South Africa on the way to serious trouble

South Africa faces another giant budget deficit for the 2025/26 financial year, with revenue collection lagging in the fiscal year to date.

This risks the state having to borrow more than expected to cover its expenditure, spelling trouble for South African bond yields.

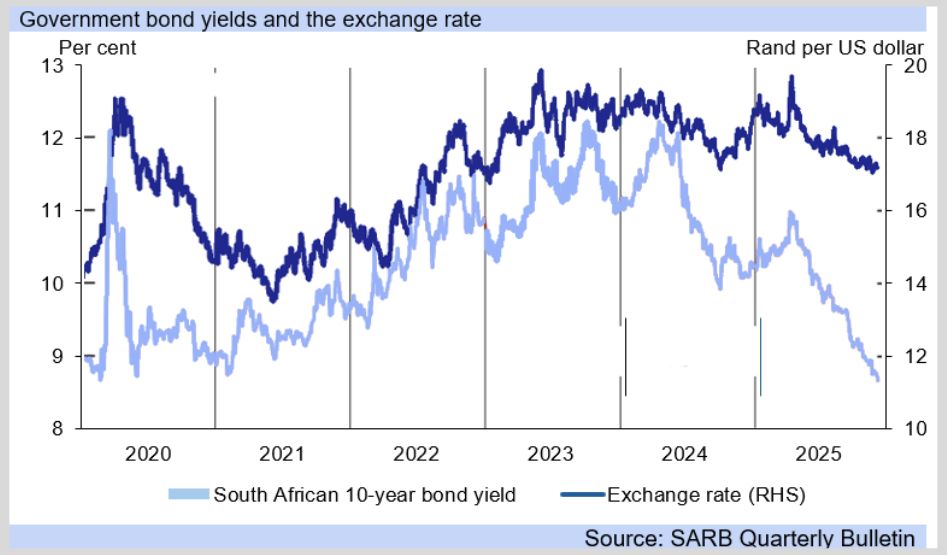

Investec chief economist Annabel Bishop recently pointed out that South Africa’s benchmark bond yield reached a seven-year low.

2025 proved to be one of the best years for South African bond yields in the past decade, with the country’s benchmark bond yield strengthening by 186 basis points.

This is far higher than the 82 basis points recorded in 2024, and a notable improvement from 2023 and 2022, when the local benchmark bond yield weakened by 20 basis points and 120 basis points, respectively.

South Africa’s benchmark bond yield rose as high as 12.23% in the lead-up to the 2024 national elections, driven by political risk associated with the potential outcome of the vote.

Ultimately, the 2024 elections yielded a market-friendly outcome, resulting in the formation of the Government of National Unity (GNU).

Bishop explained that the GNU’s focus on fiscal consolidation, rather than fiscal deterioration as seen in years past, resulted in multiple budgets in the 2025/26 fiscal year aimed at limiting expenditure.

Now, she said South Africa’s 2026/27 Budget, which is likely to be presented on 25 February 2026, will be key for the domestic bond market.

Bishop explained that the National Treasury had been keen to hike taxes, especially the value-added tax rate, in 2025, “and so much depends on expenditure containment”.

She pointed out that, currently, for the first eight months of the 2025/26 year, expenditure is running at 62.7% of the Budget, compared to 64.2% of the Budget a year ago.

The lag in expenditure in 2025 compared to 2024 can be attributed to the delay the Treasury experienced in passing the Budget last year.

However, revenue collection in 2025/26 to date is closer, at 59.7% of the Budget, versus 64.2% a year ago.

“With the deficit at R281.4 billion, it is already 80% of budget, but at only two-thirds of the year, risking pressure for further borrowings and so pressure on yields,” Bishop said.

South Africa’s budget headache

One of the government’s main motivations for reducing its deficit and achieving, at the very least, a primary budget surplus is to reduce the state’s massive debt burden.

Over the past few years, the government’s debt burden has ballooned to R5.3 trillion and has made debt service costs one of the state’s biggest spending items.

The National Treasury has acknowledged the unsustainable nature of the state’s debt burden and growing debt service costs, with plans to stabilise the debt burden in the 2025/26 fiscal year.

The Treasury has managed to achieve primary budget surpluses – i.e. excluding debt service costs – in the past two financial years, and plans to do the same in the 2025/26 fiscal year.

This should allow the state to stabilise its debt burden and free up spending for more productive line items in the Budget, including fixed investment.

However, to keep this momentum going, the state will need to ensure its spending and revenue are better aligned than they have been over the past decade.

South Africa’s government has run consecutive budget deficits for the past 15 years, which saw the state’s debt burden rise from around R627 billion in 2008 to over R5 trillion in 2025.

South Africa’s lacklustre economic growth has also played a significant role, as the economy has not grown fast enough to keep pace with government spending and the rise in state debt over the past few decades.

At the same time, ballooning debt service costs have rendered the government unable to sufficiently allocate state resources towards productive spending items like infrastructure, education and healthcare, which would have benefitted the economy in the long term.

Many experts hope that the tide has turned in this regard, with the National Treasury, under Finance Minister Enoch Godongwana, seemingly committed to fiscal consolidation.

Comments