One decision saving South Africa R900 billion

The decision to lower South Africa’s inflation target to 3% is set to save the government over R900 billion in debt-servicing costs over the next decade.

This is expected to be coupled with faster economic growth, further easing the government’s debt burden, which has surged to over 77% of GDP.

A lower inflation target is likely to result in structurally lower inflation, which will translate into lower interest rates, slashing debt-servicing costs and boosting economic growth.

This is feedback from Reserve Bank Governor Lesetja Kganyago, who recently outlined the benefits of a lower inflation target.

“The timing is absolutely correct, because inflation was already hovering around 3%. It made sense then to keep inflation where it is and lock in the gains,” Kganyago told Newzroom Afrika.

While the timing was correct and the move to a lower target appears to occur quickly, Kganyago said discussions between the National Treasury and the Reserve Bank about a lower target already began in 2021.

This enabled both the Reserve Bank and the National Treasury to conduct various analyses to determine whether the benefits of moving to a lower target would outweigh the costs.

“Let’s start with the fiscus. Our calculations show that the fiscus could potentially save about R900 billion over a period of ten years from moving to a lower inflation target,” Kganyago said.

“R900 billion is a significant amount of money saved on interest payments, which can then be used to invest in more productive areas of the budget.”

Economists typically refer to money spent on debt-servicing costs as “dead money”, as it provides no benefit to the economy or citizens.

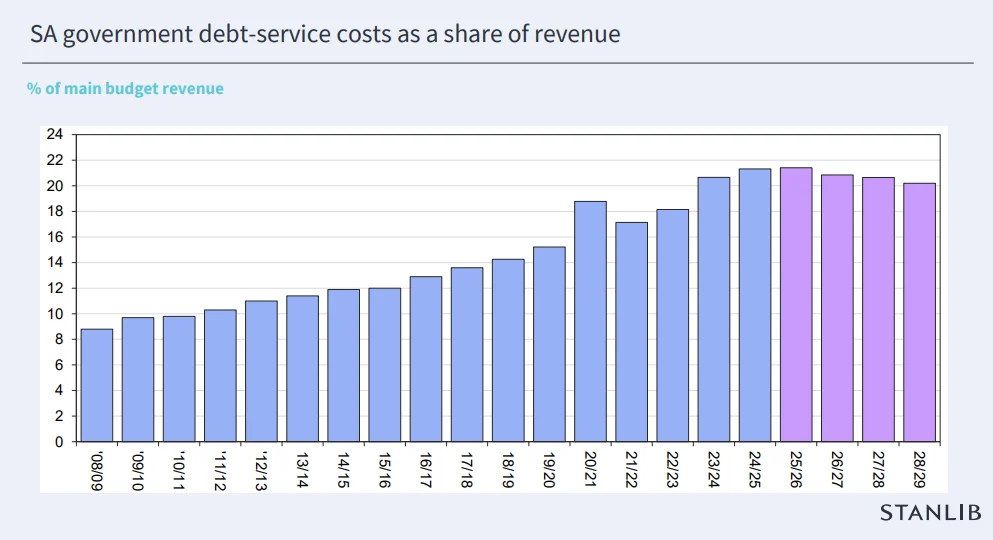

In the case of South Africa, the government pays over R1 billion a day to service its debt, which is more than it spends on education or healthcare.

Currently, around 22% of all taxes collected in South Africa is used to pay interest on the government’s debt, crowding out expenditure in other areas of the economy.

This impacts economic growth and can create a negative spiral when debt-servicing costs compound at a faster rate than the economy.

Households benefit too

The same benefit of lower inflation and interest rates plays out on household balance sheets, which can boost economic growth in South Africa.

As with the government, debt-servicing costs on all types of debt will come down as interest rates do, reducing repayments on home loans, car loans, and other types of borrowing.

“Households will also have massive benefits, because a lower inflation environment means there will be a lower interest rate environment,” Kganyago said.

“A lower interest rate environment feeds itself into households’ balance sheets, individual spending, and the decision-making of individuals.”

Lower interest rates will also mean a reduced return on savings in South Africa, which is also expected to boost the economy.

A lower interest rate on savings accounts is expected to push companies, in particular, to move cash out of savings accounts and into the economy.

South African corporates are sitting on over R1.8 trillion in cash deposits, which is effectively waiting on the sidelines for investable opportunities.

While interest rates are not the main reason for this cash pile, low business confidence is, a lower rate of return on this cash will lower the hurdle for these companies to invest in expanding their operations.

Another significant benefit for households is that a lower inflation target will maintain their buying power for longer, easing financial pressure.

“At 6% inflation, prices will double every 12 years. If you target 3%, prices only double every 24 years, greatly improving the purchasing power of individuals over time,” Kganyago said.

“Lower inflation means that the South African Reserve Bank has more room to lower its policy rate, making the cost of borrowing lower. Lower inflation leads to lower interest rates.”

This significantly loosens financial conditions in South Africa, making it cheaper to borrow money while also reducing current debt repayments.

This frees up spending from businesses, households, and the government, significantly boosting economic growth in South Africa.

“Remember that the mandate of the South African Reserve Bank is to protect the buying power of the income of South Africans,” Kganyago explained.

“What you have seen is that with the decline in inflation, disposable income is released and, as a result, people have more buying power.”

This is a result of a combination of prices rising at a slower rate and wages rising at a faster rate than those prices, increasing buying power.

“The maintenance of inflation at lower levels provides the Reserve Bank with room to relax its monetary policy, lowering borrowing costs and that has released income for South Africans,” Kganyago said.

Comments