Hidden threat to South Africa

The increasing frequency and severity of weather-related events in South Africa pose a serious threat to the country’s insurance industry and broader financial stability.

These events can result in significant losses for businesses and households, translating into substantial claims that insurers have to pay.

The increasing frequency and severity make it more costly for insurers to cover against these events, potentially limiting access to insurance and increasing the price of reinsurance in South Africa.

As a result, South Africa’s insurance gap is widening, which will exaggerate the financial impact of future weather-related events.

A further risk comes from the economic transition towards cleaner energy and sustainable alternatives, which impacts the value of assets reliant on historic ways of generating economic activity.

This is feedback from the Reserve Bank, which recently highlighted the growing impact of climate change on South Africa’s financial sector.

“More frequent extreme weather events are compounding financial sector vulnerability to climate risk,” it said in its second Financial Stability Review for 2025.

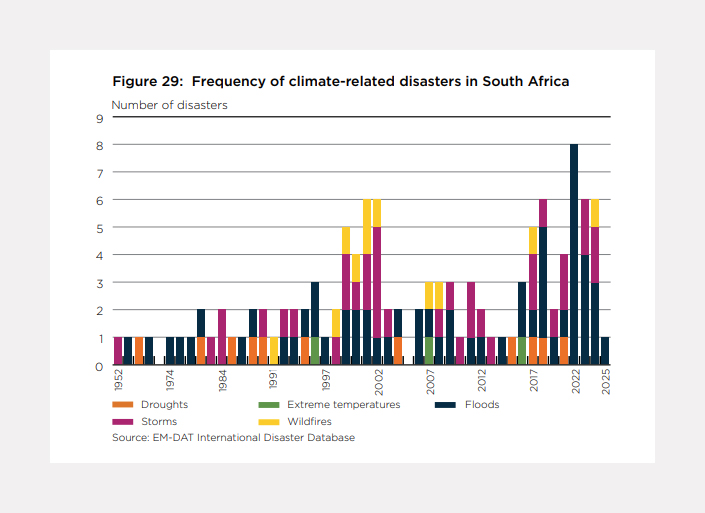

South Africa is no longer a catastrophe-free zone, with the country now experiencing several such events on an annual basis.

This has created new pressures for the country’s financial sector, with insurers facing rising reinsurance costs and increased claims.

As a result, the cost of insurance against these events has risen and is translating into a wider insurance gap.

The Reserve Bank said that only $3 billion (R51 billion) of the total $16 billion (R273 billion) in climate-related economic losses in South Africa have been insured.

It expects the uninsured portion, termed the ‘insurance gap’, to widen over time as extreme events become more common and severe.

Although the economic impact of these events has historically been manageable, the ongoing losses from the 2022 KwaZulu-Natal floods illustrate that future catastrophes could impose a high cost on the economy.

As coverage tightens or becomes costlier, activities that depend on insurability, such as mortgage lending and property development, may also be constrained, creating potential channels through which climate shocks could transmit to the broader economy.

Insurance crisis

The Reserve Bank has begun analysing the potential impact of a rise in climate-related events on South Africa’s financial services sector to better understand how they can be mitigated.

It began working on a specific climate stress test for South African banks, which laid a foundation from which the broader implications of such events on the country’s economy can be understood.

In the Financial Stability Review, it explained that it has shifted its attention to the insurance sector due to its ability to act as either a stabiliser or amplifier of financial stress.

The results from the various stress tests projected a fivefold increase in expected climate-related losses in South Africa over the coming decades as extreme weather events become more frequent and severe.

South African insurers have themselves become increasingly concerned about the impact of climate-related events on their businesses.

In particular, they have warned that a lack of investment in maintaining and upgrading the country’s infrastructure will exaggerate the impact of these events in the future.

For example, the impact of the KZN floods was exacerbated by poor urban planning, inadequate infrastructure, and insufficient stormwater drainage.

Santam chief underwriting officer Michael Cheng explained that the rise in extreme events and their increasing severity will prompt insurers to raise the cost of coverage in parts of South Africa.

While the number of domestic extreme weather events declined in 2023 and 2024, the economic losses were more severe.

Cheng said this rise has made extreme weather events a systemic risk to insurers, with the potential for them to destabilise the local industry.

Systemic risks are those with the potential to trigger widespread losses across multiple business sectors or geographic regions, threatening the functioning of the economy and the stability of the insurance industry.

Extreme weather events are increasingly classed as systemic risks as their frequency and severity increase over time.

Insurers have direct and indirect exposures to infrastructure shortcomings. For example, at the direct level, they ensure dams and power stations.

At the same time, the indirect impact arises from higher losses and damage to insured assets due to failing or poorly maintained infrastructure.

This is particularly concerning as urban development continues in flood-prone or inadequately serviced areas.

Santam has witnessed first-hand the ongoing expansion of building activity into high-risk areas, such as floodplains in Ladysmith and St Francis Bay and dolomitic zones like Centurion.

This translates into a higher average cost per claim for insurers, which necessitates either an increase in premiums charged or reduced coverage.

To limit these increases, insurers can implement higher excesses for selected risks, segmented premium increases, and enhanced selection and rating.

In South Africa, in particular, insurers have adapted by making infrastructure a core underwriting consideration to help them price premiums.

Comments