Good news about interest rate cuts in South Africa

The Reserve Bank is likely to continue cutting interest rates through 2026 as inflation peaks early next year and begins to decline towards its 3% target.

Coupled with declining inflation expectations and looming cuts from the US Federal Reserve, the Reserve Bank is set to have a relatively straightforward year.

This continues the bank’s streak of relatively easy decisions in comparison to some of the headwinds faced by its peers in other countries, chief investment strategist at Symmetry, Izak Odendaal, said.

Odendaal explained that this is despite inflation being expected to rise further in the coming months, albeit at a slow pace.

There are no major risks to the inflation picture, with the rand holding its own against the dollar, geopolitical tensions easing, and improving state finances.

These developments, particularly a stronger and more stable rand, resulted in the Reserve Bank’s Monetary Policy Committee (MPC) cutting interest rates by 25 basis points at its last meeting.

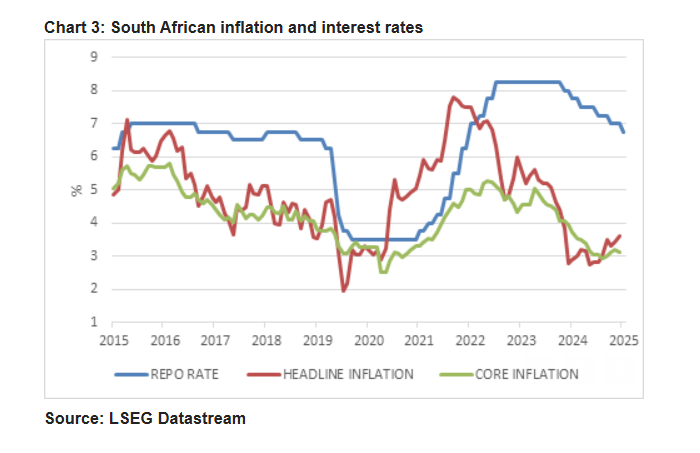

This took the repo rate to 6.75% in South Africa, which Odendaal described as an early Christmas gift for households and businesses in South Africa.

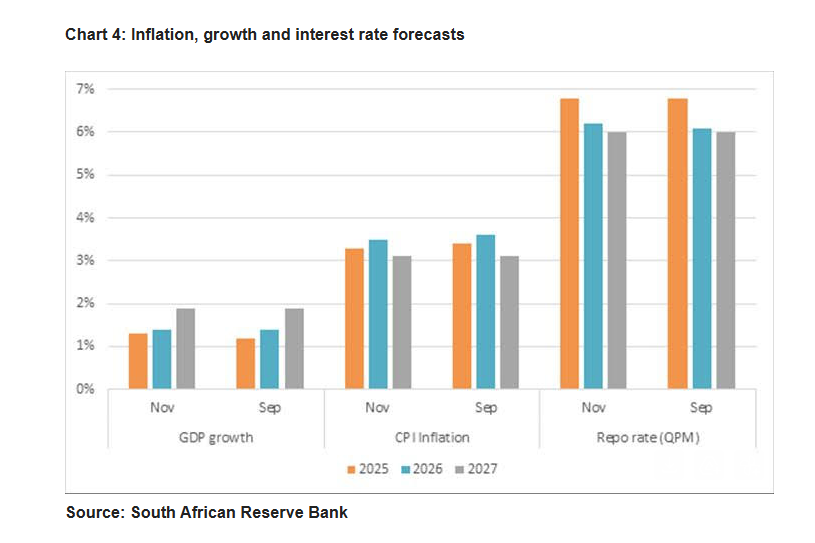

The good news is set to keep on coming as this is unlikely to be the last interest rate cut, with the MPC’s quarterly projection model indicating further rate cuts.

Its quarterly projection model is a forecast of where the repo rate should be given all the other economic assumptions made by the Reserve Bank. The QPM points to rates declining to 6% by 2027.

The Reserve Bank Bank always reiterates that the QPM is merely a guide, and that decisions are taken on a meeting-by-meeting basis, but it does indicate what a reasonable path for interest rates looks like.

The Reserve Bank expects inflation to peak at 3.8% in the second quarter of next year, before falling to around 3%, with an average rate of 3.5% in 2026 and 3.1% in 2027. If inflation behaves as expected, interest rates should continue falling.

Uncertainty remains

The MPC will proceed gradually, given the uncertain environment, with US policy shifts expected to continue throughout the Trump presidency.

There are also local factors at play, such as the ANC’s increasingly tense succession race that is playing out in public and behind closed doors.

Although this seems pressing to South Africans, in the grander scheme of global financial markets, the events in the country seem relatively tame.

In contrast to the Fed, the Reserve Bank had an excellent year, with its decisions being more straightforward than many of its peers.

A major positive is that inflation remains low, coming in at 3.6% year-on-year, a touch lower than expected. In fact, October’s inflation rate sits in the bottom 10% of all monthly inflation readings since 1970.

Though inflation has ticked up in recent months, it should start drifting lower again with few obvious risks currently visible.

Inflation expectations as surveyed by the Bureau for Economic Research also declined this year, with the five-year-ahead expected inflation rate hitting its lowest level since the start of the survey.

The rand has also appreciated against the dollar and stabilised against the euro, limiting imported inflation.

Another promising development is that the Bank has purchased a 50% stake in BankServ Africa, now known as PayInc, marking the beginning of what are expected to be significant changes in the national payments landscape.

Finally, and most importantly, the National Treasury followed the Bank’s suggestion in formally lowering the inflation target to 3%.

This not only gives the Bank political cover to target a lower inflation rate but also helps to simplify the communication around this goal.

Though it doesn’t always follow the Fed, the Reserve Bank keeps a close eye on it due to the outsized influence of American markets on global finance.

In fact, last week’s decision was proof that the MPC does not always have to wait for the Fed. This is partly due to domestic circumstances, but also because global financial conditions have been mostly supportive, notably with a stable rand-dollar exchange rate.

Ultimately, global markets determine how freely emerging market central banks can act. If the Fed turns hawkish at its upcoming meetings, pausing the cuts and changing the outlook, it could lead to a stronger dollar and increased market anxiety.

That will close off space for the Reserve Bank and other central banks to ease. If, however, the Fed continues to gradually ease, the Reserve Bank will have more confidence to do the same.

Therefore, if the dollar remains the dominant global currency, we need to keep a close track of American politics and policy, whether liking it or not.

Comments