Interest rate cuts on the cards for South Africa

Inflation has continued to surprise on the downside relative to market expectations, resulting in the Reserve Bank having room to cut interest rates by 50 basis points over the coming year.

This is despite the Reserve Bank’s Monetary Policy Committee (MPC) stating that it is implicitly targeting the lower end of its 3% to 6% target range.

As other central banks around the world, particularly the United States Federal Reserve, are set to cut rates further, the Reserve Bank is likely to follow.

Furthermore, South Africa’s real interest rate remains relatively constrictive, with any further downturn in inflation likely to result in this rate being unnecessarily restrictive.

Coronation’s head of fixed interest, Nishan Maharaj, explained in a recent research note that these short-term cyclical factors are likely to benefit South African bond prices.

However, he warned that these factors are unlikely to result in any significant appreciation in bond prices and reduction in yields because of longer-term factors like the government’s financial health continuing to weigh on bonds.

Maharaj described the short-term factors as a band-aid over the structural issue of low economic growth, which has manifested itself as a financial crisis.

The main short-term factor boosting local bonds has been the Reserve Bank’s interest rate cutting cycle over the past two years.

South Africa’s repo rate is now sitting at 7%, with inflation at around 3%. This provides the Reserve Bank with its best opportunity to lower the inflation target.

In July, the bank’s MPC announced that it would target inflation closer to the lower end of its target band, 3%, without the endorsement of the National Treasury.

This brought about fears that rates may stay higher for longer or potentially even rise to ensure inflation remains at the 3% target, with economists projecting inflation to steadily rise towards 2026.

However, inflation has repeatedly surprised to the downside due to weak demand-side pressure and softer food and rental inflation.

“This has caused much excitement in cash markets, which initially moved towards expectations of 100 basis points of further cuts before settling in at 50 basis points over the next year,” Maharaj said.

“We expect the peak in inflation to be at 4% (previously at 4.5%) in the first quarter of 2026, which we believe will give the Reserve Bank room to ease interest rates a further 50 basis points over the next year.”

Maharaj said Coronation still expects inflation to average 4% over the next two years. Despite this, the real interest rate in South Africa remains restrictive at 2.5%.

Any further downward surprise in inflation will make this rate increasingly restrictive and potentially unnecessarily so.

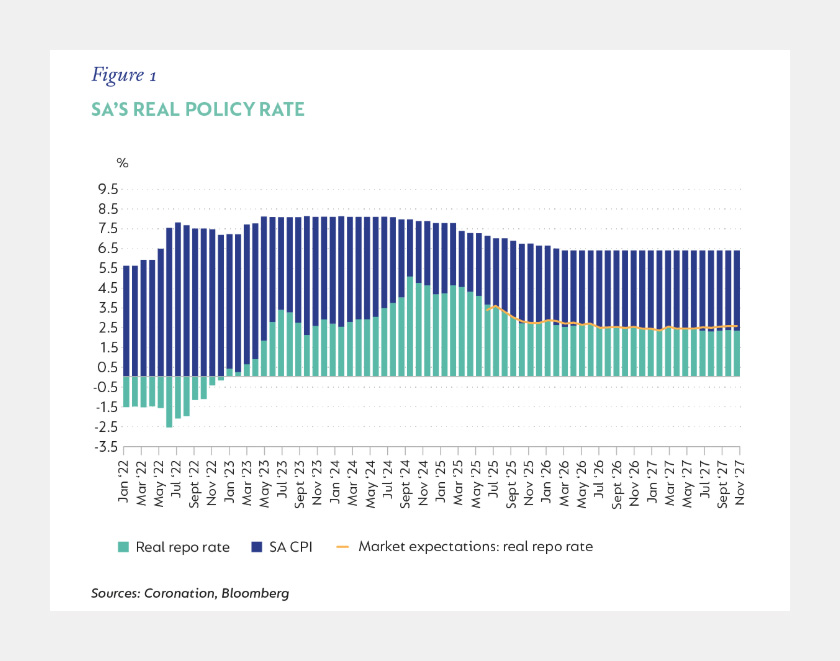

The graph below, courtesy of Maharaj and Coronation, shows South Africa’s real interest rate since January 2022 and includes the asset manager’s projection until November 2027.

November may come too soon

The Reserve Bank’s MPC meeting in November may come too soon for an interest rate cut, with it still looking to drag inflation expectations down to 3%.

Stanlib chief economist Kevin Lings explained that it is possible for interest rates to be cut in November, but that the meeting may come too soon.

Lings explained that headline inflation in South Africa has remained relatively stable and subdued within a narrow range from 2.7% to 3.3% over the past year.

While it is expected to tick upwards in the coming year, this shows that inflation has been tightly contained by the Reserve Bank.

Furthermore, the bank’s statement that it would target 3% inflation in South Africa should drag expectations down further.

“The latest inflation data should further encourage the Reserve Bank to consider cutting rates by a further 25 basis points before the end of the year – despite its 3% inflation goal,” Lings said.

“A cut of 25 basis points would not be in complete conflict with the recent downward revision to the Reserve Bank’s inflation objective of a sustained 3%.”

Inflation expectations in South Africa have declined over the past few months, with any downward surprise in inflation likely to bring them lower.

Lings said a downward surprise in inflation will probably make South Africa’s real interest rates unnecessarily high, constraining economic growth.

However, Lings said the Reserve Bank may be concerned about letting inflation drift further away from its 3% target.

As inflation rises, albeit slowly, away from that target, it will make it more difficult to bring it back down in future. This will likely result in interest rates remaining higher for longer and potentially even increasing, negatively impacting economic growth.

Lings explained that inflation is expected to increase over the next year as positive base effects roll off and administered price increases continue to place upward pressure on inflation.

Reserve Bank Governor Lesetja Kganyago has repeatedly come out in support of a lower inflation target by outlining its potential benefits.

Kganyago has explained that a lower inflation target, if met, will result in significantly lower interest rates in South Africa.

Reserve Bank researchers estimated that a lower inflation target of 3% can result in additional GDP growth of over 0.25% per year over five years and 0.4% per year within a decade.

In the researchers’ baseline scenario, debt-servicing costs as a percentage of GDP are projected to decline from 5.4% in 2025 to 5.3% in 2030 and 4.8% in 2035.

Comments