differentials will probably play a bigger role in the future, with investors hunting for yield and security.

Most major central banks are set to hold their rates for now, but the Federal Reserve is in a tricky position in 2026, with it set to get new leadership.

A dovish Fed could see further declines, especially as the dollar remains strong on a historical basis despite the recent declines.

In contrast, if the US growth outlook stabilises, and the Fed is comfortable with rates where they are, the dollar could bounce after a tough year.

Dollar decline

Odendaal has been clear in saying that the US dollar’s downward trend will not occur in a straight line, with the currency likely to experience some periods of strength.

However, the overall trend for the dollar appears to be negative for the time being, with the factors underpinning its strength being eroded.

This means the US dollar’s extended bull run since the end of the Global Financial Crisis appears to be coming to an end.

While this era appears to be coming to an end, it does not mean the US dollar will lose its privileged status, as it is likely to remain the dominant global currency.

The US dollar has been the world’s primary reserve currency for decades and is still the most-used currency in financial transactions and flows across borders by some distance.

It makes up over half of the global foreign exchange reserves, with other currencies and assets such as gold making up the rest.

However, this share has steadily fallen over the years, with recent weakness in the dollar and developments in the United States leading some to argue the world should reduce its reliance on the greenback, Investec’s Paul McKeaveney said.

These concerns could mark the end of an 18-year bull run for the dollar, with the currency typically moving in long, multi-year cycles of strength and weakness.

Most notably, the dollar has been in a prolonged bull market since 2007, one of the longest on record, as American assets soaked up global liquidity.

McKeaveney said there are various signs that this cycle could be turning, including –

- A deteriorating US growth outlook: There have recently been downward revisions to US GDP forecasts and emerging signs of a slowdown.

- Fiscal and debt concerns: The US fiscal outlook has worsened, and high government deficits and rising interest costs are undermining confidence in the dollar. Of greatest concern is perhaps the recently passed One Big Beautiful Bill Act, which is set to increase the US debt-to-GDP ratio to about 107% by 2027.

- Policy unpredictability: Uncertainty in US policy and geopolitical moves can erode trust. Policies such as inconsistent tax, tariff or regulatory changes make the US a relatively less attractive place to invest at the margin, leading investors to explore other currencies.

- A changing world order: We are seeing a shift to a multipolar world, in which countries like China look to challenge US hegemony in many spheres, including payment systems and the use of the dollar as the world’s reserve currency.

These factors have led some investors, most notably central banks, to consider alternatives to the dollar, including other currencies, but particularly gold.

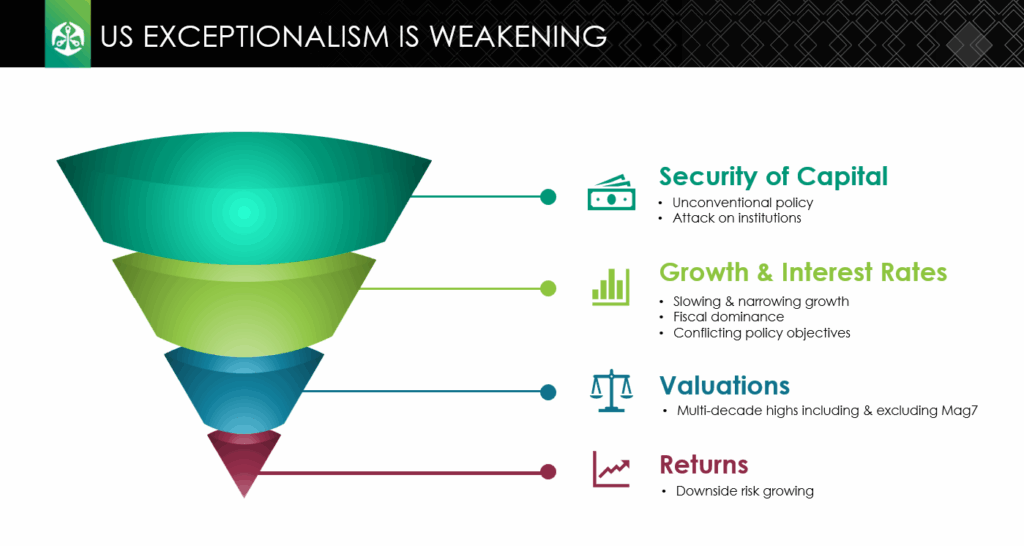

The key factors underpinning US exceptionalism can be seen in the graphic below from Old Mutual’s Zain Wilson, with some of the issues eroding these factors listed alongside.

Comments